How Do Credit Card Companies Calculate Your Minimum Payment

adminse

Apr 04, 2025 · 9 min read

Table of Contents

Decoding the Mystery: How Credit Card Companies Calculate Your Minimum Payment

What if understanding your credit card minimum payment calculation could save you thousands of dollars in interest? This seemingly simple figure holds the key to responsible credit card management and avoiding a debt spiral.

Editor’s Note: This article on credit card minimum payment calculations was published [Date]. We've compiled information from leading financial institutions, consumer protection agencies, and industry experts to provide you with a clear and accurate understanding of this crucial aspect of credit card management.

Why Understanding Your Minimum Payment Matters:

The minimum payment on your credit card statement might seem insignificant, a small amount easily overlooked. However, relying solely on minimum payments can have significant long-term financial consequences. Understanding how these payments are calculated allows you to make informed decisions about debt repayment, potentially saving you substantial amounts in interest charges and accelerating your journey to financial freedom. This knowledge empowers you to budget effectively, avoid late fees, and improve your credit score.

Overview: What This Article Covers:

This article delves into the intricacies of credit card minimum payment calculations. We will explore the different methods used by credit card issuers, the factors that influence the calculation, the hidden costs of minimum payments, and strategies for more effective debt management. We will also examine the impact of minimum payments on your credit score and offer practical tips for responsible credit card usage.

The Research and Effort Behind the Insights:

This article is the result of extensive research, drawing upon publicly available information from major credit card companies, the Consumer Financial Protection Bureau (CFPB), and reputable financial websites. We have analyzed various credit card agreements and consulted expert opinions to ensure accuracy and provide a comprehensive overview of minimum payment calculations.

Key Takeaways:

- Definition and Core Concepts: A clear explanation of minimum payment and its role in credit card repayment.

- Calculation Methods: An in-depth look at the different formulas used by credit card companies.

- Factors Influencing Minimum Payment: Understanding the variables that affect the minimum amount due.

- Hidden Costs of Minimum Payments: The long-term financial implications of only making minimum payments.

- Strategies for Effective Debt Repayment: Alternative payment strategies to accelerate debt reduction.

- Impact on Credit Score: How minimum payment behavior affects your creditworthiness.

- Practical Tips for Responsible Credit Card Use: Actionable advice for managing your credit effectively.

Smooth Transition to the Core Discussion:

Now that we understand the importance of understanding minimum payment calculations, let's dive into the specifics of how credit card companies determine this crucial figure.

Exploring the Key Aspects of Credit Card Minimum Payment Calculation:

1. Definition and Core Concepts:

The minimum payment is the smallest amount you are required to pay on your credit card statement each month to avoid late fees and maintain your account in good standing. It's crucial to remember that this is the minimum required; paying only the minimum does not mean you're paying off your debt efficiently.

2. Calculation Methods:

There isn't a single universal formula for calculating minimum payments. Credit card companies typically use one of the following methods, or a combination thereof:

-

Percentage of Outstanding Balance: This is the most common method. The minimum payment is calculated as a percentage of your outstanding balance (the amount you owe). This percentage typically ranges from 1% to 3%, though some cards might have higher or lower percentages depending on the card's terms and conditions. For example, if your outstanding balance is $1,000 and the minimum payment percentage is 2%, your minimum payment would be $20.

-

Fixed Minimum Payment: Some credit card companies might have a fixed minimum payment amount, regardless of the balance. This is less common and usually applies to cards with lower credit limits.

-

Combination Method: Some issuers might combine the percentage-based method with a fixed minimum. For example, the minimum payment might be the greater of 1% of the outstanding balance or a fixed amount like $25.

3. Factors Influencing Minimum Payment:

Several factors can influence the calculated minimum payment, even if the same calculation method is used:

- Outstanding Balance: The larger your balance, the higher your minimum payment will generally be (using the percentage method).

- Credit Limit: Credit limits can indirectly influence minimum payments as they affect the outstanding balance. Higher credit limits allow for larger balances, potentially leading to higher minimum payments.

- Promotional Periods (e.g., 0% APR): During promotional periods with 0% interest, the minimum payment might still be based on the outstanding balance, but the interest component is zero. However, once the promotional period ends, the minimum payment recalculation will include interest.

- Late Payments: Consistent late payments can lead to higher minimum payments or even a higher interest rate.

- Card Type: The type of credit card (e.g., secured, unsecured, rewards card) may indirectly influence the minimum payment through its impact on the interest rate and balance.

4. Hidden Costs of Minimum Payments:

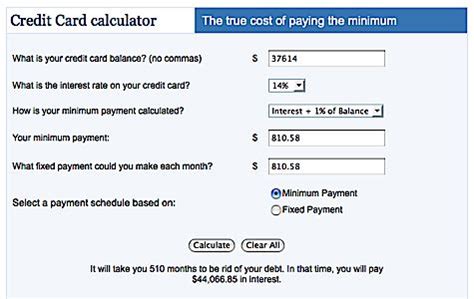

The biggest hidden cost of paying only the minimum payment is the accumulated interest. When you only pay the minimum, a significant portion of your payment goes towards interest, leaving only a small amount to reduce the principal balance. This can trap you in a cycle of debt for years, resulting in far more total interest paid than if you paid more each month. This is compounded by the fact that interest is usually calculated on the daily balance, meaning you pay interest on interest.

