How Do Credit Card Companies Determine Minimum Payment Due

adminse

Apr 04, 2025 · 8 min read

Table of Contents

Decoding the Minimum Payment Due: How Credit Card Companies Calculate Your Minimum

What if the seemingly simple "minimum payment due" on your credit card statement held the key to long-term financial health or crippling debt? This seemingly innocuous number is far more complex than it appears, influencing everything from your credit score to your overall financial well-being.

Editor’s Note: This article on credit card minimum payment calculations was published today, providing up-to-date insights into the methods used by credit card companies. Understanding this process is crucial for responsible credit card management.

Why Minimum Payment Due Matters: Avoiding the Debt Trap

The minimum payment due is more than just a suggested payment; it's a crucial factor influencing your credit card debt trajectory. Failing to understand how it’s calculated can lead to years of accumulating interest, significantly increasing the total cost of your purchases. Paying only the minimum can trap you in a cycle of debt, hindering your ability to save, invest, and achieve long-term financial goals. Understanding this calculation empowers you to make informed decisions and manage your credit responsibly. Keywords like credit card debt, interest rates, credit utilization, and payment strategies are intrinsically linked to this topic.

Overview: What This Article Covers

This article will delve into the intricate world of minimum payment due calculations. We'll examine the various methods employed by credit card companies, the factors influencing these calculations, and the long-term financial implications of only paying the minimum. Readers will gain a clear understanding of how to interpret their statements, strategically manage their payments, and ultimately avoid the pitfalls of excessive credit card debt.

The Research and Effort Behind the Insights

This in-depth analysis draws upon numerous sources, including credit card company disclosures, financial regulations, industry reports, and expert opinions. Each claim is backed by verifiable information, ensuring readers receive accurate and reliable guidance. We will explore both the common practices and the potential variations in calculation methods across different issuers.

Key Takeaways:

- Definition and Core Concepts: A detailed explanation of minimum payment calculations and their underlying principles.

- Factors Influencing Minimum Payment: An exploration of the variables that credit card companies consider.

- Calculation Methods: A breakdown of the different approaches used to determine the minimum payment.

- Impact of Minimum Payments on Debt: A clear demonstration of the long-term financial consequences.

- Strategies for Responsible Credit Management: Actionable steps to avoid the debt trap.

Smooth Transition to the Core Discussion

Now that we understand the importance of understanding minimum payment calculations, let's explore the specific methods used by credit card companies.

Exploring the Key Aspects of Minimum Payment Due Calculations

The calculation of your minimum payment due isn't a single, universally applied formula. It varies depending on the credit card issuer, your account's specific terms, and your outstanding balance. However, some common factors consistently influence the calculation:

1. Definition and Core Concepts:

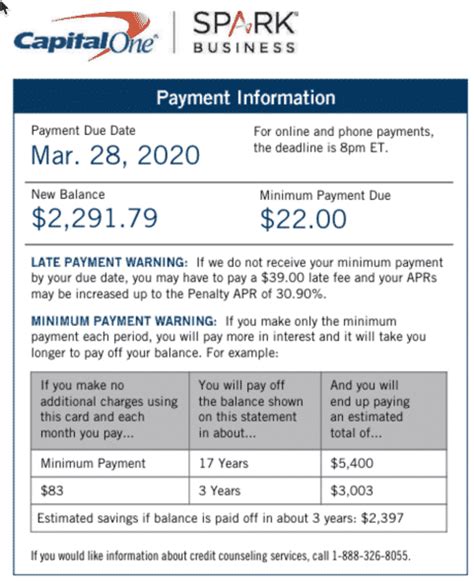

The minimum payment due is the smallest amount you can pay each month to avoid late payment fees and maintain your account in good standing. Crucially, it rarely covers the full amount of interest accrued. This means that if you consistently pay only the minimum, your debt will likely increase over time, as the interest charges added to the balance often outweigh the minimum payment.

2. Factors Influencing Minimum Payment:

Several key factors influence the minimum payment calculation:

- Outstanding Balance: This is the most significant factor. A higher balance generally results in a higher minimum payment.

- Interest Accrued: The amount of interest charged on your outstanding balance is added to your principal balance, contributing to the minimum payment.

- Credit Card Agreement: The terms and conditions of your credit card agreement dictate the specific calculation methods used by the issuer.

