How Is The Minimum Payment Calculated For Credit Card

adminse

Apr 05, 2025 · 9 min read

Table of Contents

Decoding the Minimum Payment: Understanding How Credit Card Minimums are Calculated

What if understanding your credit card minimum payment calculation could save you thousands of dollars in interest? Mastering this seemingly simple calculation is key to responsible credit card use and financial freedom.

Editor’s Note: This article provides a comprehensive guide to credit card minimum payment calculations, updated with the latest information and industry practices. Understanding this crucial aspect of credit card management is vital for maintaining good credit health.

Why Minimum Payment Calculations Matter:

Credit card minimum payments are more than just a suggested amount; they represent a critical element in managing debt and credit scores. Failing to understand how these minimums are calculated can lead to significantly higher interest charges, prolonged debt repayment periods, and potential damage to your financial standing. The seemingly small minimum payment often masks the substantial cost of carrying a balance. Understanding the mechanics behind this calculation empowers consumers to make informed decisions about their finances and avoid the debt trap. This knowledge extends beyond personal finance; it has implications for businesses utilizing credit cards for operational expenses as well.

Overview: What This Article Covers

This article will delve into the intricacies of credit card minimum payment calculations, examining various methods employed by different credit card issuers. We’ll explore the factors influencing these calculations, including outstanding balance, interest accrued, and the issuer's specific policies. We’ll also address common misconceptions and offer practical strategies for responsible credit card management. The article will further analyze the long-term financial implications of consistently paying only the minimum, and explore alternative strategies for efficient debt repayment.

The Research and Effort Behind the Insights

This article is based on extensive research, drawing upon publicly available information from leading credit card companies, financial regulations, and expert analysis of consumer credit practices. Information regarding specific calculation methods has been compiled from official issuer documentation and reputable financial resources. The goal is to provide readers with accurate, unbiased information to assist them in understanding their credit card statements and managing their finances effectively.

Key Takeaways:

- Definition and Core Concepts: A clear explanation of minimum payment calculation methods and their underlying principles.

- Factors Influencing Calculations: Identification of key variables impacting minimum payment amounts.

- Common Calculation Methods: Analysis of different approaches used by credit card issuers.

- Long-Term Financial Implications: Assessment of the costs and consequences of consistently paying only the minimum.

- Strategies for Efficient Debt Repayment: Practical advice for managing credit card debt effectively.

Smooth Transition to the Core Discussion:

With a clear understanding of the importance of understanding minimum payment calculations, let's explore the key aspects that govern this crucial aspect of credit card management.

Exploring the Key Aspects of Minimum Payment Calculations:

1. Definition and Core Concepts:

The minimum payment on a credit card is the smallest amount a cardholder is required to pay each billing cycle to avoid late payment fees and maintain their account in good standing. However, this doesn't mean it's the best amount to pay. It's simply the minimum required to avoid immediate penalties. The calculation of this minimum payment varies between issuers, but typically incorporates a percentage of the outstanding balance, plus any accrued interest and applicable fees.

2. Factors Influencing Minimum Payment Calculations:

Several factors influence the calculation of your minimum payment. These include:

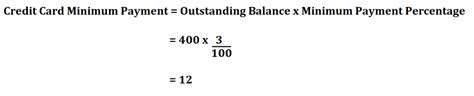

- Outstanding Balance: This is the most significant factor. The minimum payment is usually calculated as a percentage of the outstanding balance. This percentage can range from 1% to 3%, depending on the issuer and the cardholder's credit history.

- Accrued Interest: The interest charged on your outstanding balance is added to the minimum payment calculation. This is a crucial component and often the reason why paying only the minimum prolongs debt repayment.

- Fees: Any late payment fees, over-limit fees, or other charges incurred during the billing cycle are added to the minimum payment.

- Issuer's Policy: Each credit card issuer has its own policy regarding minimum payment calculation. These policies aren't always standardized and can differ significantly.

- Credit History: While not explicitly stated in the calculation formula, a cardholder's credit history can indirectly influence the minimum payment, particularly in cases of consistently late payments. Issuers might increase the minimum percentage in such scenarios.

3. Common Calculation Methods:

While the exact formula varies, several common approaches are used:

- Percentage of Balance Method: The most prevalent method, this involves calculating a fixed percentage (e.g., 2%) of the outstanding balance. This amount is then added to the accrued interest and any fees.

- Fixed Minimum Payment: Some issuers may have a fixed minimum payment amount, regardless of the outstanding balance. This is less common, especially for higher-limit cards.

- Tiered Minimum Payment: Certain issuers might employ a tiered system where the minimum payment percentage increases or decreases based on the outstanding balance. A higher balance might trigger a higher minimum payment percentage.

- Combination Method: A combination of percentage of balance and a fixed minimum amount. For example, the issuer might require 2% of the outstanding balance, but no less than $25.

4. Long-Term Financial Implications:

Paying only the minimum payment has significant long-term financial consequences:

- Prolonged Debt: Paying only the minimum barely covers the interest accrued, meaning the principal balance remains largely untouched. This significantly lengthens the repayment period.

