What Determines Minimum Payment Credit Card

adminse

Apr 05, 2025 · 8 min read

Table of Contents

Unlocking the Mystery: What Determines Your Minimum Credit Card Payment?

What if your understanding of minimum credit card payments could save you hundreds, even thousands, of dollars in interest? This seemingly simple figure holds the key to responsible credit management and financial freedom.

Editor’s Note: This article on minimum credit card payments was published today, providing you with the most up-to-date information and strategies for managing your credit card debt effectively.

Why Minimum Credit Card Payments Matter: Relevance, Practical Applications, and Industry Significance

Understanding your minimum credit card payment is crucial for several reasons. It directly impacts your debt repayment timeline, the total interest you pay, and ultimately, your credit score. Failing to grasp this fundamental aspect of credit card management can lead to a cycle of debt that's difficult to escape. The implications extend beyond individual finances; understanding minimum payment structures helps consumers make informed decisions about credit card usage and selection. This knowledge empowers consumers to negotiate better terms and avoid costly financial pitfalls.

Overview: What This Article Covers

This article comprehensively explores the factors determining minimum credit card payments, dissecting the calculation methods employed by issuers. We'll delve into the implications of only paying the minimum, explore strategies for accelerated debt repayment, and discuss how minimum payment calculations differ across various credit card types. Finally, we'll address frequently asked questions and provide practical tips for effective credit card management.

The Research and Effort Behind the Insights

This article draws upon extensive research, incorporating information from leading financial institutions, consumer protection agencies, and reputable financial publications. Data analysis on various credit card agreements and repayment structures has been undertaken to ensure accuracy and provide readers with a well-rounded understanding of minimum payment calculations.

Key Takeaways:

- Definition and Core Concepts: A clear explanation of minimum credit card payments and the underlying principles governing their calculation.

- Calculation Methods: A detailed breakdown of the various methods used by credit card issuers to determine minimum payments.

- Impact of Minimum Payments: Analysis of the long-term financial consequences of only making minimum payments.

- Strategies for Accelerated Repayment: Practical strategies to pay down credit card debt faster and reduce overall interest costs.

- Minimum Payment Differences Across Card Types: Examination of how minimum payment calculations vary depending on the type of credit card.

Smooth Transition to the Core Discussion

Now that we've established the importance of understanding minimum credit card payments, let's explore the intricacies of their determination. We'll examine the factors influencing these calculations and their profound impact on your financial well-being.

Exploring the Key Aspects of Minimum Credit Card Payments

1. Definition and Core Concepts:

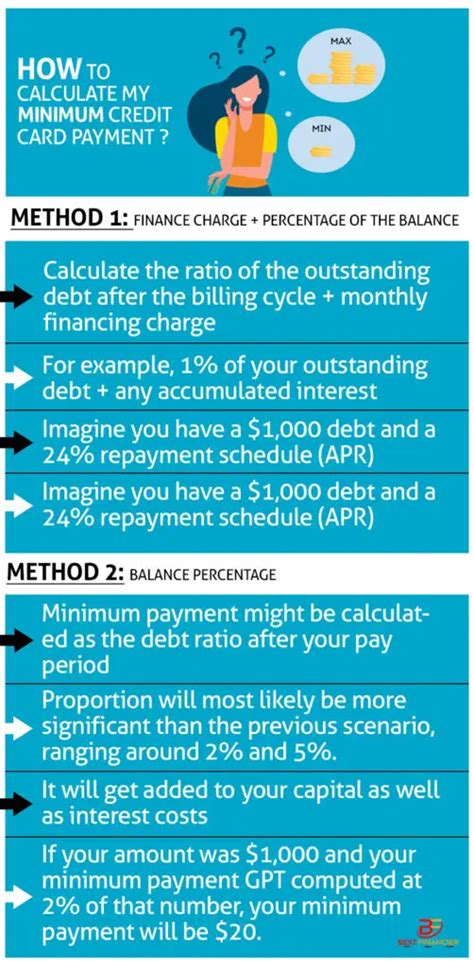

The minimum payment on a credit card is the smallest amount you can pay each month to avoid late fees and maintain your account in good standing. It's usually a percentage of your outstanding balance (often 1-3%), but it can also include a minimum dollar amount, whichever is greater. Importantly, this payment only covers a portion of your balance; the remaining amount accrues interest.

2. Calculation Methods:

Credit card issuers employ various methods to calculate minimum payments. The most common is a percentage of the outstanding balance, typically ranging from 1% to 3%. This percentage can vary depending on the issuer, the type of credit card, and the cardholder's credit history. However, many issuers also incorporate a minimum dollar amount into the calculation. This means even if the percentage-based minimum is less than a certain dollar amount (e.g., $25), the minimum payment will be that higher dollar amount. The goal is to ensure that the minimum payment is not excessively low, even for low balances.

3. Applications Across Industries:

The calculation of minimum payments is consistent across the credit card industry, though the specific percentages and minimum dollar amounts may differ. However, variations can occur based on the type of card:

- Secured Credit Cards: These cards usually have a higher minimum payment requirement to mitigate risk.

