What Is A Statement Balance For Credit Card

adminse

Apr 04, 2025 · 8 min read

Table of Contents

Decoding the Mystery: Understanding Your Credit Card Statement Balance

What if a simple understanding of your credit card statement balance could save you from crippling debt? Mastering this crucial financial concept is the cornerstone of responsible credit card management.

Editor’s Note: This article on understanding credit card statement balances was published today to provide you with the most up-to-date and accurate information on navigating your credit card statements and managing your finances effectively.

Why Understanding Your Credit Card Statement Balance Matters:

In today's digital age, credit cards are ubiquitous. They offer convenience, rewards, and build credit history—but only if managed wisely. A fundamental aspect of responsible credit card use is comprehending the information presented on your monthly statement. Misunderstanding your statement balance can lead to late fees, high interest charges, and ultimately, significant debt. Understanding your statement balance allows you to budget effectively, track spending, and avoid the pitfalls of overspending and accumulating debt. This knowledge empowers you to make informed financial decisions, improving your credit score and overall financial health.

Overview: What This Article Covers

This article provides a comprehensive guide to understanding your credit card statement balance. We'll dissect the different types of balances, explain how they're calculated, and offer practical tips for managing your credit effectively. We'll explore the impact of various factors like interest rates, payment due dates, and minimum payment requirements. Finally, we'll address common questions and provide actionable strategies for maintaining a healthy credit card balance.

The Research and Effort Behind the Insights

This article is the product of extensive research, drawing upon information from reputable financial institutions, consumer protection agencies, and established financial literacy resources. The information presented is designed to be accurate and easily understandable, empowering you to take control of your credit card finances.

Key Takeaways:

- Definition and Core Concepts: A clear definition of different statement balances (previous balance, current balance, available credit, credit limit).

- Practical Applications: How to use statement information to track spending, budget effectively, and avoid interest charges.

- Challenges and Solutions: Understanding and mitigating the risks of high interest rates, late fees, and minimum payment traps.

- Future Implications: Long-term impact of responsible credit card management on credit scores and financial well-being.

Smooth Transition to the Core Discussion:

Now that we've established the importance of understanding your credit card statement, let's delve into the specifics. We'll break down the key components of a typical statement and provide clarity on how each element impacts your overall financial picture.

Exploring the Key Aspects of Your Credit Card Statement Balance

Your credit card statement provides a detailed summary of your account activity over a billing cycle. Understanding the different balances presented is crucial for responsible financial management. Let's examine the key aspects:

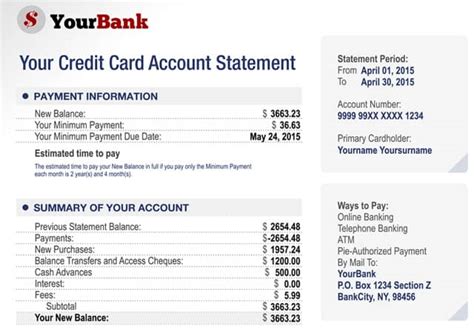

1. Previous Balance: This represents the outstanding balance from your previous billing cycle. It's the amount you owed at the end of the last statement period. It's the starting point for calculating your current balance.

2. Payments: This section details all payments made during the current billing cycle. This includes payments made online, by mail, or via phone. Note that processing time for payments can vary, so ensure your payment is received before the due date to avoid late fees.

3. Purchases: This lists all transactions made with your credit card during the current billing cycle. This includes everyday purchases, online shopping, and any other transactions charged to your account. Carefully review this section to identify any unauthorized or incorrect charges.

4. Credits: This section includes any credits applied to your account. These could be for returns, adjustments, or other credits issued by the card issuer.

5. Fees: This section displays any fees charged to your account during the billing cycle. This might include late payment fees, over-limit fees, balance transfer fees, or other applicable charges. Carefully review these fees to ensure their accuracy.

6. Interest Charges (Finance Charges): This crucial component represents the interest accrued on your outstanding balance during the billing cycle. The interest rate is determined by your credit card agreement and is typically calculated daily on the average daily balance. High interest rates can significantly impact your overall cost of borrowing.

7. Current Balance (Statement Balance): This is the total amount you owe at the end of the current billing cycle. It's calculated by adding your previous balance, purchases, and fees, then subtracting payments and credits. This is the amount you need to pay to avoid incurring further interest charges.