- High Interest Costs: The accumulated interest over time far exceeds the amount repaid, leading to a substantially higher total cost compared to paying more than the minimum.

- Debt Snowball Effect: This can lead to accumulating more debt as you struggle to repay the principal.

- Credit Score Impact: While not directly impacting your credit score like late payments, consistently paying only the minimum suggests financial strain and can negatively influence your creditworthiness over time.

5. Strategies for Efficient Debt Repayment:

To avoid the pitfalls of minimum payments, consider these strategies:

- Pay More Than the Minimum: The most effective strategy is consistently paying more than the minimum payment each month, even if it's just a small increase.

- Debt Avalanche or Snowball Method: These are structured methods for prioritizing debt repayment, focusing on either the highest-interest debt (avalanche) or the smallest debt (snowball) to build momentum and motivation.

- Budgeting and Financial Planning: Create a comprehensive budget to identify areas where you can reduce spending and allocate more funds towards debt repayment.

- Balance Transfers: Consider transferring your balance to a card with a lower interest rate to reduce interest charges. Be mindful of balance transfer fees.

- Debt Consolidation: Explore debt consolidation options to combine multiple debts into a single loan with a lower interest rate. This simplifies repayment and reduces overall interest costs.

Exploring the Connection Between Interest Rates and Minimum Payment Calculations:

The relationship between interest rates and minimum payment calculations is crucial. Higher interest rates significantly inflate the interest component of the minimum payment, making it harder to reduce the principal balance. Even a small increase in the interest rate can have a substantial impact on the long-term cost of carrying a balance.

Key Factors to Consider:

- Roles and Real-World Examples: A card with a 20% APR will have a much higher interest component in the minimum payment compared to a card with a 10% APR, even if both have the same outstanding balance.

- Risks and Mitigations: High interest rates increase the risk of accumulating significant debt. Mitigation strategies include seeking lower-interest credit cards, paying more than the minimum, and exploring debt management options.

- Impact and Implications: The interest rate directly impacts the affordability and feasibility of paying off the debt, affecting both short-term and long-term financial stability.

Conclusion: Reinforcing the Connection:

The connection between interest rates and minimum payment calculations highlights the importance of carefully considering interest rates when choosing a credit card. Understanding this relationship empowers consumers to make informed decisions and avoid the pitfalls of high-interest debt.

Further Analysis: Examining APR in Greater Detail:

The Annual Percentage Rate (APR) is the annual interest rate charged on outstanding credit card balances. It's a crucial factor influencing minimum payments. A higher APR translates to higher interest charges, resulting in a larger minimum payment amount and a slower repayment process. Understanding how APR is calculated and the different types of APR (e.g., purchase APR, balance transfer APR, cash advance APR) is crucial for responsible credit card use.

FAQ Section: Answering Common Questions About Minimum Payments:

-

Q: What happens if I don't pay my minimum payment?

- A: You'll likely incur late payment fees, negatively impact your credit score, and potentially face collection actions.

-

Q: Can my minimum payment change from month to month?

- A: Yes, it can change based on your outstanding balance, interest accrued, and any new fees.

-

Q: Is it always best to pay more than the minimum payment?

- A: Yes, paying more than the minimum is almost always the best strategy to minimize interest charges and accelerate debt repayment.

-

Q: How can I calculate my minimum payment myself?

- A: While the exact calculation may vary depending on your issuer, you can get a good estimate by applying the percentage of balance method (typically 1-3%) to your outstanding balance, adding the interest and any fees. However, checking your statement is always the most accurate method.

-

Q: What if I'm struggling to pay even the minimum payment?

- A: Contact your credit card issuer immediately to discuss options like payment plans or hardship programs.

Practical Tips: Maximizing the Benefits of Understanding Minimum Payments:

- Review Your Statement Carefully: Understand the breakdown of your minimum payment, including the interest and fee components.

- Budget Effectively: Allocate sufficient funds each month to pay more than the minimum payment.

- Track Your Progress: Monitor your debt repayment progress regularly to stay motivated and adjust your payment strategy as needed.

- Explore Debt Management Options: Don't hesitate to seek professional help if you're struggling to manage your credit card debt.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding how minimum credit card payments are calculated is paramount for responsible financial management. While seemingly straightforward, this calculation holds significant implications for long-term financial health. By understanding the factors involved, avoiding the pitfalls of minimum payments, and employing effective debt repayment strategies, individuals can take control of their finances and avoid the burden of excessive credit card debt. Remember, informed choices are the cornerstone of sound financial planning.

Latest Posts

Latest Posts

-

How Does Mobile Pay Work

Apr 06, 2025

-

How Does Mobile Payments Work

Apr 06, 2025

-

How To Find Monthly Payment On A Loan

Apr 06, 2025

-

How Much Will My Monthly Loan Payment Be

Apr 06, 2025

-

How To Calculate Minimum Payment On Line Of Credit

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about How Is The Minimum Payment Calculated For Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.