Calculate 18 Per Annum Interest

adminse

Apr 03, 2025 · 6 min read

Table of Contents

Calculating 18% Per Annum Interest: A Comprehensive Guide

What if understanding the intricacies of calculating 18% per annum interest unlocks significant financial opportunities? Mastering this fundamental concept empowers individuals and businesses to make informed financial decisions and optimize their returns.

Editor’s Note: This article on calculating 18% per annum interest provides a detailed, practical guide for understanding and applying this crucial financial concept. It's designed to be accessible to a broad audience, from students learning about finance to seasoned professionals seeking a refresher. Updated [Date of Publication].

Why Calculating 18% Per Annum Interest Matters:

Interest calculations are fundamental to numerous financial transactions. Understanding how to calculate 18% per annum interest, a relatively high rate often associated with high-risk investments or loans, is particularly crucial. This knowledge is essential for:

- Investing: Determining potential returns on investments like high-yield bonds or certain types of real estate.

- Borrowing: Understanding the true cost of loans, including credit cards, personal loans, and business financing.

- Budgeting: Accurately forecasting future financial obligations and planning accordingly.

- Financial Planning: Making informed decisions about savings, investments, and debt management.

Overview: What This Article Covers:

This article comprehensively explores calculating 18% per annum interest, covering various methods, scenarios, and factors influencing the calculation. We will examine simple interest, compound interest, and the impact of compounding frequency. Real-world examples and practical applications will be provided to solidify understanding.

The Research and Effort Behind the Insights:

This guide draws upon established financial principles and formulas. The examples and explanations are designed for clarity and accuracy, ensuring readers gain a practical understanding of calculating 18% per annum interest in different contexts.

Key Takeaways:

- Definition of Simple and Compound Interest: A clear explanation of the core concepts.

- Formulas and Calculations: Step-by-step guides to calculate interest under different scenarios.

- Impact of Compounding Frequency: How the frequency of compounding affects the final amount.

- Real-World Applications: Examples illustrating the use of 18% interest calculations in various situations.

- Practical Tips: Guidance on applying these calculations in personal finance and business decisions.

Smooth Transition to the Core Discussion:

Now that we've established the importance of understanding 18% per annum interest calculations, let's delve into the specifics. We'll begin with the fundamental concepts of simple and compound interest.

Exploring the Key Aspects of Calculating 18% Per Annum Interest:

1. Simple Interest:

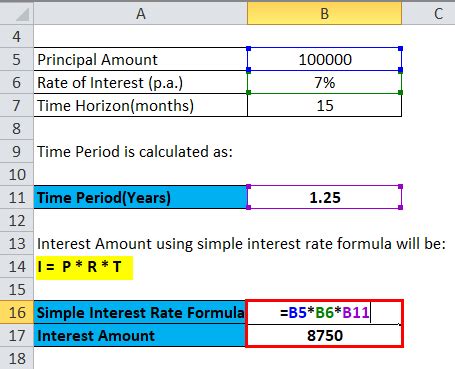

Simple interest is calculated only on the principal amount. It doesn't take into account any accumulated interest from previous periods. The formula for simple interest is:

Simple Interest = (Principal × Rate × Time) / 100

Where:

- Principal: The initial amount of money borrowed or invested.

- Rate: The annual interest rate (in this case, 18%).

- Time: The duration of the loan or investment in years.

Example: If you invest $1,000 at a simple interest rate of 18% for 3 years, the simple interest earned would be:

Simple Interest = ($1,000 × 18 × 3) / 100 = $540

The total amount after 3 years would be $1,000 + $540 = $1,540.

2. Compound Interest:

Compound interest is calculated on the principal amount plus any accumulated interest from previous periods. This means that interest earns interest, leading to faster growth. The formula for compound interest is:

A = P (1 + r/n)^(nt)

Where:

- A: The future value of the investment/loan, including interest.

- P: The principal amount.

- r: The annual interest rate (as a decimal, so 18% becomes 0.18).

- n: The number of times that interest is compounded per year (e.g., annually = 1, semi-annually = 2, quarterly = 4, monthly = 12).

