What Will My Minimum Credit Card Payment Be Calculator

adminse

Apr 05, 2025 · 8 min read

Table of Contents

What if managing your credit card debt hinges on understanding your minimum payment?

Accurately calculating your minimum credit card payment is crucial for responsible credit management and avoiding costly interest charges.

Editor’s Note: This article on calculating minimum credit card payments was published today, providing readers with up-to-date information and strategies for effective credit management. This guide provides a comprehensive overview of calculating minimum payments, factors influencing them, and the long-term financial implications of various payment strategies.

Why Understanding Minimum Credit Card Payments Matters:

Understanding your minimum credit card payment isn't just about avoiding late fees; it's about responsible financial management. Failing to grasp the implications of only paying the minimum can lead to a snowball effect of accumulating interest and debt, significantly impacting your credit score and long-term financial health. Knowing how to calculate this crucial figure empowers you to make informed decisions, budget effectively, and ultimately, control your finances. This knowledge is relevant for everyone, from students managing their first credit card to established professionals aiming to optimize their debt repayment strategies.

Overview: What This Article Covers

This article provides a detailed guide to understanding and calculating your minimum credit card payment. We will explore the various factors influencing the minimum payment, dissect common calculation methods, examine the long-term financial consequences of only making minimum payments, and provide practical strategies for managing credit card debt effectively. The article concludes with a frequently asked questions section and actionable tips for maximizing your financial well-being.

The Research and Effort Behind the Insights

This article is based on extensive research into credit card agreements, financial regulations, and industry best practices. Data on interest rates, minimum payment calculations, and debt accumulation scenarios are sourced from reputable financial institutions and government agencies. The analysis presented here is intended to provide accurate and actionable insights for readers seeking to manage their credit card debt responsibly.

Key Takeaways:

- Definition and Core Concepts: A precise understanding of what constitutes a minimum credit card payment and the factors affecting its calculation.

- Calculation Methods: Exploration of different ways to calculate minimum payments, including common formulas and online tools.

- Practical Applications: Real-world examples illustrating how minimum payments impact long-term debt and interest accumulation.

- Challenges and Solutions: Identifying the pitfalls of only paying the minimum and strategies for developing more effective repayment plans.

- Future Implications: Long-term financial consequences of minimum payment strategies and the impact on credit scores.

Smooth Transition to the Core Discussion

Now that we've established the importance of understanding your minimum credit card payment, let's delve into the specifics of calculation, the factors involved, and the implications of various payment strategies.

Exploring the Key Aspects of Minimum Credit Card Payment Calculation

Definition and Core Concepts:

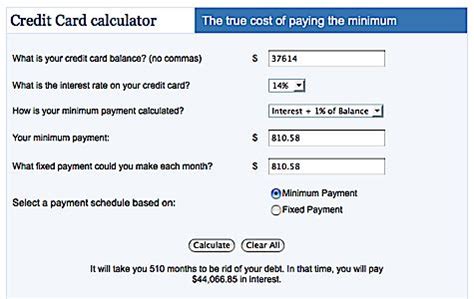

The minimum credit card payment is the smallest amount you're required to pay each billing cycle to avoid late fees and maintain your account in good standing. This amount is typically a percentage of your outstanding balance (often between 1% and 3%), or a fixed minimum dollar amount, whichever is greater. It's crucial to understand that this minimum payment usually only covers a small portion of your debt, leaving a significant portion to accrue interest.

Calculation Methods:

There's no single universal formula for calculating minimum credit card payments. The calculation varies depending on the credit card issuer and the terms outlined in your credit card agreement. However, some common methods include:

-

Percentage of Balance: Many issuers calculate the minimum payment as a percentage (e.g., 1% to 3%) of your outstanding balance. If your balance is $1000 and the minimum payment percentage is 2%, your minimum payment would be $20.

-

Fixed Minimum: Some issuers set a fixed minimum dollar amount, regardless of your balance. For example, the minimum payment might be $25, regardless of whether your balance is $500 or $5000.

-

Combination Method: The most common approach is a combination of both percentage and fixed minimum. The issuer calculates the minimum payment as a percentage of your balance, and if that amount is less than a fixed minimum, the fixed minimum becomes your minimum payment.

-

Online Calculators: Many banks and financial websites provide online calculators that can estimate your minimum payment based on your balance, interest rate, and credit card terms. These calculators are helpful but might not reflect your exact minimum payment, as the specific calculation methods vary by issuer.

Applications Across Industries:

The concept of minimum payments is consistent across the credit card industry, although the specific calculation methods may vary slightly between issuers. Understanding these variations is crucial for making informed financial decisions.

Challenges and Solutions:

The primary challenge associated with minimum payments is that they often lead to a cycle of accumulating debt. Because a significant portion of the balance remains unpaid, interest continues to accrue, potentially causing the debt to grow over time, even with consistent minimum payments.

