What Is The Late Fee Fairness Amendment Act Of 2016

adminse

Apr 03, 2025 · 9 min read

Table of Contents

Unpacking the Late Fee Fairness Amendment Act of 2016: A Deep Dive into Consumer Protections

What if the seemingly small matter of late fees held the key to significant consumer protection? The Late Fee Fairness Amendment Act of 2016 represents a crucial step in re-evaluating the fairness and transparency of these charges, significantly impacting how businesses interact with their customers.

Editor’s Note: This article provides a comprehensive overview of the Late Fee Fairness Amendment Act of 2016, its impact on consumers, and its implications for businesses. The information presented is for educational purposes and should not be considered legal advice.

Why the Late Fee Fairness Amendment Act Matters: Relevance, Practical Applications, and Industry Significance

The Late Fee Fairness Amendment Act of 2016, while not a sweeping piece of federal legislation impacting all industries uniformly, serves as a critical example of the ongoing debate regarding consumer protection and the ethical application of late fees. Its impact is primarily felt within specific sectors where it has been adopted or where similar state-level legislation exists. The Act highlights the importance of transparency, reasonable charges, and the potential for abusive practices related to late fees. It underscores the need for businesses to carefully consider the ethical and legal implications of their fee structures, and for consumers to understand their rights. This focus on fairness resonates with the growing consumer awareness of predatory lending practices and the increasing scrutiny placed on business practices.

Overview: What This Article Covers

This article will thoroughly examine the Late Fee Fairness Amendment Act of 2016, exploring its origins, provisions, and impact. We will analyze its specific application (or lack thereof) in different contexts, discuss the challenges it presents to businesses, and consider the broader implications for consumer protection and financial responsibility. The analysis will include discussions of similar state-level legislation and the future potential for broader federal reforms.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon legal documents, scholarly articles, news reports, and government publications related to late fees, consumer protection legislation, and relevant case law. The aim is to present a clear, unbiased, and comprehensive understanding of the Late Fee Fairness Amendment Act of 2016 and its broader context.

Key Takeaways:

- Definition and Core Concepts: A precise definition of the Late Fee Fairness Amendment Act of 2016 (where applicable) and the core principles it aims to uphold.

- Practical Applications: Examination of how the Act, or similar legislation, functions in practice across different industries and jurisdictions.

- Challenges and Solutions: Analysis of the obstacles faced by businesses in complying with the Act and potential solutions for achieving compliance while maintaining profitability.

- Future Implications: Discussion of the long-term effects of the Act and the potential for future legislative changes related to late fees.

Smooth Transition to the Core Discussion

While the Late Fee Fairness Amendment Act of 2016 might not be universally known, its underlying principles are crucial. Understanding these principles allows for a clearer understanding of the ongoing push for consumer protection in financial transactions. Let's delve into the key aspects of this legislation and its broader context.

Exploring the Key Aspects of the Late Fee Fairness Amendment Act of 2016 (and its Context)

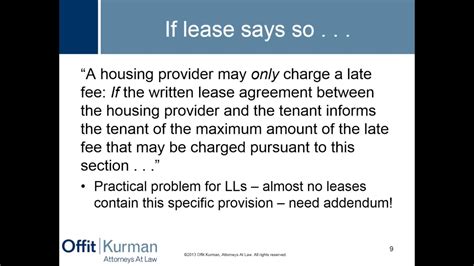

It's crucial to begin by clarifying that the "Late Fee Fairness Amendment Act of 2016" isn't a single, federally enacted law. The term refers more broadly to a trend of legislation and amendments at both the state and, in some cases, federal levels aimed at reforming late fee practices. These legislative efforts share common goals: greater transparency, limitations on excessive fees, and clearer communication between businesses and consumers regarding late payment penalties. There isn't a single, uniformly applied "Act" but rather a collection of similar state-level laws and amendments that often share similar goals and approaches.

Definition and Core Concepts:

The core concept behind the various state acts and amendments focused on late fee fairness centers on preventing exploitative practices. Many state acts aim to:

- Establish Caps on Late Fees: This prevents businesses from charging exorbitant fees disproportionate to the actual cost of processing late payments.

- Require Clear and Conspicuous Disclosure: Businesses must clearly and prominently disclose their late fee policies to consumers before a late payment occurs. This includes specifying the amount of the fee, the trigger for its application, and any other relevant details.

- Define "Late Payment": Many acts clarify what constitutes a late payment to avoid ambiguity and potential disputes.

- Limit the Number of Fees Applied: Some legislation restricts the number of late fees that can be applied to a single account within a specific period.

Applications Across Industries:

The application of late fee fairness legislation varies depending on the jurisdiction and the specific industry. It commonly affects industries like:

- Telecommunications: Late payment fees for phone and internet services.

- Utilities: Late payment charges for electricity, gas, and water services.

- Financial Services: Late fees on credit cards, loans, and mortgages (though federal regulations already exist for some aspects of this sector).

- Rentals: Late fees for rent payments.

Challenges and Solutions:

Implementing and enforcing these regulations presents several challenges:

- Variations in State Laws: The lack of a uniform federal law creates inconsistencies across states, making it challenging for businesses operating nationwide to maintain consistent compliance.

