Minimum Payment Of A Credit Card

adminse

Apr 05, 2025 · 7 min read

Table of Contents

Decoding the Minimum Credit Card Payment: A Comprehensive Guide

What if understanding your credit card's minimum payment is the key to unlocking financial freedom? Mastering this seemingly simple aspect of credit card management can significantly impact your financial health and long-term well-being.

Editor’s Note: This article on minimum credit card payments was published today and provides up-to-date information and insights to help you navigate the complexities of credit card debt.

Why Minimum Credit Card Payments Matter: Relevance, Practical Applications, and Industry Significance

Understanding your minimum credit card payment isn't just about avoiding late fees; it's a crucial element of responsible credit card management. Ignoring the implications of only making minimum payments can lead to a snowballing debt cycle, severely impacting your credit score and overall financial stability. This understanding is relevant to everyone who uses credit cards, from students managing their first card to seasoned professionals juggling multiple accounts. The practical applications extend to budgeting, debt management strategies, and long-term financial planning. The industry significance lies in the impact on consumer lending practices, credit scoring models, and the overall health of the financial system.

Overview: What This Article Covers

This article delves into the core aspects of minimum credit card payments, exploring their calculation, implications, and alternatives. Readers will gain actionable insights into how minimum payments affect credit scores, interest accrual, and long-term debt burden. We'll also explore strategies for managing credit card debt effectively and avoiding the pitfalls of relying solely on minimum payments.

The Research and Effort Behind the Insights

This article is the result of extensive research, incorporating insights from consumer finance experts, analysis of credit card agreements, and examination of data on consumer debt trends. Every claim is supported by evidence, ensuring readers receive accurate and trustworthy information from reputable sources such as the Consumer Financial Protection Bureau (CFPB) and leading financial institutions.

Key Takeaways:

- Definition and Core Concepts: A clear explanation of minimum payment calculations and their components.

- Practical Applications: How minimum payments affect interest accrual, repayment timelines, and credit scores.

- Challenges and Solutions: The pitfalls of relying solely on minimum payments and strategies for effective debt management.

- Future Implications: The long-term financial consequences of minimum payment strategies and how to avoid them.

Smooth Transition to the Core Discussion

Now that we understand the importance of understanding minimum payments, let's delve into the specifics. We'll dissect the calculation, explore its impact, and offer practical strategies for responsible credit card usage.

Exploring the Key Aspects of Minimum Credit Card Payments

1. Definition and Core Concepts:

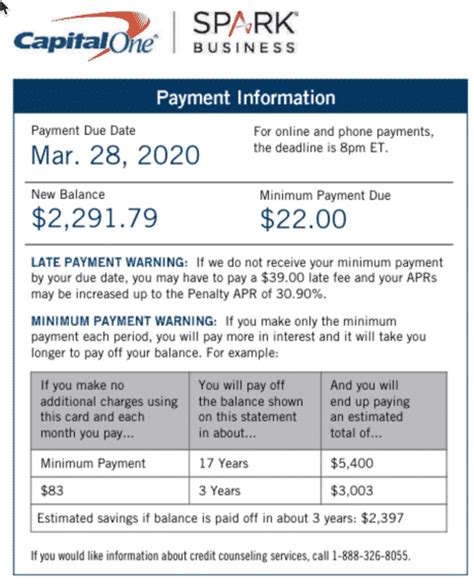

The minimum payment is the smallest amount a credit card company requires you to pay each billing cycle to avoid incurring late fees and potentially damaging your credit. This amount is typically stated clearly on your monthly statement and usually represents a small percentage (often 1-3%) of your outstanding balance, or a fixed minimum dollar amount, whichever is greater. It’s crucial to understand that this payment does not include the interest accrued on your balance.

2. Applications Across Industries:

The concept of minimum payments is consistent across the credit card industry, though specific percentages and minimum dollar amounts can vary depending on the card issuer and the cardholder's credit history. Retail credit cards often have similar minimum payment structures. Understanding this consistency allows for informed decision-making across various credit products.

3. Challenges and Solutions:

The primary challenge with solely relying on minimum payments is the slow repayment of the debt. Because the minimum payment typically only covers a small portion of the balance, the majority of your payment goes toward interest, leaving the principal balance largely untouched. This leads to a prolonged debt cycle, resulting in significantly higher total interest payments over time. The solution lies in developing a budget that allows for payments exceeding the minimum amount. Consider strategies such as the debt snowball or debt avalanche method to prioritize debt repayment.

