What's The Average Monthly Payment For Student Loans

adminse

Apr 05, 2025 · 8 min read

Table of Contents

What's the true cost of higher education? Deciphering the average monthly student loan payment.

Understanding your monthly student loan payment is crucial for effective financial planning after graduation.

Editor's Note: This article on average monthly student loan payments was published on {Date}. The information provided reflects current trends and data, but individual loan payments vary significantly. It's crucial to consult your loan servicer for personalized details.

Why Understanding Average Monthly Student Loan Payments Matters

Navigating the complexities of student loan debt is a significant challenge for many recent graduates and even those who borrowed years ago. Understanding the average monthly payment isn't just a matter of simple arithmetic; it’s crucial for responsible financial planning. This knowledge allows borrowers to budget effectively, prioritize debt repayment strategies, and avoid the pitfalls of overwhelming debt. The average monthly payment impacts everything from housing decisions and saving for a down payment on a house to retirement planning and overall financial well-being. Furthermore, understanding these averages provides context for policy discussions surrounding student loan debt and its impact on the economy.

What This Article Covers

This article will delve into the intricacies of average monthly student loan payments, exploring factors that influence these amounts, analyzing data from various sources, and offering practical advice for managing student loan debt. We will cover:

- Factors Determining Monthly Payments: Loan amount, interest rate, loan type, repayment plan, and loan forgiveness programs.

- Data Analysis and Trends: Examining recent data on average student loan debt and monthly payments.

- Different Repayment Plans: Exploring the various repayment options available to borrowers and their impact on monthly payments.

- Strategies for Managing Student Loan Debt: Practical tips and advice for effectively managing and repaying student loans.

- The Impact of Income-Driven Repayment Plans: How income-driven repayment plans affect monthly payments and long-term repayment.

- Potential for Loan Forgiveness Programs: Overview of available loan forgiveness programs and their eligibility criteria.

- Frequently Asked Questions: Addressing common questions about average monthly student loan payments.

The Research and Effort Behind the Insights

This article draws upon data from reputable sources including the U.S. Department of Education, the Federal Reserve, the Consumer Financial Protection Bureau (CFPB), and various academic studies. The information presented reflects a comprehensive analysis of publicly available data and expert opinions to provide readers with accurate and trustworthy insights. The analysis acknowledges the limitations of using averages and emphasizes the importance of individual loan details.

Key Takeaways:

- There is no single "average" monthly student loan payment. The amount varies drastically based on several individual factors.

- Understanding your individual loan terms and repayment options is crucial for effective financial planning.

- Several repayment plans are available, each with different implications for monthly payments and total repayment costs.

- Proactive debt management strategies can significantly impact the long-term financial health of borrowers.

Smooth Transition to the Core Discussion

With a grasp of the significance of understanding individual monthly payments, let's examine the key factors that contribute to the wide range of monthly student loan bills.

Exploring the Key Aspects of Average Monthly Student Loan Payments

1. Loan Amount: The most significant factor influencing monthly payments is the total amount borrowed. Larger loan balances naturally translate to higher monthly payments, regardless of interest rates or repayment plans.

2. Interest Rate: Student loan interest rates fluctuate depending on the type of loan (federal vs. private), the year the loan was disbursed, and prevailing market conditions. Higher interest rates result in larger monthly payments and a greater total cost of borrowing over the loan's lifetime.

3. Loan Type: Federal student loans and private student loans differ significantly in their terms and conditions, including interest rates, repayment options, and borrower protections. Federal loans typically offer more flexible repayment plans and income-driven repayment options.

4. Repayment Plan: The chosen repayment plan significantly impacts the monthly payment amount. Standard repayment plans typically require higher monthly payments over a shorter period, while extended repayment plans spread payments over a longer duration, resulting in lower monthly payments but higher total interest paid. Income-driven repayment plans adjust monthly payments based on income and family size, making them more manageable for borrowers with lower incomes.

5. Loan Forgiveness Programs: Certain professions or circumstances may qualify borrowers for loan forgiveness programs, eliminating the need for further payments. However, eligibility requirements are often stringent, and forgiveness doesn't typically happen overnight. These programs don’t affect the monthly payment until forgiveness is granted, but they offer long-term relief.

