What Is A Grace Period In Terms Of Credit Card Payments

adminse

Apr 02, 2025 · 9 min read

Table of Contents

What are the hidden benefits and potential pitfalls of credit card grace periods?

Understanding your grace period is crucial for responsible credit card management and avoiding unnecessary fees.

Editor’s Note: This article on credit card grace periods was published today, offering readers the most up-to-date information and insights to help them navigate their credit card accounts effectively.

Why Grace Periods Matter: Relevance, Practical Applications, and Industry Significance

A grace period on a credit card is a crucial element of responsible credit card management. It represents a window of opportunity for cardholders to pay their outstanding balance in full without incurring interest charges. This seemingly small detail significantly impacts a cardholder's finances, influencing their credit score, overall debt burden, and long-term financial health. Understanding the intricacies of a grace period—how it works, its limitations, and its potential pitfalls—is paramount for making informed financial decisions. This knowledge directly impacts a consumer's ability to avoid accumulating unnecessary debt and maintain a positive credit history. The industry significance lies in the direct correlation between consumer understanding of grace periods and the overall health of the credit market. Misunderstandings can lead to increased debt and potential financial instability for individuals and, in aggregate, can affect the broader economy.

Overview: What This Article Covers

This article provides a comprehensive overview of credit card grace periods. We will explore the definition and core concepts of grace periods, examining how they are calculated and applied by different credit card issuers. We will delve into the practical applications of understanding grace periods, highlighting scenarios where maximizing the grace period can save money. Further, we will analyze potential challenges and solutions related to grace period utilization and explore the broader implications for credit management and financial responsibility. Finally, we will address common questions surrounding grace periods and provide practical tips for leveraging this valuable feature of credit cards.

The Research and Effort Behind the Insights

This article draws upon extensive research, including analysis of credit card terms and conditions from various issuers, examination of industry reports on credit card usage, and consideration of relevant consumer protection laws. The information presented is grounded in factual data and aims to provide readers with an accurate and reliable understanding of credit card grace periods.

Key Takeaways: Summarize the Most Essential Insights

- Definition and Core Concepts: A clear definition of a credit card grace period, including its essential components and how it relates to interest charges.

- Calculation and Application: An explanation of how grace periods are calculated and the factors that can influence their duration.

- Practical Applications: Real-world examples of how to maximize the grace period to minimize interest payments.

- Challenges and Solutions: Potential obstacles in utilizing grace periods and effective strategies to overcome them.

- Impact on Credit Scores: The influence of grace period utilization (or lack thereof) on an individual's credit score.

- Future Implications: Long-term financial consequences of understanding and utilizing (or failing to utilize) grace periods.

Smooth Transition to the Core Discussion

Having established the importance of understanding credit card grace periods, let’s now delve into a detailed examination of its core aspects, exploring its practical applications, potential challenges, and its significant influence on personal finance.

Exploring the Key Aspects of Grace Periods

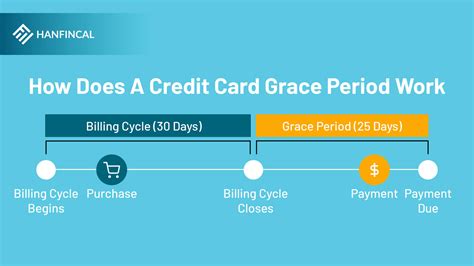

Definition and Core Concepts: A grace period, in the context of credit card payments, is the time frame a cardholder has after their billing cycle ends to pay their statement balance in full without incurring interest charges. This period is typically 21 to 25 days, but it can vary depending on the issuer and the specific card agreement. It’s crucial to understand that the grace period only applies to the previous billing cycle's purchases and balance transfers. Any new transactions made during the grace period will accrue interest from the transaction date.

Calculation and Application: The grace period calculation begins on the day the billing cycle ends. The due date is usually printed clearly on the monthly statement. It's essential to note that making even a partial payment during the grace period does not extend the grace period; interest will still accrue on the unpaid balance. To avoid interest, the entire statement balance must be paid by the due date.

Applications Across Industries: While the concept of a grace period is consistent across the credit card industry, specific terms and conditions can vary slightly. Some issuers may offer promotional periods with extended grace periods or other incentives. Understanding these nuances requires careful review of the individual cardholder agreement.

Challenges and Solutions: One primary challenge lies in accurately tracking spending and managing payments. Overspending and failure to pay the statement balance in full before the due date are common reasons for losing the grace period benefit and accruing interest charges. Solutions include budgeting tools, setting up automatic payments, and closely monitoring credit card statements. Another challenge is understanding the complexities of different credit card types and their associated grace period terms. Solutions include carefully reading the terms and conditions and contacting the credit card issuer for clarifications.

