What Happens If I Only Pay The Minimum Payment On My Credit Card

adminse

Apr 04, 2025 · 8 min read

Table of Contents

The Minimum Payment Trap: What Happens When You Only Pay the Minimum on Your Credit Card?

What if the seemingly insignificant act of paying only the minimum on your credit card could lead to a financial crisis? This seemingly small decision can have devastating long-term consequences, significantly impacting your credit score and overall financial health.

Editor’s Note: This article on the implications of only paying minimum credit card payments has been updated today to reflect current interest rates and financial practices. Understanding the true cost of minimum payments is crucial for responsible credit card management.

Why Paying Only the Minimum Matters: Relevance, Practical Applications, and Financial Significance

The seemingly harmless act of paying only the minimum due on your credit card bill is a decision with far-reaching consequences. It's a common misconception that this practice is a viable strategy for managing debt; in reality, it's a slippery slope that can lead to accumulating debt, damaging credit scores, and even financial ruin. This article explores the hidden costs, long-term effects, and alternative strategies to effectively manage credit card debt. Understanding these implications is essential for maintaining healthy personal finances and building a strong credit history.

Overview: What This Article Covers

This article provides a comprehensive overview of the implications of only making minimum payments on credit cards. We will delve into how interest accrues, the impact on your credit score, the potential for spiraling debt, and strategies for avoiding this financial pitfall. We will also explore alternative debt management solutions and offer practical advice for responsible credit card usage. Readers will gain actionable insights and a clear understanding of the financial risks involved in minimum payment strategies.

The Research and Effort Behind the Insights

This article is based on extensive research, drawing from reputable financial websites, consumer protection agencies, and analyses of credit card agreements. Data regarding average interest rates, credit scoring models, and debt management strategies is included to ensure accuracy and provide readers with reliable information. The information presented aims to empower readers with the knowledge necessary to make informed decisions about their credit card debt.

Key Takeaways:

- High Interest Costs: Paying only the minimum prolongs the repayment period significantly, leading to substantially higher interest charges.

- Credit Score Damage: High credit utilization (the percentage of your available credit that you're using) negatively impacts your credit score. Consistently paying the minimum keeps your utilization high.

- Debt Accumulation: The slow repayment process allows interest to accumulate faster than you pay down the principal, leading to a snowball effect of increasing debt.

- Financial Stress: The constant burden of high-interest debt can cause significant financial stress and limit your ability to save and invest.

- Collection Agencies: Failure to make timely payments can result in your account being sent to collections, severely damaging your credit.

Smooth Transition to the Core Discussion

Now that we've established the potential dangers, let's explore the specifics of how minimum payments contribute to a cycle of debt. We will examine the mechanics of interest calculation, the impact on credit scores, and offer strategies for a more responsible approach to credit card management.

Exploring the Key Aspects of Paying Only the Minimum Credit Card Payment

1. Definition and Core Concepts: Understanding Credit Card Interest

Credit cards operate on a revolving credit system. This means you can borrow money up to your credit limit, and you're expected to pay back a portion of the balance each month. The minimum payment is the smallest amount your credit card issuer requires you to pay to remain in good standing. However, this minimum payment typically only covers a small fraction of your total balance. The remaining balance, plus accrued interest, rolls over to the next billing cycle.

2. Applications Across Industries: The Ubiquity of Revolving Credit

Revolving credit, the foundation of credit cards, isn't limited to personal spending. Businesses also utilize credit lines for operational expenses, inventory, and other financial needs. The same principles of minimum payments and interest accrual apply, highlighting the widespread impact of this financial mechanism. Understanding how minimum payments work across various sectors provides a comprehensive understanding of their consequences.

3. Challenges and Solutions: The Debt Spiral and Escape Strategies

The primary challenge associated with minimum payments is the debt spiral. Because the majority of your monthly payment goes toward interest, only a small portion is applied to the principal. This slow repayment allows interest to accumulate, effectively increasing your debt over time. This creates a vicious cycle where it becomes increasingly difficult to pay off the balance. Solutions include creating a budget, exploring debt consolidation options, and seeking professional financial advice.

4. Impact on Innovation: Financial Technology and Debt Management

The rise of financial technology (fintech) has brought about new tools and resources for managing debt. Apps and online platforms offer budgeting assistance, debt tracking, and even automated payment strategies. However, it's crucial to remember that technology alone cannot solve the problem of irresponsible credit card usage. Responsible financial behavior remains essential.

Closing Insights: Summarizing the Core Discussion

Paying only the minimum on your credit card is a risky strategy that can lead to a significant accumulation of debt and damage to your credit score. The high interest rates and the slow pace of repayment create a situation where the debt can snowball, making it increasingly challenging to pay off the balance. Understanding this dynamic is crucial for responsible financial management.