- t: The time the money is invested or borrowed for, in years.

Example: Let's use the same $1,000 principal invested for 3 years at 18% interest, but this time compounded annually:

A = $1,000 (1 + 0.18/1)^(1×3) = $1,000 (1.18)^3 ≈ $1,540.7

Notice that the total amount with compound interest ($1,560.897) is slightly higher than with simple interest ($1,540). This difference becomes more significant over longer periods and with higher interest rates.

3. Impact of Compounding Frequency:

The frequency of compounding significantly impacts the final amount. More frequent compounding (e.g., monthly instead of annually) leads to higher returns because interest is calculated and added to the principal more often.

Example: Let's see the difference if the $1,000 is compounded monthly instead of annually:

A = $1,000 (1 + 0.18/12)^(12×3) ≈ $1,677.69

As you can see, monthly compounding results in a considerably higher final amount ($1,677.69) compared to annual compounding ($1,600.897).

Exploring the Connection Between Loan Term and 18% Per Annum Interest:

The length of the loan term (Time, 't' in the formulas) plays a crucial role in the total interest paid. Longer loan terms lead to higher total interest payments, even if the interest rate remains the same.

Key Factors to Consider:

- Roles and Real-World Examples: A longer loan term at 18% interest is common in high-risk, short-term loans or some types of business financing. The high interest compensates the lender for the increased risk.

- Risks and Mitigations: Borrowing at 18% interest carries substantial risk. Borrowers should carefully assess their ability to repay the loan and explore alternative financing options with lower interest rates if possible.

- Impact and Implications: High interest payments can severely impact personal or business finances. Careful budgeting and financial planning are critical when dealing with loans at this interest rate.

Further Analysis: Examining Loan Amortization in Greater Detail:

Loan amortization refers to the process of paying off a loan through regular payments. Each payment typically covers both interest and principal. For an 18% per annum loan, a substantial portion of the initial payments will go towards interest, with the principal repayment increasing over time.

FAQ Section: Answering Common Questions About Calculating 18% Per Annum Interest:

Q: What is the difference between simple and compound interest?

A: Simple interest is calculated only on the principal amount, while compound interest is calculated on the principal plus accumulated interest. Compound interest leads to faster growth.

Q: How does compounding frequency affect the total interest paid?

A: More frequent compounding leads to higher total interest earned (or paid) because interest is calculated and added to the principal more often.

Q: Are there any online calculators to help with these calculations?

A: Yes, numerous online calculators are available to simplify these calculations. Searching for "compound interest calculator" will provide many options.

Practical Tips: Maximizing the Benefits (or Minimizing the Costs) of 18% Per Annum Interest:

-

Understand the Basics: Before entering into any financial agreement involving 18% interest, ensure a complete understanding of simple vs. compound interest and the impact of compounding frequency.

-

Compare Options: If borrowing at 18%, explore all available options and compare interest rates, terms, and fees from different lenders.

-

Careful Budgeting: If you have a loan at this rate, develop a strict budget to ensure timely repayments and avoid late fees or default.

Final Conclusion: Wrapping Up with Lasting Insights:

Calculating 18% per annum interest is a crucial skill for anyone involved in finance. Whether investing or borrowing, understanding the nuances of simple and compound interest, the impact of compounding frequency, and the implications of loan terms is essential for informed decision-making. By mastering these concepts, individuals and businesses can optimize their financial outcomes and navigate the complexities of high-interest financial instruments effectively. Remember, responsible financial planning is key, especially when dealing with higher interest rates.

Latest Posts

Latest Posts

-

How To Set Up Automatic Late Fees In Quickbooks Desktop

Apr 04, 2025

-

How To Charge Late Fees In Quickbooks

Apr 04, 2025

-

How To Apply Late Fees In Quickbooks

Apr 04, 2025

-

How To Set Up Automatic Late Fees In Quickbooks Online

Apr 04, 2025

-

How Do I Set Up Automatic Late Fees In Quickbooks Desktop

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about Calculate 18 Per Annum Interest . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.