What Is The Minimum Payment On A Balance Transfer Credit Card

adminse

Apr 04, 2025 · 8 min read

Table of Contents

What are the minimum payment requirements on a balance transfer credit card?

Understanding minimum payments on balance transfer credit cards is crucial for responsible debt management.

Editor’s Note: This article on minimum payments for balance transfer credit cards was published today, offering current and accurate information on this critical aspect of personal finance. This guide aims to clarify the complexities surrounding minimum payments, helping readers make informed decisions and avoid potential pitfalls.

Why Minimum Payments Matter:

Ignoring the intricacies of minimum payments on balance transfer credit cards can lead to significant financial repercussions. Understanding these payments is crucial for several reasons:

-

Avoiding Late Fees: Failing to make even the minimum payment by the due date results in late fees, significantly increasing the overall cost of your debt. These fees can add up rapidly, hindering your progress toward paying off the balance.

-

High Interest Accumulation: While a balance transfer card offers a temporary 0% APR period, this grace period eventually expires. If the balance isn't paid down substantially before the promotional period ends, the interest charges can become overwhelming. Minimum payments primarily cover interest, leaving the principal balance largely untouched.

-

Negative Impact on Credit Score: Consistent late payments, even if only minimum amounts, severely damage your credit score. A poor credit score makes it harder to secure loans, rent an apartment, or even get a job in some cases. It can also lead to higher interest rates on future borrowing.

-

Lengthened Repayment Period: Sticking to minimum payments significantly extends the time it takes to pay off your debt. This prolonged repayment period means you'll pay substantially more in interest over the life of the loan.

-

Potential for Debt Trap: Relying solely on minimum payments can trap you in a cycle of debt, making it increasingly difficult to escape the burden.

Overview: What This Article Covers:

This article provides a comprehensive guide to understanding minimum payments on balance transfer credit cards. It explores how minimum payments are calculated, the factors influencing their amount, the potential consequences of only making minimum payments, and strategies for managing debt effectively. We'll also address common questions and offer practical advice for navigating this crucial aspect of personal finance.

The Research and Effort Behind the Insights:

This article is the result of extensive research, drawing upon information from reputable financial institutions, consumer protection agencies, and authoritative personal finance resources. The information presented is intended to be accurate and up-to-date, but readers are encouraged to consult with their individual credit card issuers for specific details regarding their accounts.

Key Takeaways:

-

Minimum Payment Calculation: The minimum payment is typically a percentage of your outstanding balance, often between 1% and 3%, but can also include a fixed minimum amount.

-

Factors Affecting Minimum Payments: Several factors can influence the minimum payment amount, including your outstanding balance, the terms of your credit card agreement, and your credit history.

-

Consequences of Minimum Payments: Only making minimum payments can lead to prolonged repayment periods, higher interest costs, damaged credit scores, and the potential for a debt trap.

-

Strategies for Effective Debt Management: Explore different repayment strategies, such as the debt avalanche or debt snowball methods, to accelerate debt repayment and minimize interest charges.

Smooth Transition to the Core Discussion:

Now that we've established the importance of understanding minimum payments, let's delve into the specifics of how these payments are calculated and the factors influencing their amount.

Exploring the Key Aspects of Minimum Payments on Balance Transfer Credit Cards:

1. Definition and Core Concepts:

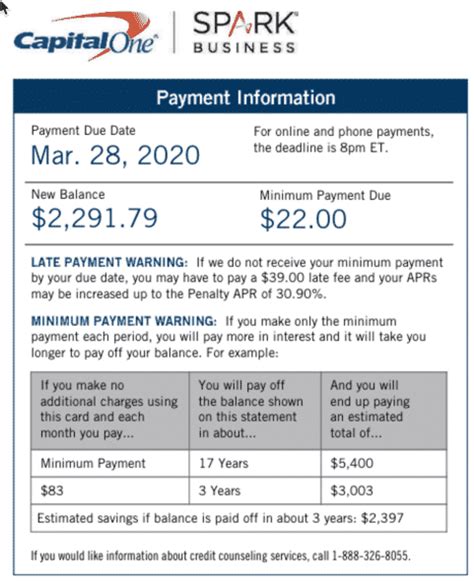

The minimum payment on a balance transfer credit card is the smallest amount you're required to pay each month to avoid late fees and maintain your account in good standing. It's usually calculated as a percentage of your outstanding balance, with a minimum dollar amount often added. For example, a card might require a minimum payment of 2% of the balance, but not less than $25.

2. How Minimum Payments are Calculated:

The calculation method can vary slightly from one credit card issuer to another. However, the general process involves determining a percentage of the outstanding balance and then adding a fixed minimum amount if the percentage-based calculation falls below that threshold. The credit card agreement outlines the specific formula used for calculating minimum payments.

