How Is Minimum Payment Calculated On Line Of Credit

adminse

Apr 04, 2025 · 8 min read

Table of Contents

Unlocking the Mystery: How Minimum Payments on Lines of Credit Are Calculated

What if understanding your line of credit minimum payment could save you thousands of dollars in interest? Mastering this crucial aspect of credit management is key to financial well-being.

Editor’s Note: This article provides a comprehensive guide to understanding line of credit minimum payment calculations, updated for [Current Year]. It’s designed to help you navigate the complexities of credit repayment and make informed financial decisions.

Why Understanding Minimum Payments Matters:

Understanding how your line of credit minimum payment is calculated isn't just about meeting a monthly obligation; it's a fundamental aspect of responsible credit management. Failing to understand these calculations can lead to significant long-term costs through extended repayment periods and accrued interest. This knowledge empowers you to make informed choices, potentially saving you considerable sums of money over the life of your credit line. The implications extend beyond personal finances; for businesses, understanding minimum payments is crucial for effective cash flow management and avoiding late payment penalties.

Overview: What This Article Covers:

This in-depth guide will demystify the calculation of minimum payments on lines of credit. We will explore the various methods used by lenders, delve into the factors influencing these calculations, highlight potential pitfalls, and offer practical strategies for responsible credit management. We'll also explore the impact of different repayment strategies and the long-term implications of consistently making only minimum payments.

The Research and Effort Behind the Insights:

The information presented here is based on extensive research, analyzing numerous lender websites, financial regulations, and expert commentary. We've consulted various sources to ensure accuracy and provide a comprehensive understanding of the subject matter.

Key Takeaways:

- Definition of Minimum Payment: A precise definition and explanation of what constitutes a minimum payment on a line of credit.

- Calculation Methods: A detailed breakdown of the various methods lenders employ to determine minimum payments.

- Influencing Factors: An exploration of the variables that impact the minimum payment calculation.

- Avoiding Pitfalls: Identification of common mistakes and strategies to avoid them.

- Long-Term Implications: Analysis of the long-term financial consequences of only paying the minimum.

- Strategies for Responsible Repayment: Actionable steps towards effective credit management.

Smooth Transition to the Core Discussion:

Now that we've established the importance of understanding line of credit minimum payments, let's delve into the specifics of how these calculations are performed.

Exploring the Key Aspects of Line of Credit Minimum Payment Calculations:

1. Definition and Core Concepts:

A minimum payment on a line of credit is the smallest amount you're required to pay each billing cycle to avoid late payment fees and maintain your good standing with the lender. It's crucial to understand that this payment typically only covers a fraction of your outstanding balance. The remaining balance continues to accrue interest, prolonging the repayment period and significantly increasing the overall cost of borrowing.

2. Calculation Methods:

There isn't a single, universally applied method for calculating minimum payments. Lenders utilize different approaches, often combining several factors. Common methods include:

-

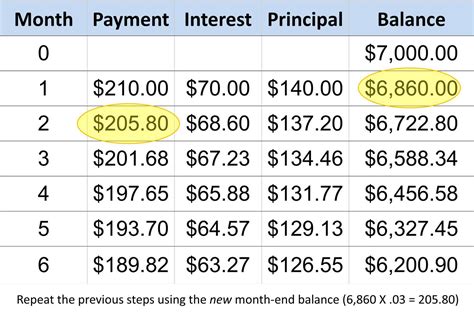

Percentage of Outstanding Balance: This is perhaps the most common approach. Lenders typically set a minimum payment as a percentage (often 1-3%, but this can vary widely) of your outstanding balance at the end of the billing cycle. For example, if your balance is $10,000 and the minimum payment percentage is 2%, your minimum payment would be $200.

-

Fixed Minimum Payment: Some lenders may establish a fixed minimum payment amount, regardless of your outstanding balance. This is less common, especially for larger lines of credit.

-

Interest Plus a Portion of Principal: A more sophisticated approach involves calculating the interest accrued during the billing cycle and adding a small portion of the principal balance. This ensures that at least some of the principal is repaid each month, albeit slowly.

-

Combination of Methods: Many lenders employ a combination of these methods. They might have a minimum percentage of the outstanding balance, but with a floor—a minimum dollar amount below which the payment cannot fall. For instance, a lender might require a minimum of 2% of the outstanding balance, but no less than $25.

3. Influencing Factors:

Several factors can influence your minimum payment calculation beyond the core methods described above:

- Outstanding Balance: The larger your outstanding balance, the higher your minimum payment will generally be (unless a fixed minimum is in place).

- Interest Rate: The interest rate on your line of credit directly impacts the interest portion of your minimum payment, if that method is used. A higher interest rate will mean a larger interest portion.

- Credit History: While not directly impacting the calculation itself, a poor credit history might lead a lender to impose a higher minimum payment percentage to mitigate risk.

