When Do You Pay Minimum Payment On Credit Card

adminse

Apr 05, 2025 · 6 min read

Table of Contents

When Should You Pay Only the Minimum Payment on Your Credit Card? (Almost Never)

Should you ever only pay the minimum payment on your credit card? The short answer is almost never. While it might seem like a convenient option in a pinch, understanding the long-term financial implications is crucial before making this choice. This article delves into the complexities of minimum credit card payments, exploring when (and why) it's rarely the right decision.

Editor’s Note: This article on the strategic use of minimum credit card payments was published today, offering current insights and advice for managing credit card debt responsibly. It's crucial to remember that financial situations are unique; always consult with a financial advisor for personalized guidance.

Why Minimum Payments Matter: A High Price for Convenience

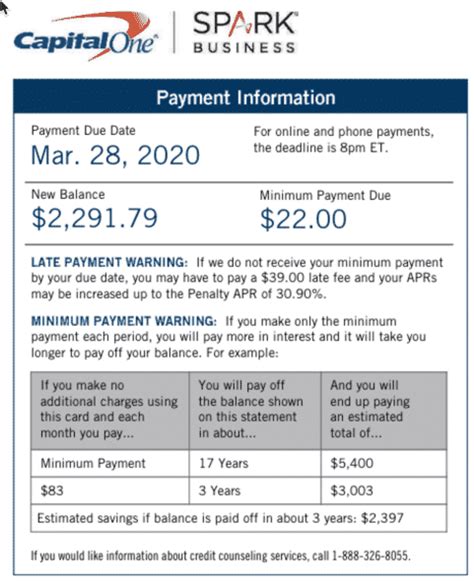

The allure of minimum payments is undeniable. Facing unexpected expenses or a tight budget, the seemingly small minimum payment can provide temporary relief. However, this short-term gain often comes at a significant long-term cost. Minimum payments only cover the interest accrued, leaving the principal balance largely untouched. This results in:

- Prolonged Debt: Paying only the minimum dramatically extends the repayment period, leading to years, even decades, of debt.

- Accumulated Interest: The majority of your payment goes towards interest, leaving you paying far more than the original amount borrowed.

- Damaged Credit Score: High credit utilization (the percentage of your available credit you’re using) negatively impacts your credit score, hindering future borrowing opportunities.

- Financial Stress: The constant burden of a long-term debt can lead to significant financial stress and limit your ability to save and invest.

Overview: What This Article Covers

This article provides a comprehensive analysis of minimum credit card payments, covering their implications, exceptions to the rule, and strategic considerations. Readers will gain actionable insights into responsible credit card management and understand the long-term costs of consistently making only minimum payments.

The Research and Effort Behind the Insights

This article is based on extensive research, drawing from reputable financial sources, including government publications, consumer finance websites, and academic studies on consumer debt. Data on average interest rates, debt accumulation models, and the impact on credit scores are incorporated to ensure accurate and trustworthy information.

Key Takeaways:

- Understanding Interest Accrual: A detailed breakdown of how interest compounds on unpaid credit card balances.

- Impact on Credit Scores: How consistently making minimum payments affects creditworthiness.

- Alternative Debt Management Strategies: Exploring options like balance transfers, debt consolidation, and seeking professional financial advice.

- Calculating Total Repayment Costs: Methods for estimating the overall cost of making only minimum payments versus paying down the debt more aggressively.

Smooth Transition to the Core Discussion

Understanding the high cost of solely relying on minimum payments is the first step towards responsible credit card management. Let's now explore the key aspects of this financial strategy and its long-term consequences in detail.

Exploring the Key Aspects of Minimum Credit Card Payments

1. Definition and Core Concepts: The minimum payment is the smallest amount a credit card company requires you to pay each month to remain in good standing. This amount typically includes a portion of the interest accrued and a small portion of the principal balance.

2. Applications Across Industries: The concept of minimum payments is universal across most credit card issuers, though the specific calculation methods and minimum payment amounts can vary.

3. Challenges and Solutions: The primary challenge is the slow repayment speed and the high accumulation of interest. Solutions involve creating a budget, exploring debt repayment strategies, and prioritizing debt reduction.

4. Impact on Innovation: The financial industry's innovation in credit card products and debt management tools has aimed to both increase transparency and provide tools to help consumers manage their debt more effectively.

Closing Insights: Summarizing the Core Discussion

Relying solely on minimum payments creates a cycle of debt that can be difficult to break. The high interest charges and slow repayment periods result in a significantly higher overall cost compared to paying down the debt more aggressively.

Exploring the Connection Between Interest Rates and Minimum Payments

The relationship between interest rates and minimum payments is crucial. Higher interest rates mean a larger portion of your minimum payment goes toward interest, leaving less to reduce the principal. This amplifies the negative consequences of only making minimum payments.

Key Factors to Consider:

- Roles and Real-World Examples: A person with a high interest rate and a large balance will see a disproportionately larger amount of their minimum payment go towards interest, extending the repayment period significantly.

- Risks and Mitigations: The risk is extended debt and financial stress. Mitigation strategies include budgeting, exploring debt consolidation, and seeking financial counseling.

- Impact and Implications: The long-term impact is a substantially higher total cost of borrowing and a potential negative impact on credit scores.

Conclusion: Reinforcing the Connection

The link between interest rates and minimum payments highlights the importance of proactive debt management. By understanding how interest rates impact your minimum payment, you can make informed decisions about your repayment strategy.

Further Analysis: Examining Interest Rates in Greater Detail

Interest rates on credit cards are typically variable, meaning they can fluctuate based on market conditions. This adds an element of uncertainty to your minimum payment calculations, making it even more critical to aim for aggressive repayment.

FAQ Section: Answering Common Questions About Minimum Payments

- Q: What happens if I only pay the minimum payment on my credit card? A: You will continue to accrue interest, prolonging the repayment period and increasing the total cost.

- Q: How is the minimum payment calculated? A: The calculation varies by issuer but generally includes a portion of the interest and a small amount of the principal.

- Q: Will making only minimum payments affect my credit score? A: Yes, high credit utilization (due to a large outstanding balance) negatively impacts your credit score.

- Q: What are the alternatives to minimum payments? A: Consider debt consolidation, balance transfers, or working with a credit counselor.

Practical Tips: Maximizing the Benefits of Responsible Credit Card Use

- Budgeting: Create a detailed budget to track income and expenses, ensuring you can afford your credit card payments.

- Prioritize Debt Reduction: Make extra payments whenever possible to accelerate repayment and minimize interest charges.

- Debt Consolidation: Explore consolidating high-interest debt into a lower-interest loan to reduce monthly payments.

- Balance Transfers: Transfer high-interest balances to a card with a lower introductory APR.

- Seek Professional Help: Consult a financial advisor or credit counselor for personalized guidance on debt management.

Final Conclusion: Wrapping Up with Lasting Insights

While minimum payments offer temporary convenience, they are rarely a financially sound long-term strategy. Understanding the mechanics of interest accrual, credit utilization, and alternative debt management strategies is crucial for responsible credit card management. By proactively managing your credit card debt and avoiding the trap of minimum payments, you can safeguard your financial future and achieve lasting financial stability.

Latest Posts

Latest Posts

-

How To Teach A 3 Year Old About Money

Apr 06, 2025

-

How To Teach Kids Financial Management

Apr 06, 2025

-

Ramsey 8

Apr 06, 2025

-

Retainerd Earning

Apr 06, 2025

-

How Does A Retainer Salary Work

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about When Do You Pay Minimum Payment On Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.