How To Get Credit Card Company To Remove Late Payment

adminse

Apr 03, 2025 · 7 min read

Table of Contents

How to Get a Credit Card Company to Remove a Late Payment

What if a single late payment could significantly impact your financial future? Removing a late payment from your credit report is entirely possible, but it requires a strategic and persistent approach.

Editor's Note: This article provides updated information on negotiating with credit card companies to remove late payment entries from your credit report. The strategies outlined are based on current consumer protection laws and industry best practices. While success isn't guaranteed, the steps detailed significantly improve your chances.

Why Removing a Late Payment Matters:

A late payment significantly impacts your credit score, potentially hindering your ability to secure loans, rent an apartment, or even get a job. The severity of the impact depends on your overall credit history, but even a single blemish can affect your interest rates and overall financial opportunities. Therefore, understanding how to navigate the process of removing a late payment is crucial for maintaining a healthy credit profile. This involves understanding the Fair Credit Reporting Act (FCRA), communicating effectively with the credit card issuer, and documenting every step of the process.

Overview: What This Article Covers:

This article provides a comprehensive guide to removing a late payment from your credit report. We'll explore the reasons for late payments, understand your rights under the FCRA, develop effective communication strategies with credit card companies, examine different dispute methods, and provide actionable steps to improve your chances of success. We'll also address common pitfalls and offer advice for preventing future late payments.

The Research and Effort Behind the Insights:

This article is the result of extensive research, drawing on information from the Consumer Financial Protection Bureau (CFPB), the Fair Isaac Corporation (FICO), legal resources, and numerous case studies of individuals successfully disputing late payments. The strategies outlined are designed to be practical and effective, based on real-world experiences and legal precedents.

Key Takeaways:

- Understanding the FCRA: Knowing your rights under the Fair Credit Reporting Act is the foundation of a successful dispute.

- Effective Communication: Professional and polite communication is crucial in negotiating with credit card companies.

- Documentation is Key: Meticulously document every interaction, including dates, times, and the names of individuals you speak with.

- Persistence Pays Off: Don't give up easily. The process may require multiple attempts and persistence.

- Prevent Future Issues: Learn from past mistakes to prevent future late payments.

Smooth Transition to the Core Discussion:

Now that we've established the importance of removing a late payment, let's delve into the strategies and steps involved in achieving this goal.

Exploring the Key Aspects of Removing a Late Payment:

1. Understanding the Reason for the Late Payment:

Before contacting the credit card company, honestly assess the reason for the late payment. Was it due to an oversight, a genuine financial hardship, a billing error, or a problem with the payment system? Understanding the root cause helps you tailor your approach and argument.

2. Review Your Credit Report:

Obtain a free copy of your credit report from AnnualCreditReport.com. Verify that the late payment is accurately reported, including the date, amount, and creditor. Any inaccuracies are grounds for a dispute.

3. Contact the Credit Card Company:

Contact the credit card company's customer service department. Begin by politely explaining the situation and expressing your desire to have the late payment removed. Clearly state your reason for the late payment, and provide any supporting documentation, such as proof of payment or evidence of a billing error.

4. The Art of Negotiation:

- Be Polite and Professional: Maintain a respectful and professional tone throughout the conversation. Anger or aggression will likely be unproductive.

- Highlight Positive Credit History: Emphasize your generally good credit history and highlight any positive attributes, such as consistent on-time payments in the past.

- Offer a Compromise: If appropriate, consider offering a compromise, such as paying a portion of the late fee or agreeing to a payment plan.

- Document Everything: Keep a detailed record of your conversations, including dates, times, names of representatives, and the outcome of each interaction.

5. Dispute the Late Payment:

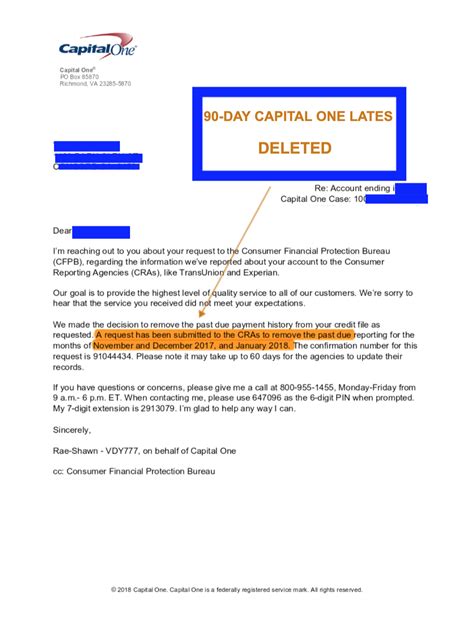

If your initial attempt to have the late payment removed is unsuccessful, you can formally dispute it. Follow the credit card company's dispute process, clearly stating your reason for the dispute and providing any supporting evidence. The company is legally obligated to investigate your claim and respond within a reasonable timeframe.