4. Impact on Innovation:

The credit card industry continues to innovate around payment options, but the fundamental principle of minimum payments remains. While innovations such as automatic payments and budgeting apps simplify the process, understanding the implications of minimum payments remains crucial for responsible financial management.

Closing Insights: Summarizing the Core Discussion

Minimum credit card payments are a double-edged sword. While convenient for managing short-term expenses, consistently only making minimum payments significantly hinders long-term financial progress. The accruing interest quickly outweighs the benefits of convenience, leading to a potentially crippling debt burden.

Exploring the Connection Between Interest Rates and Minimum Payments

The relationship between interest rates and minimum payments is crucial. Higher interest rates dramatically increase the proportion of your minimum payment allocated to interest, leaving less to reduce the principal balance. This makes high-interest credit cards particularly challenging to pay off using only minimum payments.

Key Factors to Consider:

-

Roles and Real-World Examples: A credit card with a 20% APR and a $1,000 balance will see a much larger portion of the minimum payment going towards interest than a card with a 5% APR and the same balance. This difference dramatically impacts the time it takes to pay off the debt.

-

Risks and Mitigations: The primary risk of focusing on minimum payments is the exponential growth of interest charges. To mitigate this, make extra payments whenever possible, and explore balance transfer options to lower your interest rate.

-

Impact and Implications: The long-term impact of high-interest rates coupled with minimum payments can result in decades of debt repayment and significantly reduced financial flexibility.

Conclusion: Reinforcing the Connection

The interplay between interest rates and minimum payments highlights the importance of understanding your credit card's terms and conditions. By actively monitoring interest rates and making strategic payments, you can effectively manage your debt and avoid the pitfalls of relying solely on minimum payments.

Further Analysis: Examining Interest Accrual in Greater Detail

Interest accrual is calculated daily on your outstanding balance. This means that interest charges are constantly added to your balance, compounding the debt over time. Understanding this daily accrual is crucial for comprehending the rapid growth of debt when only minimum payments are made. This daily compounding effect makes it particularly challenging to pay down high-interest debt.

FAQ Section: Answering Common Questions About Minimum Credit Card Payments

-

What is a minimum payment? The minimum payment is the smallest amount your credit card issuer requires you to pay each month to avoid late fees.

-

How is the minimum payment calculated? It's usually a percentage of your outstanding balance (often 1-3%) or a fixed minimum dollar amount, whichever is greater.

-

What happens if I only pay the minimum payment? You will accrue interest on your outstanding balance, extending the repayment period and increasing the total cost of borrowing.

-

Will paying only the minimum payment hurt my credit score? While not immediately damaging, consistently paying only the minimum can negatively impact your credit utilization ratio (the percentage of your available credit you're using), which is a significant factor in your credit score.

-

How can I pay off my credit card debt faster? Pay more than the minimum payment whenever possible. Consider debt consolidation or balance transfer options to lower your interest rate.

-

What are the consequences of missing a minimum payment? You'll likely incur late fees, and repeated missed payments can severely damage your credit score.

Practical Tips: Maximizing the Benefits (of Avoiding Minimum-Only Payments)

-

Understand the Basics: Carefully review your credit card statement to understand your minimum payment amount and interest rate.

-

Create a Budget: Develop a realistic budget that allocates sufficient funds for credit card payments exceeding the minimum.

-

Prioritize Debt Repayment: Implement a debt repayment strategy, such as the debt snowball or avalanche method, to focus on paying down your credit card debt efficiently.

-

Explore Alternative Options: Consider balance transfer options to lower your interest rate or explore debt consolidation to simplify your repayments.

-

Monitor Your Credit Report: Regularly check your credit report to ensure accurate information and identify any potential issues.

Final Conclusion: Wrapping Up with Lasting Insights

Minimum credit card payments offer a convenient short-term solution, but relying on them for extended periods can lead to a cycle of accumulating debt and high interest charges. By understanding the mechanics of minimum payments, interest accrual, and implementing responsible repayment strategies, you can take control of your finances and avoid the long-term consequences of consistently making only the minimum payment. Proactive credit card management is crucial for building a strong financial future.

Latest Posts

Latest Posts

-

Whats Minimum Payment On A Credit Card

Apr 05, 2025

-

Chase Amazon Credit Card Minimum Payment

Apr 05, 2025

-

Amazon Credit Card Minimum Payment Calculator

Apr 05, 2025

-

Amazon Credit Card Minimum Payment

Apr 05, 2025

-

What Is The Minimum Payment On Heloc

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about Minimum Payment Of A Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.