Solutions include:

- Budgeting: Create a realistic budget that allows you to pay more than the minimum.

- Debt Consolidation: Consider consolidating your high-interest debt into a lower-interest loan.

- Balance Transfers: Explore balance transfer credit cards that offer a 0% introductory APR period.

- Debt Management Programs: Enroll in a debt management program offered by a credit counseling agency.

Impact on Innovation:

The credit card industry is constantly evolving, with new technologies and features emerging. However, the fundamental principle of minimum payments remains, underscoring the importance of financial literacy and responsible credit management.

Closing Insights: Summarizing the Core Discussion

Understanding your minimum credit card payment is fundamental to responsible financial management. While paying only the minimum might seem convenient in the short term, it can lead to long-term debt accumulation and significant financial repercussions. By understanding the calculation methods, factors involved, and the potential consequences, individuals can make informed decisions and develop effective strategies for managing their credit card debt responsibly.

Exploring the Connection Between Interest Rates and Minimum Credit Card Payments

The relationship between interest rates and minimum credit card payments is critical. Higher interest rates lead to faster debt accumulation, even when making consistent minimum payments. Conversely, lower interest rates slow down the growth of debt, giving individuals more financial flexibility.

Key Factors to Consider:

Roles and Real-World Examples:

Imagine two individuals, both with a $1000 balance. One has a card with a 15% interest rate, while the other has a card with a 5% interest rate. Even if both make the same minimum payment, the individual with the higher interest rate will see their debt grow significantly faster due to the compounding effect of interest.

Risks and Mitigations:

The primary risk associated with high interest rates and minimum payments is the potential for debt to snowball out of control. Mitigating this risk involves actively seeking lower interest rates through balance transfers, debt consolidation, or negotiating with your credit card issuer.

Impact and Implications:

High interest rates coupled with minimum payments can severely impact an individual's credit score, limiting access to future credit and increasing the overall cost of borrowing.

Conclusion: Reinforcing the Connection

The connection between interest rates and minimum payments is undeniably crucial. High interest rates accelerate debt accumulation, emphasizing the need for proactive debt management strategies. Understanding this relationship enables individuals to make more informed decisions regarding their credit card payments and overall financial well-being.

Further Analysis: Examining Interest Calculation in Greater Detail

Interest on credit cards is typically calculated daily on your outstanding balance, then added to your account at the end of the billing cycle. This daily compounding means that even small balances can accumulate substantial interest over time. This underscores the importance of paying more than the minimum whenever possible to minimize the total amount of interest paid.

FAQ Section: Answering Common Questions About Minimum Credit Card Payments

What is a minimum credit card payment?

It’s the smallest amount you can pay each billing cycle to avoid late fees. However, paying only the minimum often leads to significant interest charges over time.

How is my minimum credit card payment calculated?

The calculation varies by issuer but typically involves a percentage of your balance or a fixed minimum dollar amount, whichever is greater.

What happens if I only pay the minimum?

You will avoid late fees, but your debt will likely grow due to accumulating interest charges. This can negatively impact your credit score and overall financial health.

What are the risks of only paying the minimum?

The risks include accumulating debt, increased interest charges, potential damage to your credit score, and reduced access to credit in the future.

What are some strategies for paying down my credit card debt more efficiently?

Strategies include creating a budget, making more than the minimum payment, exploring debt consolidation or balance transfers, and seeking help from a credit counselor.

Practical Tips: Maximizing the Benefits of Understanding Your Minimum Payment

-

Track Your Spending: Monitor your spending to avoid exceeding your credit limit and accumulating unnecessary debt.

-

Pay More Than the Minimum: Allocate extra funds to pay down your balance faster, significantly reducing the total interest paid.

-

Review Your Credit Card Agreement: Understand the terms and conditions, including the calculation method for your minimum payment and any associated fees.

-

Explore Debt Management Options: If you're struggling to manage your debt, consider debt consolidation, balance transfers, or credit counseling.

-

Regularly Check Your Credit Report: Monitor your credit score and look for any discrepancies or potential issues.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding your minimum credit card payment is not just about avoiding late fees; it's a cornerstone of responsible financial management. By grasping the calculation methods, understanding the implications of only paying the minimum, and actively implementing effective repayment strategies, individuals can take control of their finances, build a strong credit history, and achieve long-term financial stability. The information in this article provides a solid foundation for navigating the complexities of credit card debt and making informed decisions that contribute to a secure financial future.

Latest Posts

Latest Posts

-

How Does Phonepe Work

Apr 06, 2025

-

How Does Mobile Wallet Work With Moneygram

Apr 06, 2025

-

How Does Phone Payments Work

Apr 06, 2025

-

How Does Mobile Wallet Work

Apr 06, 2025

-

How Do Mobile Wallet Work

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about What Will My Minimum Credit Card Payment Be Calculator . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.