Impact on Innovation: The grace period concept hasn't seen significant innovation in recent years. However, the emphasis on transparency and consumer protection has led to clearer communication of grace period terms on credit card statements and agreements.

Closing Insights: Summarizing the Core Discussion

The grace period is a powerful tool that can significantly reduce the overall cost of using credit cards when utilized correctly. However, it’s not a license for overspending; responsible spending and timely payment remain crucial for managing credit card debt effectively. Failure to utilize the grace period appropriately can lead to accumulating significant interest charges, impacting financial well-being and credit scores.

Exploring the Connection Between Late Payments and Grace Periods

Late payments represent a critical juncture where the benefits of a grace period are lost. The relationship between late payments and grace periods is inverse; a missed due date eliminates the grace period's protective effect, immediately subjecting the outstanding balance to interest charges.

Key Factors to Consider:

Roles and Real-World Examples: Consider a cardholder who consistently pays their credit card balance in full by the due date. They effectively leverage the grace period, enjoying the benefit of interest-free credit for purchases made during the billing cycle. Conversely, a cardholder who consistently misses payments will accrue interest from the transaction date, leading to significantly higher costs.

Risks and Mitigations: The primary risk associated with late payments is the accumulation of interest charges and potential penalties. This can lead to a snowball effect of debt, harming credit scores and overall financial health. Mitigations include setting reminders, automating payments, or utilizing budgeting apps to track spending and ensure timely payments.

Impact and Implications: The long-term impact of consistently late payments is substantial. It can lead to a damaged credit score, impacting future loan applications, insurance rates, and even employment opportunities. Furthermore, late payments can lead to higher interest rates on future credit products, creating a cycle of debt that's difficult to break.

Conclusion: Reinforcing the Connection

The link between late payments and the loss of the grace period's benefits is undeniable. Responsible credit card usage hinges on understanding this connection and implementing strategies to ensure timely payments, maximizing the grace period's value and avoiding the pitfalls of late payment penalties and escalating debt.

Further Analysis: Examining Late Payment Penalties in Greater Detail

Late payment penalties are a significant financial consequence of missing the due date on a credit card payment. These penalties vary depending on the issuer and the card agreement, but they often include additional fees and higher interest rates. The impact of these penalties on an individual's credit score can be substantial, leading to a decreased credit rating and making it more difficult to secure loans or other credit products in the future.

FAQ Section: Answering Common Questions About Grace Periods

What is a grace period? A grace period is the time given after the billing cycle ends to pay your balance in full without incurring interest.

How is the grace period calculated? It begins after the billing cycle ends and ends on the due date stated on your statement.

What happens if I make a partial payment during the grace period? Interest will still be charged on the remaining balance. Only paying the entire statement balance avoids interest charges.

Does the grace period apply to cash advances? No, grace periods generally do not apply to cash advances or balance transfers. These transactions typically accrue interest from the transaction date.

What happens if I miss my due date? You will lose your grace period and accrue interest on your outstanding balance. You may also be subject to late payment fees.

How can I avoid losing my grace period? Ensure you pay your statement balance in full by the due date. Set up automatic payments or reminders to avoid missing payments.

Practical Tips: Maximizing the Benefits of Grace Periods

-

Understand Your Statement: Carefully review your credit card statement each month to understand your billing cycle, due date, and outstanding balance.

-

Budget and Track Spending: Create a budget and track your spending to ensure you can pay your balance in full by the due date.

-

Set Reminders: Set up reminders on your phone or calendar to ensure you don't miss your payment due date.

-

Automate Payments: Consider setting up automatic payments to ensure your payment is made on time each month.

-

Review Your Card Agreement: Familiarize yourself with the terms and conditions of your credit card agreement, paying close attention to the grace period details.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding and effectively utilizing the grace period offered by credit cards is a cornerstone of responsible credit management. By paying attention to billing cycles, due dates, and maintaining diligent tracking of expenses, individuals can significantly minimize the cost of credit and preserve their financial health. Ignoring the grace period's intricacies, however, can lead to substantial debt accumulation and damage to one's creditworthiness. The knowledge gained from this article empowers consumers to make informed decisions, ensuring they can leverage this valuable benefit and maintain control over their finances.

Latest Posts

Latest Posts

-

How Do Credit Card Companies Determine Your Minimum Payment

Apr 04, 2025

-

How Do Credit Card Companies Calculate Your Minimum Payment

Apr 04, 2025

-

How Do Credit Card Companies Determine Minimum Payment Due

Apr 04, 2025

-

How Do Credit Card Companies Work Out Minimum Payment

Apr 04, 2025

-

How Does Credit Card Company Calculate Minimum Payment

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about What Is A Grace Period In Terms Of Credit Card Payments . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.