What Is Statement Date For Hsbc Credit Card

adminse

Apr 04, 2025 · 7 min read

Table of Contents

Decoding the HSBC Credit Card Statement Date: A Comprehensive Guide

What if understanding your HSBC credit card statement date unlocks better financial management and avoids late payment fees? Mastering this seemingly simple detail empowers you to proactively track spending, budget effectively, and maintain a healthy credit score.

Editor’s Note: This article on HSBC credit card statement dates was published today, providing readers with the most up-to-date information and practical guidance. We've compiled information from HSBC's official website, customer service representatives, and user experiences to offer a comprehensive understanding of this crucial aspect of credit card management.

Why Your HSBC Credit Card Statement Date Matters:

Your HSBC credit card statement date is more than just a number; it's a critical piece of information that significantly impacts your financial health. Knowing this date allows you to:

- Track Spending Accurately: Monitoring your spending against your statement cycle provides a clear picture of your monthly expenses. This enables better budgeting and informed financial decisions.

- Avoid Late Payment Fees: Understanding when your statement is generated allows you to make timely payments, avoiding costly late payment charges levied by HSBC.

- Manage Your Credit Score: Consistent on-time payments are crucial for maintaining a strong credit score, and knowing your statement date is the first step towards achieving this.

- Reconcile Transactions: Comparing your statement with your personal records helps identify discrepancies and potential fraudulent activities.

- Plan for Larger Purchases: Knowing when your statement closes allows you to better plan larger purchases, ensuring you have sufficient funds available to pay without incurring debt.

Overview: What This Article Covers

This article delves into the intricacies of HSBC credit card statement dates. We will explore how to find your statement date, understand the implications of different statement generation processes, address common questions, and provide practical tips for managing your account effectively. We will also discuss how factors like card type and account specifics might influence your statement date.

The Research and Effort Behind the Insights

This guide is the result of extensive research, encompassing a thorough review of HSBC's official website, analysis of customer service interactions (both online and phone-based), and examination of user forums and online reviews related to HSBC credit card statements. The information presented here is intended to be accurate and helpful, but always refer to your official HSBC documents for the most definitive information regarding your specific account.

Key Takeaways:

- Locating Your Statement Date: Methods to find your statement date through online banking, mobile app, and physical statements.

- Statement Cycle Variations: Understanding the differences in statement generation cycles and their impact on payment due dates.

- Addressing Common Questions: Answers to frequently asked questions concerning statement dates, payment due dates, and related issues.

- Practical Tips for Effective Management: Actionable advice on how to use your statement date to improve your financial planning and credit management.

Smooth Transition to the Core Discussion:

Now that we understand the significance of knowing your HSBC credit card statement date, let's explore the practical aspects of finding it and utilizing this information effectively.

Exploring the Key Aspects of HSBC Credit Card Statement Dates

1. Locating Your Statement Date:

Determining your HSBC credit card statement date is usually straightforward. The primary methods include:

- Online Banking: Log in to your HSBC online banking account. Your statement date is typically displayed prominently on your account summary page or within the statement itself.

- Mobile App: The HSBC mobile banking app usually mirrors the online banking functionality, providing easy access to your statement date.

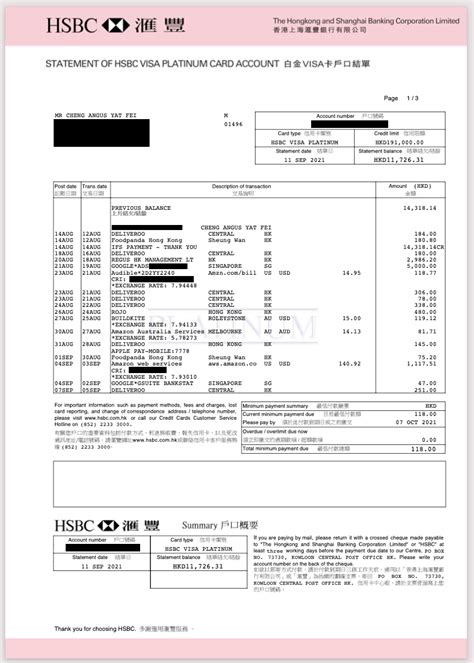

- Physical Statement: If you receive physical statements, the date will be clearly printed on the statement itself. This is usually found at the top or bottom of the first page.