- Rewards Credit Cards: Minimum payments for these cards follow the standard calculation methods but may be impacted by promotional periods or balance transfers.

- Business Credit Cards: Minimum payments might be higher to reflect the higher credit limits and potential business expenses.

4. Challenges and Solutions:

The biggest challenge associated with minimum payments is the slow pace of debt repayment. Paying only the minimum keeps the debt perpetually growing due to accrued interest. This leads to a cycle of debt that can be difficult to break. The solution is to pay more than the minimum each month, accelerating repayment and saving on interest charges.

5. Impact on Innovation:

Financial technology (FinTech) companies are constantly innovating to provide consumers with better tools for managing their credit card debt. Apps and online platforms provide detailed breakdowns of minimum payments, interest accrual, and projected repayment timelines. They frequently offer debt reduction strategies, empowering consumers to make informed decisions.

Closing Insights: Summarizing the Core Discussion

Understanding your minimum credit card payment is not just about avoiding late fees; it's a fundamental aspect of financial literacy. Failing to pay more than the minimum can lead to significant long-term costs. By understanding the calculation methods and embracing proactive repayment strategies, individuals can take control of their debt and avoid the pitfalls of perpetual minimum payments.

Exploring the Connection Between Interest Rates and Minimum Credit Card Payments

The interest rate on your credit card significantly impacts your minimum payment calculation and the overall cost of carrying a balance. Higher interest rates mean more interest accrues each month, potentially leading to a higher minimum payment (if the percentage-based minimum exceeds the minimum dollar amount). This section examines this pivotal relationship.

Key Factors to Consider:

Roles and Real-World Examples: A card with a 20% APR will accrue significantly more interest than a card with a 10% APR, making the minimum payment more substantial over time. For instance, if you have a $1,000 balance on a card with a 20% APR and a 2% minimum payment, your minimum payment will be $20. However, a significant portion of that $20 goes towards interest, leaving a small amount to reduce your principal balance.

Risks and Mitigations: The major risk is the snowball effect of accruing interest. The longer you pay only the minimum, the more interest you pay, extending your repayment timeline indefinitely. Mitigation strategies include aggressively paying down the balance, transferring to a card with a lower APR, or consolidating debt.

Impact and Implications: The long-term financial impact of high interest rates combined with minimum payments is considerable. It can trap individuals in a cycle of debt, limiting their financial opportunities.

Conclusion: Reinforcing the Connection

The relationship between interest rates and minimum payments is inextricably linked. Higher interest rates amplify the negative consequences of paying only the minimum, accelerating debt accumulation. By understanding this dynamic, consumers can make informed decisions about credit card selection and debt repayment strategies.

Further Analysis: Examining Interest Calculation Methods in Greater Detail

Credit card interest is typically calculated using the average daily balance method. This involves calculating the daily balance over the billing cycle and averaging it to determine the interest charged. This method ensures fairness, even if your balance fluctuates throughout the month. Some issuers may use other methods, such as the previous balance method or the adjusted balance method, but the average daily balance method is most prevalent.

FAQ Section: Answering Common Questions About Minimum Credit Card Payments

Q: What happens if I only pay the minimum payment? A: You'll avoid late fees, but you'll pay significantly more in interest over time, extending your repayment period considerably.

Q: Can my minimum payment change? A: Yes, it can change based on your outstanding balance and the card issuer's policies. It may increase if your balance goes up.

Q: Is it always better to pay more than the minimum? A: Absolutely. Paying more than the minimum significantly reduces the total interest paid and accelerates debt repayment.

Q: What if I can't afford the minimum payment? A: Contact your credit card issuer immediately. They may offer hardship programs or payment plans to help you manage your debt.

Practical Tips: Maximizing the Benefits of Responsible Credit Card Management

- Budgeting: Create a realistic budget that accounts for all expenses, including your credit card payments.

- Track Spending: Monitor your credit card spending closely to avoid overspending and accumulating unnecessary debt.

- Pay More Than Minimum: Always pay more than the minimum payment to reduce interest and shorten your repayment period.

- Explore Debt Consolidation: If you have multiple credit cards, consider consolidating your debt into a single loan with a lower interest rate.

- Consider Balance Transfers: Transferring your balance to a card with a 0% introductory APR can help you pay down your debt faster.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding the factors determining your minimum credit card payment is paramount for responsible financial management. While minimum payments prevent late fees, relying on them indefinitely leads to substantial long-term costs. By actively managing your debt, paying more than the minimum, and employing strategic repayment methods, you can achieve financial freedom and avoid the pitfalls of accumulating debt. Remember, responsible credit card usage is key to building a strong financial future.

Latest Posts

Latest Posts

-

What Happens If You Pay More Than The Minimum Payment On A Credit Card

Apr 06, 2025

-

What Happens If You Pay Less Than Your Minimum Payment

Apr 06, 2025

-

What Happens If You Pay More Than The Minimum Payment

Apr 06, 2025

-

What Is A Money Market Account Vs Hysa

Apr 06, 2025

-

What Is A Money Market Account Minimum Balance

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about What Determines Minimum Payment Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.