What Does Minimum Monthly Payment Mean On Credit Cards

adminse

Apr 05, 2025 · 7 min read

Table of Contents

Decoding the Minimum Monthly Payment on Credit Cards: A Comprehensive Guide

What if the seemingly innocuous minimum monthly payment on your credit card is secretly sabotaging your financial future? Understanding this seemingly simple figure is crucial for navigating the complexities of credit and building a strong financial foundation.

Editor’s Note: This article on minimum monthly credit card payments was published today, providing you with the most up-to-date information and insights to manage your credit card debt effectively.

Why Minimum Monthly Payments Matter: Relevance, Practical Applications, and Industry Significance

The minimum monthly payment on your credit card is more than just a suggested amount; it’s a critical factor influencing your overall financial health. Ignoring its implications can lead to snowballing debt, damaged credit scores, and significant long-term financial hardship. Understanding how this payment works, its implications, and strategies for managing it effectively is vital for responsible credit card usage and achieving financial stability. This knowledge empowers consumers to make informed decisions, avoid costly interest charges, and ultimately, achieve their financial goals faster.

Overview: What This Article Covers

This article dives deep into the world of minimum monthly credit card payments. We will explore its definition, calculation methods, the impact of paying only the minimum, strategies for effective debt management, and frequently asked questions. By the end, you will have a comprehensive understanding of this critical aspect of credit card management, empowering you to make financially sound decisions.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon information from reputable financial institutions, consumer advocacy groups, and legal resources related to consumer credit. We've analyzed numerous studies on consumer debt and credit card usage to provide accurate, unbiased information. The insights presented are backed by evidence and designed to provide actionable advice for responsible credit card management.

Key Takeaways:

- Definition and Core Concepts: A precise definition of the minimum monthly payment and its components.

- Calculation Methods: Understanding how credit card issuers calculate minimum payments.

- Impact of Paying Only the Minimum: The long-term financial consequences of consistently paying only the minimum.

- Strategies for Effective Debt Management: Practical tips and techniques for managing and reducing credit card debt efficiently.

- Legal Protections and Consumer Rights: Understanding your rights as a credit card holder.

Smooth Transition to the Core Discussion:

Now that we've established the importance of understanding minimum monthly payments, let's delve into the details, exploring the intricacies of this seemingly straightforward concept.

Exploring the Key Aspects of Minimum Monthly Payments

1. Definition and Core Concepts:

The minimum monthly payment is the smallest amount a credit card holder is required to pay each month to remain in good standing with their credit card issuer. This payment typically includes a portion of the outstanding balance (principal) and accrued interest. Failure to pay at least the minimum payment will result in late payment fees, negative impacts on your credit score, and potential collection actions.

2. Calculation Methods:

Credit card issuers use different methods to calculate minimum payments, but a common approach involves a percentage of the outstanding balance (usually between 1% and 3%) plus any accrued interest and fees. Some issuers may set a minimum payment amount regardless of the balance, ensuring at least a small payment is made each month. It's crucial to check your credit card statement for the precise calculation used by your issuer.

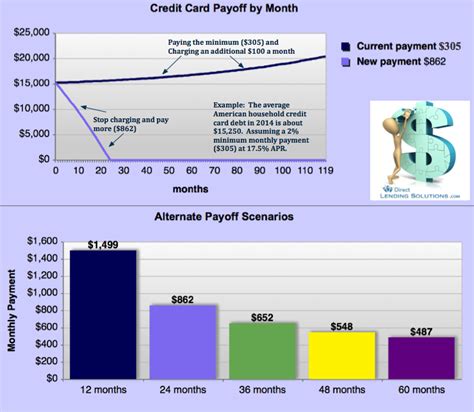

3. Impact of Paying Only the Minimum:

Paying only the minimum monthly payment might seem convenient, but it has severe long-term financial consequences. The primary problem is that a significant portion of your payment goes towards interest, leaving a minimal amount applied to the principal. This leads to a slow repayment process, extending the debt's lifespan and significantly increasing the overall interest paid. The longer it takes to repay your debt, the more interest you will accrue, effectively making the initial debt far more expensive.

4. Strategies for Effective Debt Management:

To avoid the pitfalls of only paying the minimum, consider these strategies:

- Budgeting and Expense Tracking: Understanding your spending habits is crucial for managing debt. Track your expenses to identify areas where you can cut back and allocate more funds toward debt repayment.

- Debt Snowball or Avalanche Method: The snowball method focuses on paying off the smallest debt first, building momentum and motivation. The avalanche method prioritizes paying off the debt with the highest interest rate first.