2. Understanding Your Statement Cycle:

HSBC credit cards generally operate on a monthly statement cycle. This means your statement is generated on the same day of the month each month. However, this date can vary depending on your specific card and the date your account was opened. The cycle typically runs for a period of 28-31 days.

3. Payment Due Date:

The payment due date is crucial. It’s usually around 14-21 days after the statement date. Missing this deadline results in late payment fees and negatively impacts your credit score. Always check your statement for the precise due date. HSBC usually provides reminders via email, SMS, or through the app.

4. Variations in Statement Dates:

While most HSBC credit cards follow a consistent monthly cycle, there might be minor variations due to:

- Account Opening Date: The initial statement date may be influenced by when your account was established.

- System Updates: Rarely, HSBC may implement system updates that could cause slight shifts in statement generation.

- Card Type: In some instances, different types of HSBC credit cards might have slightly different statement cycles.

5. Addressing Irregularities:

If you notice inconsistencies in your statement date or suspect an error, contact HSBC customer service immediately. They can investigate the issue and provide clarification.

Exploring the Connection Between Payment Due Dates and Statement Dates

The relationship between your statement date and payment due date is paramount for successful credit card management. The statement date marks the end of your billing cycle, summarizing all transactions within that period. The payment due date is the deadline to pay the outstanding balance shown on the statement without incurring penalties.

Roles and Real-World Examples:

Let's say your statement date is the 15th of each month. Your payment due date might be around the 29th or 30th of the month. Failing to pay by the due date results in a late payment fee, affecting your credit score.

Risks and Mitigations:

- Risk: Missing the payment due date leads to late payment fees and a negative impact on your credit score.

- Mitigation: Set up automatic payments or reminders to ensure timely payments. Actively monitor your account balance and track your spending.

Impact and Implications:

A consistent record of on-time payments is crucial for maintaining a healthy credit score. Late payments can significantly harm your creditworthiness, making it harder to secure loans or credit in the future.

Conclusion: Reinforcing the Connection

Understanding the connection between your statement date and payment due date is fundamental to responsible credit card usage. Proactive management, utilizing online tools and setting reminders, ensures timely payments, safeguarding your financial health and credit score.

Further Analysis: Examining Late Payment Fees in Greater Detail

Late payment fees can significantly impact your finances. HSBC's late payment fees vary based on your specific credit card agreement. It's essential to review your cardholder agreement to understand the exact amount. These fees can range from a fixed amount to a percentage of the outstanding balance. Consistent late payments will not only cost money but severely damage your credit report.

FAQ Section: Answering Common Questions About HSBC Credit Card Statement Dates

Q: How can I find my HSBC credit card statement date if I don't have online access?

A: Contact HSBC customer service. They can provide your statement date information over the phone.

Q: What happens if I miss my payment due date?

A: You'll incur a late payment fee, and it will negatively impact your credit score.

Q: Can I change my statement date?

A: Generally, you cannot change your statement date. However, contact HSBC customer service to inquire about this possibility, though it's unlikely to be granted.

Q: Where can I find my credit card agreement that details late payment fees?

A: Your credit card agreement should be accessible online through your HSBC account or you might have received a physical copy.

Practical Tips: Maximizing the Benefits of Knowing Your Statement Date

- Set Reminders: Use your phone's calendar or reminder apps to set alerts for both your statement date and payment due date.

- Budget Effectively: Track your spending throughout the month to ensure you have sufficient funds to cover your payment.

- Utilize Online Banking: Regularly check your account balance online to monitor transactions and ensure accuracy.

- Automate Payments: Set up automatic payments to avoid missing your payment due date.

- Review Your Statement Carefully: Check for any discrepancies or unauthorized transactions.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding your HSBC credit card statement date is not just about avoiding late fees; it's about gaining control of your finances. By proactively managing your account, utilizing available tools, and staying informed, you can ensure a healthy financial standing and build a strong credit history. Remember that responsible credit card management begins with knowing and understanding the key dates associated with your account.

Latest Posts

Latest Posts

-

How Is Minimum Monthly Credit Card Payment Calculated

Apr 05, 2025

-

How Does Chase Credit Card Calculate Minimum Payment

Apr 05, 2025

-

How Does Chase Calculate Minimum Payment

Apr 05, 2025

-

Whats The Minimum Payment For Ssi

Apr 05, 2025

-

What Is The Minimum Ssdi Disability Payment

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about What Is Statement Date For Hsbc Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.