What Percent Is Minimum Payment On Credit Card

adminse

Apr 05, 2025 · 8 min read

Table of Contents

Decoding the Minimum Payment on Your Credit Card: A Comprehensive Guide

What if the financial health of millions hinges on understanding the true cost of only making minimum credit card payments? This seemingly simple concept holds the key to financial freedom or crippling debt, depending on how it's managed.

Editor’s Note: This comprehensive guide to minimum credit card payments was published today, offering readers up-to-date information and actionable strategies for managing credit card debt effectively.

Why Understanding Minimum Payments Matters:

The minimum payment on a credit card—that seemingly small amount you see on your statement—is deceptively powerful. It impacts not only your credit score but also the overall cost of your debt and your long-term financial well-being. Understanding its implications is crucial for responsible credit management. Failing to grasp the true cost of minimum payments can lead to years of struggling with debt, accumulating significant interest charges, and damaging your creditworthiness. This affects your ability to secure loans, rent an apartment, or even get a job in some cases. The implications extend beyond individual finances; understanding minimum payments contributes to broader economic stability by fostering responsible borrowing habits.

Overview: What This Article Covers

This article will delve deep into the intricacies of minimum credit card payments, exploring their calculation, implications, and alternatives. Readers will learn how minimum payments are determined, the hidden costs of relying on them, the impact on credit scores, strategies for paying down debt faster, and the importance of proactively managing credit card balances. We will also examine factors that influence minimum payment amounts and offer practical advice for avoiding the debt trap.

The Research and Effort Behind the Insights

This article is based on extensive research, drawing from data from credit card issuers, financial analysis reports, and consumer protection agencies. We have consulted reputable sources to ensure accuracy and provide readers with evidence-based information. Our analysis includes real-world examples and scenarios to illustrate the potential financial consequences of relying solely on minimum payments.

Key Takeaways:

- Definition and Core Concepts: A clear explanation of what constitutes a minimum payment and how it's calculated.

- Practical Applications: Understanding how minimum payments impact debt repayment timelines and overall interest costs.

- Challenges and Solutions: Identifying the pitfalls of minimum payments and strategies for accelerating debt repayment.

- Future Implications: The long-term financial consequences of consistent minimum payments versus proactive debt management.

Smooth Transition to the Core Discussion:

Now that we've established the significance of understanding minimum credit card payments, let's explore the key aspects in detail.

Exploring the Key Aspects of Minimum Credit Card Payments

1. Definition and Core Concepts:

The minimum payment on a credit card is the smallest amount you are required to pay each billing cycle to avoid late payment fees and maintain your account in good standing. This amount is typically a small percentage of your outstanding balance, often between 1% and 3%, but it can also include any accrued interest charges and fees. The exact percentage is determined by your credit card issuer and is stipulated in your cardholder agreement. It's crucial to understand that this percentage is usually applied to the principal balance (the original amount you borrowed), not to the total amount due which also includes interest. This is a critical distinction that many cardholders overlook.

2. Applications Across Industries:

The minimum payment concept is consistent across the credit card industry, though the specific percentage and calculation methods may differ slightly between issuers. The calculation usually involves a base amount (e.g., $25) plus a percentage of the balance, ensuring that at least some progress is made towards paying off the debt. However, relying solely on this method drastically extends the repayment period and leads to far greater interest charges over the life of the debt.

3. Challenges and Solutions:

The primary challenge with minimum payments lies in the high accumulation of interest charges. Since only a small portion of the outstanding balance is paid off each month, the majority of the payment goes toward interest. This creates a vicious cycle, making it extremely difficult to eliminate the debt. Solutions include:

- Increasing payments: A deliberate effort to pay more than the minimum amount each month accelerates debt reduction and significantly reduces the total interest paid.

- Debt consolidation: Combining multiple high-interest debts into a single loan with a lower interest rate can simplify repayment and save money.

- Balance transfer: Transferring the balance to a credit card with a lower introductory APR (Annual Percentage Rate) can temporarily reduce interest costs, giving you more money to put toward the principal.

- Debt management plan: A formal program that helps you manage your debt by negotiating lower interest rates and creating a structured repayment plan.

4. Impact on Innovation:

While the core concept of minimum payments remains largely unchanged, the industry has seen innovations in debt management tools and financial planning resources. Apps and websites now provide debt repayment calculators and personalized strategies to help consumers manage their credit card debt more effectively. These advancements make it easier for individuals to understand the long-term implications of minimum payments and develop more strategic repayment plans.

Closing Insights: Summarizing the Core Discussion

The minimum payment is a double-edged sword. While it prevents immediate delinquency, it significantly prolongs debt repayment, leading to substantial interest accrual. Understanding its mechanics and opting for higher payments or employing alternative debt management strategies is paramount for responsible credit management and long-term financial health.