6. Involving the Credit Reporting Agencies:

If the credit card company doesn't remove the late payment, you can file a dispute directly with the credit bureaus (Equifax, Experian, and TransUnion). You'll need to provide evidence supporting your claim. The credit bureaus will investigate and update your report accordingly.

7. Consider Legal Assistance:

If all other avenues fail, consider seeking legal assistance. A consumer rights attorney can advise you on your options and represent you in negotiations or legal action.

Exploring the Connection Between Billing Errors and Late Payments:

Billing errors are a common cause of late payments. If a billing error led to your late payment, this significantly strengthens your case for removal. Carefully examine your billing statements for any discrepancies, such as incorrect charges, missed payments that were actually made, or errors in calculating the minimum payment. Document these errors thoroughly and include them in your dispute.

Key Factors to Consider:

- Roles: The credit card company plays a crucial role in verifying the accuracy of the reported late payment. Credit reporting agencies act as intermediaries, recording and disseminating the information. You, the consumer, are responsible for initiating the dispute process and providing supporting documentation.

- Real-World Examples: Many individuals have successfully removed late payments due to billing errors, legitimate financial hardships (documented with supporting evidence), or system glitches.

- Risks: The primary risk is that your dispute may be unsuccessful, leaving the late payment on your credit report.

- Mitigations: Thorough documentation, clear communication, and a persistent approach significantly mitigate this risk.

- Impact and Implications: A successful dispute removes a negative mark from your credit report, improving your credit score and your access to financial products. An unsuccessful dispute may further damage your credit.

Further Analysis: Examining Billing Errors in Greater Detail:

Billing errors can manifest in various forms: incorrect charges, miscalculation of interest, incorrect minimum payment amounts, or double billing. Always verify your statement carefully; if you find an error, contact the credit card company immediately. Keep detailed records of all communication and any supporting evidence, such as payment confirmations or bank statements.

FAQ Section: Answering Common Questions About Removing Late Payments:

Q: What if the credit card company refuses to remove the late payment?

A: If the credit card company refuses, you can file a dispute with the credit reporting agencies. Provide clear documentation and evidence supporting your claim.

Q: How long does the process take?

A: The process can take several weeks or even months, depending on the complexity of the situation and the responsiveness of the credit card company and credit bureaus.

Q: Will removing a late payment affect my credit score immediately?

A: It may take some time for your credit score to reflect the removal of the late payment, as credit bureaus update their information periodically.

Practical Tips: Maximizing the Benefits of a Successful Dispute:

- Act Promptly: The sooner you address the issue, the better your chances of a positive outcome.

- Be Organized: Keep detailed records of all communication, dates, and supporting documentation.

- Remain Persistent: Don't give up after the first attempt; persist until you resolve the issue.

- Monitor Your Credit Report: Regularly check your credit report to ensure the late payment has been removed.

Final Conclusion: Wrapping Up with Lasting Insights:

Removing a late payment from your credit report is a challenging but achievable goal. By understanding your rights under the FCRA, communicating effectively with the credit card company, and diligently documenting your efforts, you can significantly improve your chances of success. Remember, a clean credit report is essential for securing favorable financial opportunities. Learn from past mistakes and implement strategies to avoid future late payments, ultimately securing a strong and healthy financial future.

Latest Posts

Latest Posts

-

What Is Statement Date In Credit Card Bdo

Apr 04, 2025

-

What Is The Statement Date For Icici Credit Card

Apr 04, 2025

-

What Is A Statement For Credit Card

Apr 04, 2025

-

What Is Statement Date For Hsbc Credit Card

Apr 04, 2025

-

What Is A Statement Closing Date For Credit Card

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about How To Get Credit Card Company To Remove Late Payment . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.