Data Analysis and Trends

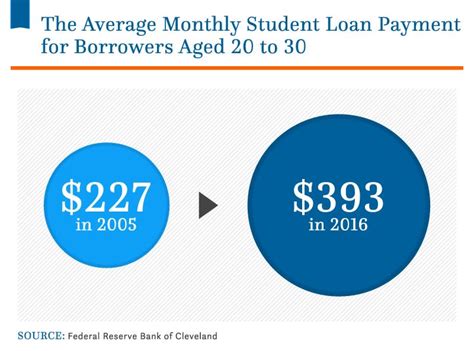

While a precise average monthly student loan payment is elusive due to the varied factors mentioned above, data from the U.S. Department of Education and other sources reveals trends. The average student loan debt for borrowers in recent years has climbed, leading to higher average monthly payments. This increase reflects rising tuition costs and an increase in the number of students borrowing to finance their education. However, it's important to remember that these are averages, masking the reality of significantly higher or lower payments for individual borrowers.

Different Repayment Plans and Their Impact

- Standard Repayment Plan: Fixed monthly payments over 10 years. This plan results in the lowest total interest paid but potentially higher monthly payments.

- Graduated Repayment Plan: Payments start low and gradually increase over time. This can be helpful initially but leads to significantly higher payments later in the repayment term.

- Extended Repayment Plan: Payments are spread over a longer period (up to 25 years for federal loans), resulting in lower monthly payments but higher total interest paid.

- Income-Driven Repayment (IDR) Plans: Monthly payments are based on income and family size. These plans are designed to make repayment more manageable for borrowers with lower incomes, but they often extend the repayment period significantly. Examples include ICR, IBR, PAYE, and REPAYE.

Strategies for Managing Student Loan Debt

- Create a Budget: Track income and expenses to determine how much can be allocated towards student loan repayment.

- Prioritize High-Interest Loans: Focus on repaying loans with the highest interest rates first to minimize the total interest paid.

- Consider Refinancing: If eligible, refinancing student loans with a lower interest rate can reduce monthly payments and the overall cost of borrowing. However, carefully compare offers and consider the implications of losing federal loan benefits.

- Explore Loan Forgiveness Programs: Research and determine eligibility for any loan forgiveness programs applicable to your situation.

- Communicate with Your Loan Servicer: Stay in contact with your loan servicer to address any issues and explore options for managing your debt.

The Impact of Income-Driven Repayment Plans

IDR plans offer significant flexibility, adjusting monthly payments based on income and family size. While this reduces short-term financial burden, it often extends the repayment period, leading to significantly higher total interest paid over the life of the loan. Borrowers should carefully weigh the short-term benefits against the long-term costs before choosing an IDR plan.

Potential for Loan Forgiveness Programs

Several loan forgiveness programs exist, targeting specific professions (e.g., teachers, public service workers) or circumstances (e.g., disability, death). The eligibility requirements for these programs are often complex and change over time, so careful research and consultation with a financial advisor are recommended.

Frequently Asked Questions (FAQ)

-

Q: What is the average monthly student loan payment in the US? A: There is no single average due to the diverse factors influencing individual payments. The average varies considerably depending on loan amount, interest rates, and repayment plans.

-

Q: How can I calculate my monthly student loan payment? A: Most loan servicers provide online calculators to estimate monthly payments based on your specific loan terms.

-

Q: What happens if I miss student loan payments? A: Missed payments can lead to late fees, damage your credit score, and eventually result in loan default, which has serious financial consequences.

-

Q: Can I consolidate my student loans? A: Consolidating multiple loans into a single loan can simplify repayment, but it may not always lower your monthly payment or total interest paid.

Practical Tips: Maximizing the Benefits of Understanding Your Student Loan Payments

-

Understand Your Loan Terms: Carefully review all loan documents to understand the interest rates, repayment periods, and other terms and conditions.

-

Explore Repayment Options: Compare different repayment plans to determine which best fits your financial situation and long-term goals.

-

Budget for Repayment: Allocate a specific amount in your budget for student loan repayment, prioritizing this expense.

-

Monitor Your Credit Score: Regularly check your credit score to ensure that your student loan payments are not negatively impacting your creditworthiness.

-

Seek Professional Advice: Consider consulting a financial advisor for personalized guidance on managing your student loan debt.

Final Conclusion: Navigating the Path to Student Loan Repayment

The average monthly student loan payment remains a complex and highly variable figure. However, by understanding the key factors that influence these payments and exploring various repayment options, borrowers can develop effective strategies to manage their debt responsibly and achieve financial well-being. Proactive planning, budgeting, and communication with loan servicers are crucial steps in navigating this significant financial challenge. Remember, your individual circumstances determine your payment, and seeking personalized guidance when necessary is always a smart move.

Latest Posts

Latest Posts

-

Money Management Saham

Apr 06, 2025

-

How To Set Up Money Management

Apr 06, 2025

-

How To Start Managing Money

Apr 06, 2025

-

Money Management Companies

Apr 06, 2025

-

How To Start A Money Management Business

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about What's The Average Monthly Payment For Student Loans . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.