What Is The Minimum Payment On A $3000 Credit Card Chase

adminse

Apr 05, 2025 · 7 min read

Table of Contents

Decoding the Minimum Payment on a $3000 Chase Credit Card: A Comprehensive Guide

What if navigating your credit card payments felt less like a minefield and more like a well-charted course? Understanding your minimum payment on a $3000 Chase credit card is the first step towards responsible credit management.

Editor’s Note: This article provides up-to-date information on calculating and understanding minimum payments on Chase credit cards, as of October 26, 2023. Credit card terms and conditions can change, so always refer to your specific cardholder agreement for the most accurate details.

Why Understanding Your Minimum Payment Matters:

Ignoring or misunderstanding your minimum payment on a $3000 (or any amount) Chase credit card can have serious financial consequences. It directly impacts your credit score, interest accrual, and overall debt burden. Understanding this seemingly simple figure is crucial for responsible credit management and long-term financial well-being. This knowledge empowers you to make informed decisions about your finances, avoiding late fees, high interest charges, and potential damage to your credit history. The information presented here applies not only to a $3000 balance but also provides a framework for understanding minimum payments regardless of your credit card debt.

Overview: What This Article Covers:

This article will dissect the complexities surrounding minimum payments on Chase credit cards, focusing on a $3000 balance as an example. We’ll explore how minimum payments are calculated, the dangers of only paying the minimum, strategies for paying down debt more efficiently, and resources available to help manage credit card debt effectively. We'll also touch on the importance of reading your statement carefully and understanding the nuances of your specific card agreement.

The Research and Effort Behind the Insights:

The information presented here is based on a review of Chase's official website, credit card agreements, and publicly available information regarding credit card minimum payments. We’ve also considered industry best practices and advice from financial experts to provide a well-rounded and accurate understanding of this crucial aspect of credit card management.

Key Takeaways:

- Minimum Payment Calculation: Understanding the formula Chase uses to determine your minimum payment.

- The High Cost of Minimum Payments: Illustrating the long-term financial impact of only paying the minimum.

- Strategies for Accelerated Debt Repayment: Exploring effective methods to pay off your debt faster.

- Resources for Debt Management: Identifying helpful tools and organizations that can assist with debt reduction.

- Preventing Future Debt Accumulation: Proactive steps to avoid high credit card balances.

Smooth Transition to the Core Discussion:

Now that we understand the importance of understanding your minimum payment, let's delve into the specifics. We'll start by examining how Chase calculates this vital figure.

Exploring the Key Aspects of Minimum Payments on Chase Credit Cards:

1. Definition and Core Concepts:

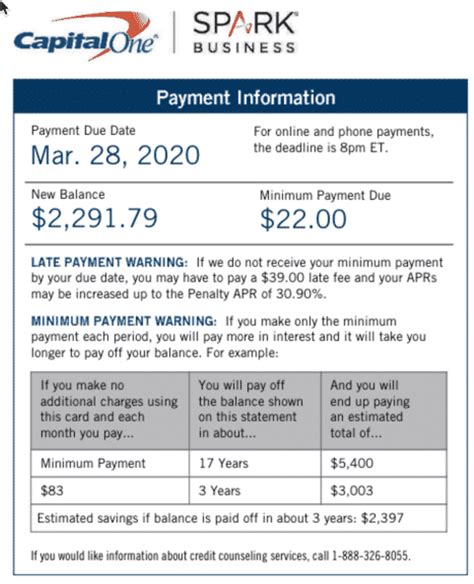

Chase, like most credit card issuers, doesn't use a fixed percentage for minimum payments. Instead, the minimum payment is typically calculated as the greater of:

- A fixed minimum dollar amount: This is a small, set amount, often between $25 and $35, regardless of your balance.

- A percentage of your outstanding balance: This percentage is usually between 1% and 3% of the balance, but it could vary based on your specific card agreement.

For a $3000 balance, let's assume a 1% minimum payment: $3000 x 0.01 = $30. However, if the fixed minimum is $35, then your minimum payment would be $35. Always check your statement for the precise amount.

2. Applications Across Industries:

This calculation method is standard across most major credit card providers in the United States. While the specific percentages and fixed minimums may vary slightly, the core concept remains consistent.