Exploring the Connection Between Interest Rates and Minimum Payments

The relationship between interest rates and minimum payments is pivotal. Higher interest rates exacerbate the problem of minimum payments, leading to faster debt accumulation. Let's examine this connection in detail.

Key Factors to Consider:

Roles and Real-World Examples: The impact of interest rates on minimum payments is significant. If you have a credit card with a high APR (Annual Percentage Rate), a larger portion of your minimum payment will go towards interest, leaving only a small amount to reduce the principal. A real-world example: A $5,000 balance with a 20% APR will accumulate significant interest even with consistent minimum payments.

Risks and Mitigations: The primary risk is the ever-increasing debt burden. Mitigation strategies include actively paying more than the minimum payment, refinancing to a lower interest rate, or consolidating debt into a loan with a lower APR. Negotiating with your credit card issuer for a lower interest rate is also an option.

Impact and Implications: The long-term implications of consistently paying only the minimum can be detrimental to your financial health. It can prevent you from saving, investing, and achieving long-term financial goals. It may also lead to stress and negatively affect your credit rating for years to come.

Conclusion: Reinforcing the Connection

The interplay between interest rates and minimum payments underscores the importance of understanding the true cost of credit card debt. By actively working to pay down your balance and considering options for lower interest rates, you can significantly improve your financial situation and avoid the trap of minimum payments.

Further Analysis: Examining Interest Calculation in Greater Detail

Credit card interest is typically calculated using the average daily balance method. This involves calculating the average daily balance owed throughout the billing cycle and multiplying it by the daily periodic interest rate. The result is your monthly interest charge. Understanding this calculation is crucial for comprehending the speed at which interest accrues, particularly when only paying the minimum.

FAQ Section: Answering Common Questions About Minimum Payments

What is the average minimum payment percentage? The minimum payment percentage varies depending on the credit card issuer, but it's often between 1% and 3% of the total balance.

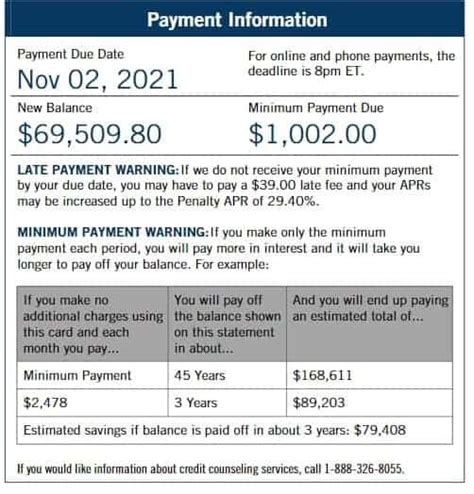

How long will it take to pay off a credit card using only minimum payments? It can take years, even decades, to pay off a credit card balance using only minimum payments, depending on the interest rate and balance.

What is a credit utilization ratio, and why does it matter? The credit utilization ratio is the percentage of your available credit that you're using. A high utilization ratio negatively impacts your credit score.

What happens if I miss a minimum payment? Missing a minimum payment results in late fees, a negative impact on your credit score, and potential collection agency involvement.

Practical Tips: Maximizing the Benefits of Responsible Credit Card Usage

- Create a Budget: Track your income and expenses to understand where your money is going.

- Pay More Than the Minimum: Even a small increase in your payment can significantly reduce the total interest paid and shorten the repayment period.

- Transfer Balances: Consider transferring your balance to a card with a lower APR (Annual Percentage Rate).

- Debt Consolidation: Explore consolidating your debt into a loan with a fixed interest rate.

- Seek Professional Help: If you're struggling with credit card debt, consider seeking help from a credit counselor.

Final Conclusion: Wrapping Up with Lasting Insights

Paying only the minimum payment on your credit card can seem like a manageable approach, but it's a deceptive strategy that can lead to a cycle of mounting debt and financial stress. Understanding the mechanics of interest accrual, the impact on your credit score, and the available debt management options is crucial for responsible credit card usage. By taking proactive steps to manage your credit card debt, you can protect your financial health and build a strong financial future. Remember, responsible credit card usage is not just about making payments; it's about understanding the long-term implications of your financial decisions.

Latest Posts

Latest Posts

-

Money Management Trading Forex

Apr 06, 2025

-

What Is Proper Money Management In Forex

Apr 06, 2025

-

How To Teach Budgeting Skills For Adults

Apr 06, 2025

-

How To Teach Someone To Manage Money

Apr 06, 2025

-

How To Teach Money Management Skills To Adults

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about What Happens If I Only Pay The Minimum Payment On My Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.