5. Strategies for Effective Debt Repayment:

Paying only the minimum payment is rarely the most financially sound approach. Consider these alternatives:

- Debt Avalanche Method: Prioritize paying off the debt with the highest interest rate first.

- Debt Snowball Method: Prioritize paying off the debt with the smallest balance first, regardless of the interest rate. This method can provide psychological motivation.

- Balance Transfer: Transfer your balance to a card with a lower interest rate (be mindful of balance transfer fees).

- Debt Consolidation Loan: Consolidate your debts into a single loan with a lower interest rate.

6. Impact on Credit Score:

While paying the minimum payment avoids late fees, consistently paying only the minimum negatively impacts your credit utilization ratio – the percentage of your available credit you're using. A high credit utilization ratio (typically above 30%) can significantly lower your credit score.

7. Practical Tips for Responsible Credit Card Use:

- Budgeting: Create a budget that allows you to pay more than the minimum payment each month.

- Track Spending: Monitor your spending habits closely to avoid accumulating excessive debt.

- Pay in Full Whenever Possible: Aim to pay your balance in full each month to avoid interest charges entirely.

- Read Your Credit Card Agreement: Understand the terms and conditions, including the minimum payment calculation method.

- Contact Your Issuer: If you're struggling to make payments, contact your credit card company to discuss options like payment plans or hardship programs.

Exploring the Connection Between Interest Rates and Minimum Payment Calculation:

The interest rate on your credit card significantly impacts the minimum payment calculation, even if it isn't explicitly part of the formula. A higher interest rate means more of your minimum payment goes towards interest, leaving less to reduce your principal balance. This makes it even more crucial to pay more than the minimum if you have a high interest rate, as it minimizes the overall interest paid.

Key Factors to Consider:

-

Roles and Real-World Examples: A higher interest rate of 20% will mean significantly more of your minimum payment goes to interest compared to a rate of 10%. Consider a $1000 balance with a 2% minimum payment. At 20% interest, the interest component might be $16.67 per month, leaving only $3.33 to reduce the principal. At 10%, the interest would be approximately half that, leaving more for principal reduction.

-

Risks and Mitigations: High interest rates increase the risk of long-term debt and increased overall cost. Mitigation strategies include paying more than the minimum, seeking a lower interest rate card, or paying off debt faster.

-

Impact and Implications: High interest rates exacerbate the negative consequences of paying only the minimum payment, significantly prolonging debt repayment and increasing the total cost.

Conclusion: Reinforcing the Connection:

The connection between interest rates and minimum payment calculations is undeniably significant. A higher interest rate directly impacts the effectiveness of minimum payments in reducing debt. Understanding this relationship is crucial for responsible credit card management.

Further Analysis: Examining Interest Rates in Greater Detail:

Interest rates are determined by various factors, including the creditworthiness of the cardholder, the type of credit card, and the prevailing market conditions. Understanding these factors allows you to negotiate better rates or choose cards with more favorable terms.

FAQ Section: Answering Common Questions About Minimum Payment Calculation:

Q: What happens if I don't pay my minimum payment?

A: Failure to pay your minimum payment results in late fees, damage to your credit score, and potentially increased interest rates.

Q: Can my minimum payment change each month?

A: Yes, it can change depending on your outstanding balance and the calculation method used by your issuer.

Q: Is it always better to pay more than the minimum payment?

A: Yes, consistently paying more than the minimum payment significantly reduces the overall cost of borrowing and accelerates debt repayment.

Q: Where can I find my minimum payment amount?

A: Your minimum payment amount is clearly stated on your monthly credit card statement.

Practical Tips: Maximizing the Benefits of Understanding Minimum Payment Calculations:

- Understand the Basics: Learn how your credit card company calculates your minimum payment.

- Set Realistic Goals: Create a realistic budget that allows you to pay more than the minimum payment.

- Track Your Progress: Monitor your debt reduction progress and adjust your payment strategy as needed.

- Seek Professional Help: If you're struggling with debt, seek guidance from a financial advisor or credit counselor.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding how credit card companies calculate your minimum payment is not merely academic; it’s essential for financial health. By recognizing the pitfalls of relying solely on minimum payments and proactively managing your debt, you can avoid the debt trap and build a strong financial future. Take control of your finances, and remember that informed decisions lead to lasting financial success.

Latest Posts

Latest Posts

-

What Is The Minimum Payment On A 1000 Credit Card Chase

Apr 05, 2025

-

What Is The Minimum Payment On A 300 Credit Card Chase

Apr 05, 2025

-

What Is The Minimum Payment On A 1500 Credit Card Chase

Apr 05, 2025

-

What Is The Minimum Payment On A 3000 Credit Card Chase

Apr 05, 2025

-

What Is The Minimum Payment On Chase Credit Card

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about How Do Credit Card Companies Calculate Your Minimum Payment . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.