- Balance Transfers: Transferring your balance to a credit card with a lower interest rate can help reduce interest charges significantly.

- Debt Consolidation: Consolidate multiple debts into a single loan with a lower interest rate, simplifying repayment and potentially reducing the overall interest paid.

- Negotiating with Credit Card Companies: Contact your credit card issuer to explore options like lower interest rates, payment plans, or hardship programs. Be proactive and communicate your financial situation honestly.

5. Legal Protections and Consumer Rights:

Understand your rights as a credit card holder. The Fair Credit Reporting Act (FCRA) protects your credit information, while the Fair Debt Collection Practices Act (FDCPA) regulates how debt collectors can contact and interact with you. Familiarize yourself with these laws to ensure your rights are protected.

Exploring the Connection Between Interest Rates and Minimum Payments

The relationship between interest rates and minimum payments is fundamental to understanding the long-term cost of credit card debt. A higher interest rate means a larger portion of your minimum payment goes towards interest, leaving less to reduce the principal balance. This magnifies the impact of only making minimum payments, resulting in a much longer repayment period and significantly higher overall interest costs.

Key Factors to Consider:

- Roles and Real-World Examples: Consider a scenario where an individual has a $5,000 balance with a 15% interest rate. Only making minimum payments could lead to paying significantly more interest over several years, potentially doubling the total cost of the debt.

- Risks and Mitigations: The primary risk is the accumulation of substantial interest charges. Mitigation involves aggressive debt repayment strategies, such as those mentioned earlier.

- Impact and Implications: High interest rates associated with minimum payments lead to prolonged debt, impacting credit scores and overall financial well-being.

Conclusion: Reinforcing the Connection

The interplay between interest rates and minimum payments underscores the critical importance of proactive debt management. By understanding this connection and adopting appropriate strategies, consumers can minimize the financial burden of credit card debt.

Further Analysis: Examining Interest Rates in Greater Detail

Understanding the calculation of interest rates on credit cards is essential. The annual percentage rate (APR) is the annual cost of borrowing, factoring in all fees and interest. The method of calculating interest (e.g., daily periodic rate) significantly impacts the overall cost. Paying attention to these details will allow for informed decision-making and strategic debt management.

FAQ Section: Answering Common Questions About Minimum Monthly Payments

- What happens if I only pay the minimum payment? While you avoid immediate late fees, you will pay significantly more interest over time, extending the repayment period and increasing the total cost of the debt.

- How is the minimum payment calculated? The calculation usually involves a percentage of the outstanding balance plus accrued interest and fees. Check your credit card statement for the exact method used by your issuer.

- Can I negotiate a lower minimum payment? In certain circumstances, such as financial hardship, you can contact your credit card issuer to negotiate a lower payment or a payment plan.

- What is the impact on my credit score? Consistently paying only the minimum payment can negatively affect your credit score due to a high credit utilization ratio.

- What are my options if I can't afford the minimum payment? Contact your credit card issuer immediately to discuss possible solutions, such as hardship programs or payment plans, before your account goes into default.

Practical Tips: Maximizing the Benefits of Understanding Minimum Payments

- Understand the Basics: Learn the definition, calculation, and implications of minimum monthly payments.

- Track Your Spending: Monitor your expenses to identify areas for budget cuts and allocate more funds towards debt repayment.

- Develop a Repayment Plan: Employ strategies like the debt snowball or avalanche method to manage and reduce your debt.

- Consider Debt Consolidation: Explore options to consolidate your debts for a potentially lower interest rate.

- Negotiate with Your Issuer: Contact your credit card company to discuss payment options if you face financial difficulties.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding the implications of minimum monthly credit card payments is vital for long-term financial health. While convenient in the short term, consistently making only the minimum payment can lead to substantial financial burdens. By actively managing your debt, employing effective strategies, and understanding your rights, you can take control of your finances and build a secure financial future. Remember, proactive debt management is key to avoiding the pitfalls of minimum payments and achieving your financial goals.

Latest Posts

Latest Posts

-

How To Calculate Minimum Payment On Line Of Credit

Apr 06, 2025

-

How To Determine Monthly Loan Payment

Apr 06, 2025

-

How To Calculate Monthly Payment On A Loan

Apr 06, 2025

-

How To Calculate Minimum Payment On A Loan

Apr 06, 2025

-

How To Calculate Minimum Monthly Payment On A Loan

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about What Does Minimum Monthly Payment Mean On Credit Cards . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.