Exploring the Connection Between Interest Rates and Minimum Payments

The relationship between interest rates and minimum payments is pivotal. Higher interest rates mean a larger proportion of your minimum payment goes towards interest, leaving less to reduce the principal balance. This exacerbates the challenge of paying off the debt and can quickly lead to overwhelming debt burdens.

Key Factors to Consider:

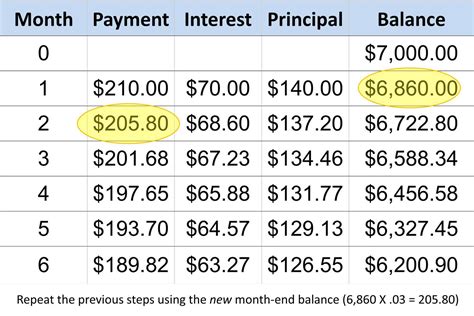

- Roles and Real-World Examples: Let's say you have a $5,000 balance with a 18% APR and a 2% minimum payment. Your minimum payment would be $100. A significant portion of this goes toward interest, and the principal reduction is minimal. Over time, the interest compounds, making the debt harder to repay.

- Risks and Mitigations: Relying solely on minimum payments significantly increases the risk of accumulating substantial debt, harming your credit score, and potentially leading to financial hardship. Mitigations include actively monitoring your credit report, budgeting effectively, and exploring debt management options.

- Impact and Implications: The long-term impact of consistently making only minimum payments can be devastating. It delays financial goals, impacts creditworthiness, and can lead to financial stress and even bankruptcy.

Conclusion: Reinforcing the Connection

The interplay between interest rates and minimum payments emphasizes the importance of proactive debt management. By acknowledging this connection and employing strategic repayment strategies, individuals can minimize interest charges and significantly reduce their debt burden.

Further Analysis: Examining Interest Calculation in Greater Detail

Credit card interest is usually calculated daily on your outstanding balance using a method called the average daily balance method. This means that the interest charges are not just applied to the original balance but accumulate daily, making early repayments beneficial. Understanding this compounding effect is crucial for responsible credit card management. The higher your interest rate, the faster the compound interest grows, reinforcing the importance of paying more than the minimum amount.

FAQ Section: Answering Common Questions About Minimum Credit Card Payments

- What is the typical percentage for a minimum credit card payment? While it varies by issuer, it commonly ranges from 1% to 3% of the outstanding balance, often with a minimum dollar amount.

- How is the minimum payment calculated? It generally involves a base amount plus a percentage of the outstanding balance, as detailed in your credit card agreement.

- What happens if I only pay the minimum payment? You avoid late fees but significantly increase the total interest paid and prolong the repayment period.

- Can I negotiate a lower minimum payment? While it's not always possible, you can contact your credit card issuer to discuss your situation and explore options. However, this rarely results in a permanently lower minimum payment, and it might affect your credit score negatively.

- How does paying more than the minimum payment affect my credit score? Paying more than the minimum reduces your credit utilization ratio (the percentage of available credit you're using), a positive factor influencing your credit score.

Practical Tips: Maximizing the Benefits of Responsible Credit Card Use

- Understand the Basics: Familiarize yourself with your credit card agreement, including the interest rate, minimum payment calculation, and late fee policy.

- Track Your Spending: Monitor your spending and ensure you can afford to pay off your balance in full each month, or at least a substantial portion of it.

- Prioritize High-Interest Debt: Focus on paying down high-interest debt first to reduce the overall cost of borrowing.

- Budget Effectively: Create a realistic budget that includes debt repayment as a priority.

- Explore Debt Management Options: If you're struggling with debt, explore options such as debt consolidation, balance transfers, or a debt management plan.

- Check your credit report regularly: This allows you to catch any errors and stay informed about your credit health.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding the implications of minimum credit card payments is essential for responsible financial management. While convenient in the short term, relying solely on minimum payments traps individuals in a cycle of debt, leading to significant interest costs and long-term financial instability. By actively managing credit card balances, employing strategic repayment strategies, and proactively seeking help when needed, individuals can avoid the debt trap and achieve lasting financial success. The seemingly small minimum payment holds the key to either financial freedom or crippling debt – the choice lies with the cardholder.

Latest Posts

Latest Posts

-

What Is The Minimum Payment On A 300 Credit Card Chase

Apr 05, 2025

-

What Is The Minimum Payment On A 1500 Credit Card Chase

Apr 05, 2025

-

What Is The Minimum Payment On A 3000 Credit Card Chase

Apr 05, 2025

-

What Is The Minimum Payment On Chase Credit Card

Apr 05, 2025

-

Tjxrewards Com Credit Card Payments

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about What Percent Is Minimum Payment On Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.