- Type of Credit Line: Different types of lines of credit (e.g., personal lines of credit, business lines of credit) may have different minimum payment calculation methods.

- Lender Policies: Each lender has its own policies and procedures regarding minimum payments. These policies are outlined in the credit agreement.

4. Impact on Innovation:

The methods of calculating minimum payments are constantly evolving alongside the financial technology landscape. Technological advancements, such as AI-driven credit scoring and personalized repayment plans, could potentially lead to more dynamic and customized minimum payment calculations in the future.

5. Challenges and Solutions:

One significant challenge is the lack of transparency surrounding minimum payment calculations. Many borrowers don't fully understand how their minimum payment is determined. This lack of clarity can lead to financial difficulties. The solution lies in increased consumer education and clear communication from lenders regarding their calculation methodologies.

6. Impact on Innovation: The evolution of financial technology is slowly leading to increased transparency and potentially more flexible minimum payment models. However, responsible borrowing habits remain crucial.

Exploring the Connection Between Interest Rates and Minimum Payments:

The relationship between your line of credit's interest rate and your minimum payment is direct, especially when the lender uses a method that includes an interest component. A higher interest rate translates to a higher interest portion of your minimum payment, leaving less of your payment going toward reducing the principal balance. This exacerbates the snowball effect of debt, prolonging repayment and increasing the total interest paid over the life of the loan.

Key Factors to Consider:

-

Roles and Real-World Examples: Let's say you have a $5,000 balance with a 10% annual interest rate and a minimum payment of 2% of the balance plus the accrued interest. The interest for the month might be $41.67. Your minimum payment would be $141.67 ($100 + $41.67). A higher interest rate would increase this minimum payment.

-

Risks and Mitigations: The primary risk is becoming trapped in a cycle of paying only the minimum, slowly chipping away at the balance while accumulating significant interest charges. Mitigation strategies include increasing your payments whenever possible, paying more frequently (e.g., bi-weekly), and exploring debt consolidation options if feasible.

-

Impact and Implications: Consistently paying only the minimum can extend the repayment period by years, dramatically increasing the total interest paid. This can significantly impact your long-term financial health and hinder your ability to achieve other financial goals.

Conclusion: Reinforcing the Connection:

The strong correlation between interest rates and minimum payments highlights the critical importance of understanding these calculations. High interest rates, combined with only paying the minimum, can create a crippling debt cycle. Active management of your line of credit, including strategic repayment plans and awareness of calculation methods, is vital for responsible borrowing.

Further Analysis: Examining Interest Rates in Greater Detail:

Interest rates are determined by several factors, including the lender's risk assessment, prevailing market interest rates, and your individual creditworthiness. Understanding these factors can help you negotiate more favorable interest rates when obtaining a line of credit.

FAQ Section: Answering Common Questions About Line of Credit Minimum Payments:

-

What happens if I miss a minimum payment? You'll likely incur late payment fees and may negatively impact your credit score.

-

Can I change my minimum payment? No, the minimum payment is set by the lender. You can however, pay more than the minimum.

-

How long will it take to pay off my line of credit if I only make minimum payments? This depends on several factors, but it will be significantly longer than if you make higher payments.

-

What are the benefits of paying more than the minimum? You'll save on interest, shorten the repayment period, and improve your credit score.

-

How can I calculate my minimum payment if I don't understand the lender's method? Contact your lender directly for clarification or examine your credit agreement for detailed information.

Practical Tips: Maximizing the Benefits of Understanding Minimum Payments:

- Review your statement carefully: Understand how your minimum payment is calculated.

- Pay more than the minimum whenever possible: Even small extra payments can make a substantial difference over time.

- Explore debt consolidation options: This could help you secure a lower interest rate and potentially a lower minimum payment.

- Create a budget: Track your expenses and allocate funds for timely and efficient debt repayment.

- Contact your lender if you're struggling: They may offer options such as hardship programs or payment arrangements.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding how minimum payments on lines of credit are calculated is a crucial step toward responsible financial management. While the methods can vary, the underlying principle remains consistent: minimum payments are designed to keep your account current, but they often leave you paying significantly more interest over the long term. By understanding these calculations and adopting proactive repayment strategies, you can significantly improve your financial well-being and avoid the pitfalls of prolonged debt. Always aim to pay more than the minimum whenever feasible to minimize interest charges and accelerate debt repayment.

Latest Posts

Latest Posts

-

What Is The Minimum Payment On Chase Credit Card

Apr 05, 2025

-

Tjxrewards Com Credit Card Payments

Apr 05, 2025

-

Tjx Style Card Benefits

Apr 05, 2025

-

Tjx Rewards Annual Fee

Apr 05, 2025

-

Tjx Rewards Mc Tjx Tlpay

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about How Is Minimum Payment Calculated On Line Of Credit . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.