8. Minimum Payment Due: This is the minimum amount you're required to pay by the due date to remain in good standing with your credit card issuer. While paying only the minimum payment is technically acceptable, it’s crucial to understand that this approach will lead to significantly higher interest charges over time. It's generally advisable to pay more than the minimum payment whenever possible.

9. Available Credit: This indicates how much credit you have left available to use on your credit card. It's calculated by subtracting your current balance from your credit limit. Keeping track of your available credit helps you avoid exceeding your credit limit, which can result in additional fees.

10. Credit Limit: This is the maximum amount of credit your card issuer has approved for your account. Avoid approaching or exceeding this limit to maintain a healthy credit utilization ratio, a crucial factor influencing your credit score.

Closing Insights: Summarizing the Core Discussion

Understanding the different balances on your credit card statement is not just about numbers; it's about responsible financial management. By carefully reviewing each component of your statement, you can monitor your spending habits, identify potential errors, and avoid accumulating excessive debt. Ignoring this information can lead to financial difficulties, highlighting the importance of proactive monitoring and responsible credit card usage.

Exploring the Connection Between Interest Rates and Your Statement Balance

The interest rate plays a pivotal role in shaping your statement balance. Understanding how interest is calculated and the impact of different interest rates is crucial for effective credit card management.

Key Factors to Consider:

- Roles and Real-World Examples: A high interest rate will significantly increase your current balance, even if you make consistent payments. For instance, a $1,000 balance with a 20% APR will accrue substantially more interest than the same balance with a 10% APR.

- Risks and Mitigations: High interest rates can quickly lead to accumulating debt if you only pay the minimum payment. To mitigate this risk, pay more than the minimum payment whenever possible, and consider exploring balance transfer options to lower your interest rate.

- Impact and Implications: High interest rates significantly impact your overall cost of borrowing and can negatively affect your credit score if you fall behind on payments.

Conclusion: Reinforcing the Connection

The connection between interest rates and your statement balance is undeniable. By understanding how interest is calculated and choosing a credit card with a manageable interest rate, you can significantly impact your overall financial health.

Further Analysis: Examining APR in Greater Detail

Annual Percentage Rate (APR) is the annual interest rate charged on your outstanding credit card balance. Understanding how APR is calculated and its impact on your statement balance is paramount. APR encompasses not only the nominal interest rate but also any additional fees included in the finance charge. A lower APR will reduce the interest charged on your outstanding balance, making it easier to manage your debt.

FAQ Section: Answering Common Questions About Credit Card Statement Balances

Q: What is the difference between the current balance and the previous balance?

A: The previous balance is the amount owed at the end of the last billing cycle, while the current balance is the amount owed at the end of the current billing cycle.

Q: What happens if I only pay the minimum payment?

A: Paying only the minimum payment will significantly increase the time it takes to pay off your balance and will result in higher interest charges over time.

Q: How can I reduce my credit card balance?

A: Create a budget, prioritize paying down your balance, consider debt consolidation options, and explore balance transfer options to lower your interest rate.

Q: What is a good credit utilization ratio?

A: A good credit utilization ratio is generally considered to be below 30% of your available credit.

Q: What should I do if I see an unauthorized charge on my statement?

A: Contact your credit card issuer immediately to report the unauthorized charge and request a credit.

Practical Tips: Maximizing the Benefits of Understanding Your Credit Card Statement

- Review your statement thoroughly each month: Identify any errors, unauthorized charges, or unusually high spending.

- Create a budget: Track your spending to ensure you don't exceed your available credit.

- Pay more than the minimum payment: This will significantly reduce the time it takes to pay off your balance and reduce interest charges.

- Monitor your credit score: A healthy credit score is essential for securing loans, mortgages, and other financial products.

- Choose a credit card with a low APR: This will reduce the cost of borrowing and make managing your credit easier.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding your credit card statement balance is a fundamental aspect of responsible financial management. By mastering this concept, you equip yourself with the knowledge and tools to avoid high interest charges, prevent debt accumulation, and build a healthy financial future. Regularly reviewing your statement, understanding its components, and employing sound financial strategies will empower you to navigate the complexities of credit card usage confidently and effectively. Remember, informed decision-making is the key to unlocking financial freedom and stability.

Latest Posts

Latest Posts

-

What Is The Lowest Pay At Home Depot

Apr 05, 2025

-

What Is The Minimum Pay At Home Depot

Apr 05, 2025

-

What Is The Minimum Payment On Home Depot Credit Card

Apr 05, 2025

-

What Is The Minimum Wage For Home Depot

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about What Is A Statement Balance For Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.