What Is The Minimum Payment On A $20000 Credit Card Balance

adminse

Apr 04, 2025 · 7 min read

Table of Contents

Decoding Minimum Payments: Understanding the Realities of a $20,000 Credit Card Balance

What if paying the minimum on a $20,000 credit card balance could trap you in a cycle of debt for years, even decades? Understanding minimum payments and their long-term implications is crucial for responsible credit management.

Editor’s Note: This article on minimum credit card payments for a $20,000 balance was published today, providing readers with up-to-date information and strategies for managing high-balance credit card debt.

Why Minimum Payments Matter: A $20,000 Reality Check

A $20,000 credit card balance represents a significant financial burden. Ignoring the magnitude of this debt can lead to severe consequences, impacting credit scores, financial stability, and overall well-being. Understanding the mechanics of minimum payments—their calculation, their impact on repayment timelines, and the associated interest costs—is crucial for developing a responsible repayment strategy. This knowledge empowers individuals to make informed decisions about their debt and potentially avoid long-term financial distress.

Overview: What This Article Covers

This comprehensive guide will explore the complexities of minimum payments on a $20,000 credit card balance. We will dissect how minimum payments are calculated, analyze their long-term financial repercussions, explore alternative repayment strategies, and provide actionable steps for debt management. Readers will gain a clear understanding of the financial pitfalls associated with solely relying on minimum payments and discover effective strategies for tackling significant credit card debt.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon information from reputable financial institutions, credit bureaus, consumer finance experts, and relevant government publications. The analysis incorporates real-world examples and data to illustrate the points discussed, ensuring readers receive accurate and reliable information to help navigate their financial situations.

Key Takeaways:

- Minimum Payment Calculation: Understanding the factors that influence the calculation of your minimum payment.

- Interest Accrual: The significant role of compound interest in prolonging repayment and increasing the total cost of debt.

- Repayment Timelines: Analyzing the extended repayment periods associated with minimum payments.

- Alternative Strategies: Exploring debt consolidation, balance transfers, and debt management plans.

- Practical Steps: Actionable steps to take control of your credit card debt.

Smooth Transition to the Core Discussion

Now that we've established the importance of understanding minimum payments, let's delve into the specifics of how they are determined and their profound impact on a $20,000 credit card balance.

Exploring the Key Aspects of Minimum Payments on a $20,000 Balance

1. Definition and Core Concepts:

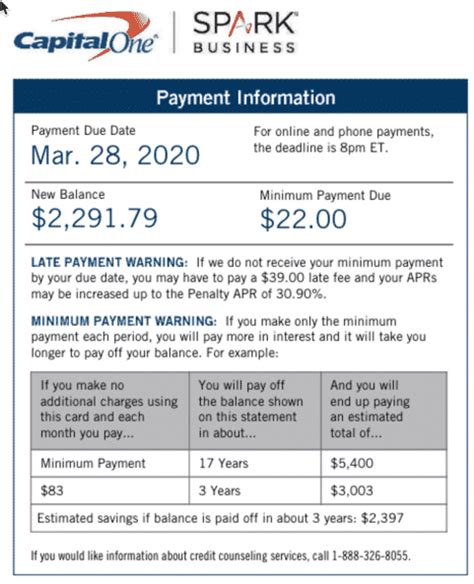

The minimum payment on a credit card is the smallest amount a cardholder is required to pay each billing cycle to remain in good standing with the creditor. This payment typically consists of a percentage of the outstanding balance (often 1-3%) plus any accrued interest and fees. For a $20,000 balance, a 2% minimum payment would equate to $400. However, this amount can fluctuate based on the card's terms and conditions.

2. Applications Across Industries:

While the calculation method may vary slightly between credit card issuers, the core principle remains consistent: minimum payments are designed to keep accounts active and generate interest income for the lender. It is crucial to understand that this system is designed to benefit the creditor, and relying solely on minimum payments almost always results in significantly increased long-term costs.

3. Challenges and Solutions:

The primary challenge with minimum payments on a large balance like $20,000 is the slow repayment and the significant accumulation of interest. This can trap individuals in a cycle of debt, potentially for many years. Solutions involve creating a budget, exploring debt consolidation options, or negotiating with creditors for lower interest rates or payment plans.

4. Impact on Innovation:

The rise of fintech companies and online debt management tools showcases innovation in addressing the challenges of credit card debt. These tools provide resources for budgeting, debt tracking, and exploring alternative repayment strategies.

