What Is A Statement For Credit Card

adminse

Apr 04, 2025 · 8 min read

Table of Contents

Understanding Credit Card Statements: Your Guide to Financial Clarity

What if navigating your credit card statement was as easy as making a purchase? Understanding this seemingly simple document is key to responsible credit management and building a strong financial future.

Editor’s Note: This article on credit card statements was published today to provide you with the most up-to-date information on deciphering this crucial financial document. We'll break down every section, empowering you to confidently manage your credit card finances.

Why Credit Card Statements Matter: Relevance, Practical Applications, and Industry Significance

Credit card statements are more than just a record of your spending; they're a critical tool for managing your finances and creditworthiness. They provide a detailed summary of your credit card activity, allowing you to track expenses, identify potential errors, and monitor your credit utilization – a key factor influencing your credit score. Ignoring or misunderstanding your statement can lead to late payment fees, higher interest charges, and ultimately, damage to your credit health. Understanding your statement is crucial for budgeting, avoiding debt, and building a positive credit history. This knowledge empowers you to negotiate better interest rates, qualify for loans, and make informed financial decisions. Furthermore, recognizing discrepancies or fraudulent activity early is essential to protecting your financial well-being.

Overview: What This Article Covers

This article provides a comprehensive guide to understanding your credit card statement. We'll dissect each section, explain common terms, discuss how to identify and address errors, and offer practical tips for using your statement to effectively manage your finances. We'll also explore how statement information impacts your credit score and how to use this knowledge to your advantage.

The Research and Effort Behind the Insights

This article draws upon extensive research, incorporating information from reputable financial institutions, consumer protection agencies, and credit reporting bureaus. We've analyzed numerous sample statements from different credit card providers to present a generalized, yet accurate, representation of the information contained within. The goal is to provide clear, concise, and actionable insights that will benefit readers of all financial backgrounds.

Key Takeaways:

- Definition and Core Concepts: A detailed explanation of credit card statements and their components.

- Practical Applications: How to use statement information for budgeting, debt management, and credit monitoring.

- Challenges and Solutions: Addressing errors, disputes, and understanding interest calculations.

- Future Implications: How statement data impacts long-term financial health and creditworthiness.

Smooth Transition to the Core Discussion

Now that we've established the importance of understanding your credit card statement, let's delve into its key components and explore how to effectively utilize this information.

Exploring the Key Aspects of Credit Card Statements

A typical credit card statement is organized into distinct sections, each providing essential information about your account activity. Let's examine these sections individually:

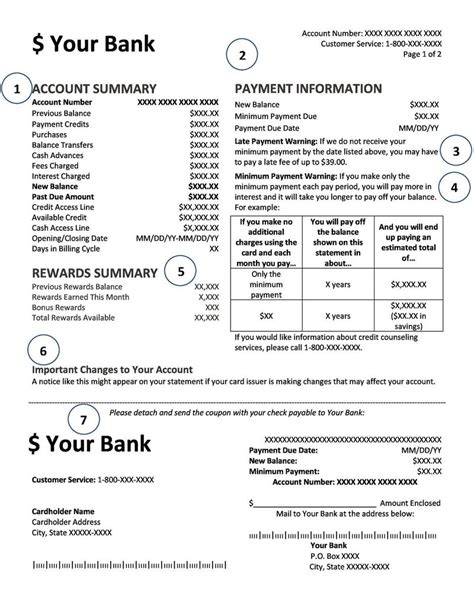

1. Account Information: This section displays your account number, the billing cycle period (the dates between which transactions are included), and the statement date (the date the statement was generated). It also includes your name and address as registered with the credit card company. Accurately reviewing this information ensures that the statement belongs to you and that your contact details are up-to-date.

2. Previous Balance: This represents the outstanding balance from your previous billing cycle. Understanding this figure is critical as it forms the basis for calculating your current balance and interest charges.

3. Payments: This section details any payments you made during the billing cycle. This includes the payment date, the amount paid, and the payment method used (e.g., online payment, check, etc.). Verify this section carefully to ensure all your payments have been accurately recorded.

4. Purchases: This is arguably the most important section of your statement. It lists all purchases made during the billing cycle, including the date of the transaction, the merchant name, and the amount spent. Reviewing this section meticulously allows you to reconcile your own records with the credit card company's records, identifying any discrepancies or unauthorized charges.

5. Credits: This section lists any credits applied to your account during the billing cycle. Credits can arise from various reasons, such as returns, adjustments, or promotional offers.

6. Fees: This section outlines any fees charged during the billing cycle. These fees might include late payment fees, over-limit fees, balance transfer fees, or foreign transaction fees. Carefully examine this section to understand the reasons behind any fees and ensure they are legitimate.