3. Factors Influencing Minimum Payments:

Several factors influence the minimum payment amount, including:

-

Outstanding Balance: The larger your balance, the higher your minimum payment will generally be (because of the percentage component).

-

Credit Card Agreement: Your credit card agreement clearly states the terms and conditions regarding minimum payments. This agreement should be carefully reviewed to understand the specific calculation method employed by your issuer.

-

Credit History: While not directly impacting the calculation formula, a poor credit history may lead to stricter payment terms, potentially resulting in higher minimum payments or additional fees.

4. Applications Across Industries:

Balance transfer credit cards are a product offered by various financial institutions, and the calculation of minimum payments generally follows a consistent pattern across the industry. However, specific terms and conditions might differ depending on the issuer.

5. Challenges and Solutions:

One major challenge with minimum payments is their tendency to significantly extend the repayment period. This can lead to substantial interest charges over time. The solution is to pay more than the minimum payment whenever possible to accelerate debt reduction.

6. Impact on Innovation:

There haven't been significant innovations in the fundamental calculation of minimum payments. However, there have been advancements in technology that allow for easier online access to statements and payment options.

Closing Insights: Summarizing the Core Discussion:

Understanding minimum payments on balance transfer credit cards is fundamental to responsible debt management. Failure to meet even the minimum payment can result in severe financial consequences, including late fees, damaged credit scores, and an extended repayment period.

Exploring the Connection Between APR and Minimum Payments:

The Annual Percentage Rate (APR) is directly related to the minimum payment. The minimum payment often only covers the interest accrued on the balance, leaving the principal largely untouched. The lower the APR, the less interest is charged, but a lower APR does not reduce the principal amount unless a larger payment than the minimum is made.

Key Factors to Consider:

-

Roles and Real-World Examples: A higher APR means a larger portion of the minimum payment will go towards interest, making it harder to reduce the principal balance. For example, a $1,000 balance with a 15% APR will have a substantially larger interest component in the minimum payment compared to the same balance with a 5% APR.

-

Risks and Mitigations: The primary risk is becoming trapped in a cycle of debt where minimum payments barely cover interest, preventing meaningful progress towards debt elimination. Mitigation involves paying more than the minimum, actively working to reduce the principal balance.

-

Impact and Implications: Failure to address the impact of APR on minimum payments leads to longer repayment periods and significantly increased overall borrowing costs.

Conclusion: Reinforcing the Connection:

The relationship between APR and minimum payments highlights the importance of proactively managing debt. Paying more than the minimum payment helps reduce principal, reducing the overall cost of borrowing and accelerating debt payoff.

Further Analysis: Examining APR in Greater Detail:

A deeper dive into APR reveals its critical influence on debt management. Understanding the APR and its impact on the minimum payment amount allows for better financial planning and informed decision-making regarding debt repayment strategies.

FAQ Section: Answering Common Questions About Minimum Payments on Balance Transfer Credit Cards:

Q: What is the typical range for minimum payments on balance transfer cards?

A: Minimum payments typically range from 1% to 3% of the outstanding balance, often with a minimum dollar amount (e.g., $25).

Q: What happens if I only make the minimum payment?

A: Making only the minimum payment prolongs the repayment period and increases the total interest paid over time.

Q: Can my minimum payment change over time?

A: Yes, the minimum payment can change based on your outstanding balance.

Q: What are the consequences of missing a minimum payment?

A: Missing a minimum payment can result in late fees, damaged credit score, and increased interest charges.

Practical Tips: Maximizing the Benefits of Balance Transfer Cards:

-

Understand the Terms: Carefully review the terms and conditions of your balance transfer credit card agreement.

-

Budget Effectively: Create a budget to allocate funds for making more than the minimum payment each month.

-

Explore Debt Repayment Strategies: Consider the debt avalanche or snowball methods to prioritize repayment.

-

Monitor Your Account Regularly: Track your spending, payments, and interest charges to ensure you're making progress.

-

Consider Professional Help: If you're struggling to manage your debt, consult with a financial advisor or credit counselor.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding the minimum payment on a balance transfer credit card is essential for responsible financial management. While the convenience of a balance transfer can be beneficial, a proactive approach to repayment, involving more than minimum payments, is necessary to avoid incurring excessive interest and jeopardizing credit scores. By understanding the factors influencing minimum payments and employing effective debt repayment strategies, individuals can harness the benefits of balance transfers while minimizing potential risks.

Latest Posts

Latest Posts

-

Payment Thresholds

Apr 05, 2025

-

Apa Itu Minimum Charge

Apr 05, 2025

-

Minimum Payment Threshold

Apr 05, 2025

-

How Much Dose Jcpenny Pay

Apr 05, 2025

-

How Much Jcpenney Pay An Hour

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about What Is The Minimum Payment On A Balance Transfer Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.