Closing Insights: Summarizing the Core Discussion

Minimum payments, while seemingly convenient, often lead to a prolonged and costly repayment journey. For a $20,000 balance, relying solely on minimum payments can result in significantly increased interest charges and a much longer repayment timeline. Understanding this reality is critical for effective debt management.

Exploring the Connection Between Interest Rates and Minimum Payments

The relationship between interest rates and minimum payments is crucial. Higher interest rates dramatically amplify the amount of interest accrued over time. On a $20,000 balance, even a small percentage increase in the annual percentage rate (APR) can substantially increase the total cost of repayment and prolong the debt repayment period.

Key Factors to Consider:

-

Roles and Real-World Examples: A credit card with a 20% APR on a $20,000 balance will accrue considerably more interest than one with a 10% APR, even if the minimum payment remains the same. This highlights the importance of considering interest rates when choosing and managing credit cards.

-

Risks and Mitigations: High interest rates coupled with minimum payments pose a significant risk of debt spiraling out of control. Mitigation strategies include negotiating lower interest rates, transferring balances to a card with a lower APR, or consolidating debt.

-

Impact and Implications: Ignoring the impact of high interest rates can lead to financial hardship, damage credit scores, and hinder long-term financial goals.

Conclusion: Reinforcing the Connection

The connection between interest rates and minimum payments underlines the importance of proactive debt management. By carefully considering interest rates and exploring alternative strategies, individuals can effectively manage their credit card debt and avoid the pitfalls of long-term, high-interest repayment.

Further Analysis: Examining Compound Interest in Greater Detail

Compound interest is the silent killer of credit card debt. It works by adding interest not only to the principal balance but also to the accumulated interest from previous periods. On a $20,000 balance, this compounding effect can drastically inflate the total amount owed over time, even if consistent minimum payments are made. Understanding this concept is paramount for developing a strategic repayment plan.

FAQ Section: Answering Common Questions About Minimum Payments

Q: What is the average minimum payment percentage on a credit card?

A: While it varies between lenders and individual card agreements, the average minimum payment is often between 1% and 3% of the outstanding balance. However, it's crucial to check your individual credit card statement for the exact percentage.

Q: How long will it take to pay off a $20,000 credit card balance using only minimum payments?

A: This depends heavily on the APR and the minimum payment percentage. It could take many years, even decades, to pay off the balance solely through minimum payments, resulting in a significantly higher total cost due to accrued interest.

Q: What are the consequences of consistently paying only the minimum payment?

A: Consistently paying only the minimum can lead to prolonged debt, increased interest charges, damage to credit scores, and potential financial strain.

Q: Are there any legal protections for cardholders struggling with minimum payments?

A: There are resources available, such as credit counseling agencies and debt management programs, that can assist individuals in developing repayment plans and negotiating with creditors. These resources can help navigate legal options and protect against potential harm.

Practical Tips: Maximizing the Benefits of Strategic Repayment

-

Create a Realistic Budget: Track your income and expenses to identify areas for savings and allocate funds towards debt repayment.

-

Negotiate with Your Credit Card Company: Contact your credit card company to discuss options such as lower interest rates, payment plans, or hardship programs.

-

Explore Debt Consolidation: Consolidate your credit card debt into a lower-interest loan to simplify payments and potentially accelerate repayment.

-

Consider a Balance Transfer: Transfer your balance to a credit card with a lower introductory APR to reduce interest charges during the promotional period. Be aware of balance transfer fees and ensure you can pay off the balance before the promotional period ends.

-

Seek Professional Help: Consult with a certified financial planner or credit counselor for personalized advice and support.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding minimum payments on a $20,000 credit card balance is critical for responsible financial management. While convenient in the short term, solely relying on minimum payments can lead to a long and costly repayment journey. By understanding the factors influencing minimum payment calculations, the impact of compound interest, and alternative repayment strategies, individuals can take control of their debt, improve their financial well-being, and achieve long-term financial stability. Remember, proactive debt management is key to avoiding the traps of high-balance credit card debt.

Latest Posts

Latest Posts

-

What Is The Minimum Amount To Run Google Ads

Apr 05, 2025

-

What Is The Minimum For Google Ads

Apr 05, 2025

-

What Is The Minimum Amount For Google Ads

Apr 05, 2025

-

Minimum Payment On Usaa Credit Card

Apr 05, 2025

-

Minimum Payment Of A Credit Card

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about What Is The Minimum Payment On A $20000 Credit Card Balance . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.