3. Challenges and Solutions:

The primary challenge is the temptation to only pay the minimum payment. While convenient, this approach significantly prolongs the repayment period and substantially increases the total interest paid over the life of the debt. The solution is to consciously make larger payments than the minimum whenever possible.

4. Impact on Innovation:

Financial institutions are increasingly incorporating technology to assist with debt management. Many offer online tools and mobile apps that allow you to track payments, visualize debt reduction, and explore repayment options.

Closing Insights: Summarizing the Core Discussion:

Understanding your minimum payment is critical for responsible credit card management. While the minimum payment may seem small in comparison to the total balance, it's crucial to remember that paying only the minimum significantly increases the overall cost of borrowing and prolongs your debt.

Exploring the Connection Between Interest Rates and Minimum Payments:

The relationship between your interest rate and your minimum payment is profoundly significant. A higher interest rate means a larger portion of your minimum payment goes towards interest, leaving a smaller amount to reduce your principal balance. This creates a vicious cycle where it takes much longer to pay off the debt, and you end up paying significantly more in interest.

Key Factors to Consider:

- Roles and Real-World Examples: Let's say your Chase card has a 20% APR. A $30 minimum payment on a $3000 balance would barely make a dent in the principal, with most of the payment allocated to interest.

- Risks and Mitigations: Only making minimum payments can lead to accumulating more debt over time and negatively impact your credit score. To mitigate this, actively seek to make larger payments than the minimum, even if it’s just a small increase each month.

- Impact and Implications: Long-term, relying solely on minimum payments results in a substantial increase in the total amount repaid. This can severely restrict your financial flexibility and limit your ability to achieve other financial goals.

Conclusion: Reinforcing the Connection:

The connection between interest rates and minimum payments highlights the importance of paying more than the minimum whenever feasible. Actively managing your debt, even with small incremental increases in your payments, can significantly reduce the total cost of borrowing and accelerate debt repayment.

Further Analysis: Examining Interest Rates in Greater Detail:

High interest rates are the enemy of debt reduction. Understanding your APR (Annual Percentage Rate) is essential. Chase offers a variety of cards with different APRs, ranging from relatively low to quite high, depending on your creditworthiness and the specific card. A higher credit score often qualifies you for a lower APR.

FAQ Section: Answering Common Questions About Chase Credit Card Minimum Payments:

- What happens if I only pay the minimum payment? While you avoid late fees, you’ll pay significantly more in interest over time, and it will take much longer to eliminate your debt.

- Can I change my minimum payment amount? No, you can't change the calculated minimum payment. However, you can always pay more than the minimum.

- What if I miss a minimum payment? You'll likely incur a late fee, and it will negatively impact your credit score.

- How can I determine my exact minimum payment? Always refer to your monthly statement or your online account details provided by Chase.

Practical Tips: Maximizing the Benefits of Responsible Credit Card Management:

- Understand the Basics: Know your APR, minimum payment calculation, and due date.

- Budget Strategically: Allocate a portion of your income each month towards your credit card debt.

- Explore Debt Repayment Strategies: Consider methods like the debt snowball or debt avalanche methods to accelerate repayment.

- Consider a Balance Transfer: A balance transfer card with a 0% introductory APR can help you save money on interest if you can pay off the balance within the promotional period.

- Seek Professional Advice: If you're struggling with debt, consider contacting a non-profit credit counseling agency for assistance.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding your minimum payment on a $3000 Chase credit card, or any credit card for that matter, is crucial for responsible financial management. While the minimum payment might seem manageable, it’s vital to recognize its limitations and actively strive to pay more to minimize interest charges and expedite debt repayment. By proactively managing your debt, you can safeguard your financial future and build a stronger credit profile. Remember, responsible credit card use is key to long-term financial success.

Latest Posts

Latest Posts

-

What Is The Minimum Payment Due On A Discover Card

Apr 05, 2025

-

How Much Is Discover Minimum Payment

Apr 05, 2025

-

How Is Credit Card Minimum Payment Calculated Discover

Apr 05, 2025

-

How Is The Minimum Payment Calculated On A Discover Card

Apr 05, 2025

-

What Will My Minimum Credit Card Payment Be Calculator

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about What Is The Minimum Payment On A $3000 Credit Card Chase . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.