- Enforcement Difficulties: Enforcing compliance across multiple states can be resource-intensive for regulatory bodies.

- Balancing Consumer Protection and Business Viability: Finding the right balance between protecting consumers from unfair fees and allowing businesses to operate profitably is a complex task.

Solutions involve a multi-pronged approach:

- Improved Communication: Clearer and more accessible information about late fees for consumers.

- Streamlined Enforcement: Improved coordination and collaboration between state regulatory agencies.

- Industry Self-Regulation: Encouraging businesses to adopt best practices and internal controls to ensure fair late fee practices.

Impact on Innovation:

The late fee fairness movement, though not directly aimed at stimulating innovation, indirectly influences it. Businesses are incentivized to develop more efficient and consumer-friendly billing and payment systems to minimize late payments and avoid associated fees. This could lead to innovations in automated payment reminders, flexible payment options, and improved customer service channels.

Closing Insights: Summarizing the Core Discussion

The push for late fee fairness reflects a broader societal movement towards greater consumer protection and ethical business practices. While the absence of a single, overarching federal act makes direct comparison difficult, the numerous state-level legislative efforts share a common thread: the need for transparency, reasonableness, and consumer awareness concerning late payment charges.

Exploring the Connection Between Consumer Financial Literacy and Late Fee Fairness

The relationship between consumer financial literacy and the effectiveness of late fee fairness legislation is significant. Legislation alone is insufficient; consumers need the knowledge and understanding to navigate complex billing systems and avoid late fees.

Roles and Real-World Examples:

Low financial literacy contributes to a greater likelihood of late payments. Individuals lacking understanding of budgeting, credit scores, and payment deadlines are more susceptible to incurring late fees. Conversely, financially literate individuals are better equipped to manage their finances, preventing late payments and reducing the impact of late fee legislation.

Risks and Mitigations:

The risk is that even with fair late fees in place, individuals with low financial literacy may still struggle to manage their finances effectively. This necessitates a complementary approach of promoting financial education and literacy programs alongside legislative reform.

Impact and Implications:

Improved financial literacy can amplify the positive impact of late fee fairness legislation. Empowered consumers can better advocate for their rights and effectively challenge unfair late fee practices. This leads to a more equitable and just financial system.

Conclusion: Reinforcing the Connection

The interplay between consumer financial literacy and late fee fairness demonstrates that effective consumer protection requires a holistic approach. Legislation alone is not enough; efforts to promote financial literacy are equally crucial in ensuring consumers can utilize the protections afforded by these laws.

Further Analysis: Examining Consumer Financial Literacy Programs in Greater Detail

Numerous organizations and government agencies offer financial literacy programs aimed at improving consumer understanding of financial concepts, including budgeting, debt management, and credit scores. These programs utilize various methods, including online resources, workshops, and one-on-one counseling. Their effectiveness varies depending on the target audience, program design, and resources available. Evaluating the effectiveness of these programs and integrating them into broader consumer protection strategies is critical.

FAQ Section: Answering Common Questions About Late Fee Fairness Legislation

Q: What is the maximum late fee I can be charged? A: The maximum late fee varies significantly depending on the state, the type of service, and the specific legislation in place. There’s no single national limit.

Q: What happens if a company violates late fee fairness laws? A: Penalties vary by state but can include fines, legal action, and regulatory intervention.

Q: How can I avoid late fees? A: Set up automatic payments, utilize online banking tools to track due dates, and establish a system for managing your bills.

Q: Are all late fees unfair? A: No, reasonable late fees that cover administrative costs are generally considered acceptable. The issue arises when fees are excessive or disproportionate to the actual cost.

Practical Tips: Maximizing the Benefits of Late Fee Fairness Legislation

- Understand Your Rights: Familiarize yourself with your state’s late fee laws and regulations.

- Communicate Proactively: Contact your service provider immediately if you anticipate a delay in payment.

- Document Everything: Keep records of all correspondence and interactions regarding late fees.

- Dispute Unfair Fees: If you believe you’ve been charged an unfair late fee, file a formal dispute with the company and, if necessary, regulatory agencies.

Final Conclusion: Wrapping Up with Lasting Insights

The ongoing debate surrounding late fee fairness highlights the importance of balancing consumer protection with business viability. The absence of a uniform federal act underscores the need for greater coordination and collaboration between state governments, consumer advocacy groups, and businesses to create a more equitable and transparent system for managing late payments. Ultimately, ensuring both consumer protection and responsible business practices requires a multi-pronged strategy that combines legislative reform with effective consumer education and industry self-regulation. The fight for fair late fees is not simply about the amount of the fee itself; it's a reflection of the broader struggle for fair and equitable financial practices.

Latest Posts

Latest Posts

-

What Does Minimum Payment In Credit Card Mean

Apr 04, 2025

-

What Happens If I Only Pay The Minimum Payment On My Credit Card

Apr 04, 2025

-

What Is The Minimum Payment On A Balance Transfer Credit Card

Apr 04, 2025

-

What Means Minimum Payment

Apr 04, 2025

-

Why Does It Say Minimum Payment Due 0 00

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about What Is The Late Fee Fairness Amendment Act Of 2016 . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.