7. Interest Charges: This crucial section calculates the interest charged on your outstanding balance. The interest rate is typically expressed as an Annual Percentage Rate (APR), and the calculation method (e.g., average daily balance method) should be clearly stated. Understanding how interest is calculated helps you manage your debt effectively and avoid accumulating excessive interest charges.

8. Current Balance: This is the total amount you owe at the end of the billing cycle. It includes your previous balance, plus new purchases and fees, minus payments and credits. This is the amount you need to pay to avoid late payment fees and further interest charges.

9. Minimum Payment Due: This is the minimum amount you are required to pay by the due date to avoid late payment fees. While making only the minimum payment may seem convenient, it will significantly prolong the repayment period and result in a larger total interest paid.

Closing Insights: Summarizing the Core Discussion

Your credit card statement provides a comprehensive overview of your spending habits and financial responsibilities. By understanding each section and diligently reviewing the information, you can gain invaluable insights into your financial health.

Exploring the Connection Between Credit Utilization and Credit Card Statements

Credit utilization is the percentage of your available credit that you're currently using. Your credit card statement plays a crucial role in determining your credit utilization ratio. A high credit utilization ratio (generally above 30%) can negatively impact your credit score, while a low ratio (generally below 30%) demonstrates responsible credit management. Your statement allows you to easily calculate your credit utilization by dividing your current balance by your credit limit. This information is essential for maintaining a healthy credit score.

Key Factors to Consider:

- Roles and Real-World Examples: High credit utilization, as reflected in your statement, can lead to higher interest rates and decreased credit score. Conversely, a low credit utilization ratio demonstrates responsible credit management and can improve your creditworthiness.

- Risks and Mitigations: Failing to monitor credit utilization, as evidenced by overlooking your statement, can lead to financial difficulties and damage to your credit score. Regularly checking your statement and paying down your balance proactively are key mitigation strategies.

- Impact and Implications: Long-term high credit utilization can make it difficult to secure loans, rent an apartment, or even obtain certain jobs. Maintaining a low credit utilization ratio, as monitored through your statement, is crucial for building a strong financial future.

Conclusion: Reinforcing the Connection

The connection between your credit card statement and credit utilization is undeniable. Your statement provides the essential data to monitor your credit utilization and manage your credit effectively.

Further Analysis: Examining Credit Scores in Greater Detail

Your credit score is a numerical representation of your creditworthiness, heavily influenced by your credit utilization (as seen on your statement), payment history, length of credit history, and the mix of credit accounts you hold. A higher credit score typically translates to lower interest rates on loans and credit cards, making it easier to obtain financing. Your statement contributes significantly to maintaining a healthy credit score.

FAQ Section: Answering Common Questions About Credit Card Statements

- What is a credit card statement? A credit card statement is a monthly summary of your credit card activity, detailing purchases, payments, fees, and interest charges.

- How often do I receive a credit card statement? Most credit card companies issue statements monthly.

- What if I don't receive my statement? Contact your credit card issuer immediately if you don't receive your statement by the expected date.

- What should I do if I see an error on my statement? Contact your credit card company immediately to report the error and request a correction.

- How can I improve my credit score based on my statement? Keep your credit utilization low, pay your bills on time, and maintain a positive payment history.

Practical Tips: Maximizing the Benefits of Your Credit Card Statement

- Review your statement thoroughly: Check every transaction to ensure accuracy and identify any unauthorized charges.

- Keep track of your spending: Use your statement to monitor your spending habits and identify areas where you can reduce expenses.

- Pay more than the minimum payment: Paying more than the minimum payment will reduce your interest charges and help you pay off your debt faster.

- Pay your bills on time: Late payments negatively impact your credit score.

- Keep your credit utilization low: Aim to keep your credit utilization below 30% to maintain a healthy credit score.

- Understand your interest rate: Know your APR to accurately estimate interest charges and plan your repayments.

Final Conclusion: Wrapping Up with Lasting Insights

Your credit card statement is a powerful tool for managing your finances and building a strong credit history. By understanding its contents and using the information effectively, you can take control of your spending, manage your debt, and improve your overall financial health. Regularly reviewing your statement is not merely a financial chore, but a proactive step toward achieving long-term financial success.

Latest Posts

Latest Posts

-

How Does The Minimum Wage Go Up

Apr 05, 2025

-

What Would The Minimum Payment Be On A Credit Card

Apr 05, 2025

-

What Is The Minimum Payment On A 3000 Credit Card

Apr 05, 2025

-

Finance In Administration

Apr 05, 2025

-

Importance Of Administrative Law

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about What Is A Statement For Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.