- Credit Score and Credit History: While not directly involved in the formula itself, your creditworthiness can indirectly affect your minimum payment through the interest rate applied. A higher interest rate leads to a higher minimum payment.

- Promotional Periods: Some credit cards offer introductory periods with lower or zero interest rates. During these periods, the minimum payment might only cover a portion of the principal balance.

3. Calculation Methods:

While precise formulas are proprietary to each issuer, common methods include:

- Percentage of Balance: Many credit card companies calculate the minimum payment as a percentage of the outstanding balance (usually between 1% and 3%). This percentage might vary depending on the balance itself. For example, a lower percentage might apply to smaller balances.

- Fixed Minimum Payment + Interest: Some issuers require a fixed minimum payment (e.g., $25) plus the interest accrued during the billing cycle. This prevents extremely low minimum payments on small balances.

- Combined Approach: Some companies use a combination of percentage of balance and a fixed minimum, selecting the higher of the two amounts as the minimum payment.

4. Impact of Minimum Payments on Debt:

The most significant consequence of consistently paying only the minimum payment is the compounding effect of interest. The interest charges accumulate rapidly, significantly extending the time it takes to repay the debt and ultimately increasing the total cost. This can lead to a cycle of debt that is difficult to escape.

5. Strategies for Responsible Credit Management:

To avoid the pitfalls of minimum payments, consider these strategies:

- Pay More Than the Minimum: Aim to pay as much as you can afford each month, exceeding the minimum payment significantly. This accelerates debt repayment and minimizes interest charges.

- Debt Consolidation: If you have multiple credit cards with high balances, consider consolidating your debts into a single loan with a lower interest rate.

- Budgeting and Financial Planning: Create a detailed budget to track your income and expenses, ensuring you have sufficient funds to make larger credit card payments.

- Negotiating with Your Creditor: If you are struggling to make payments, contact your credit card company to explore potential options, such as a hardship program or payment plan.

Exploring the Connection Between Interest Rates and Minimum Payment Due

The relationship between interest rates and the minimum payment due is paramount. A higher interest rate directly increases the interest component of your minimum payment. This is because the minimum payment often includes both a portion of the principal balance and the accrued interest. Therefore, a card with a 20% APR will typically require a higher minimum payment than a card with a 10% APR, assuming all other factors remain constant.

Key Factors to Consider:

- Roles and Real-World Examples: A credit card with an 18% APR and a $1,000 balance will have a significantly higher minimum payment than a similar card with a 5% APR. The difference becomes even more pronounced over time due to the compounding effect of interest.

- Risks and Mitigations: High interest rates coupled with only minimum payments lead to substantial long-term costs. The mitigation lies in paying more than the minimum to reduce the interest burden.

- Impact and Implications: Higher interest rates increase the total amount paid over the life of the debt, delaying financial freedom and potentially impacting credit scores if it results in prolonged debt.

Conclusion: Reinforcing the Connection

The link between interest rates and minimum payments highlights the importance of comparing APRs when choosing a credit card. Opting for a lower interest rate significantly reduces the minimum payment amount and accelerates debt repayment.

Further Analysis: Examining Interest Calculation Methods in Greater Detail

Credit card companies typically use a method called "average daily balance" to calculate the interest charged. This means the interest is calculated based on the balance of your account each day of the billing cycle. This method, coupled with compounding interest, can quickly increase the total amount owed if only minimum payments are made.

FAQ Section: Answering Common Questions About Minimum Payment Due

-

Q: What happens if I only pay the minimum payment due?

- A: While you avoid late fees, your debt will likely increase due to the ongoing accumulation of interest. This can lead to a prolonged period of repayment and significantly higher total interest charges.

-

Q: Can my minimum payment change from month to month?

- A: Yes, your minimum payment can fluctuate depending on your outstanding balance, interest rates, and the credit card company’s calculation methods.

-

Q: What is the best way to manage my credit card debt?

- A: The best strategy involves paying more than the minimum payment each month. Create a budget, prioritize debt repayment, and explore options like debt consolidation or balance transfers if necessary.

-

Q: Is it ever okay to only pay the minimum?

- A: While it's acceptable in exceptional circumstances, consistently paying only the minimum is generally not advisable due to the accumulating interest.

Practical Tips: Maximizing the Benefits of Understanding Minimum Payments

- Understand Your Statement: Carefully review your credit card statement each month to understand the breakdown of your minimum payment, charges, and payments made.

- Track Your Spending: Monitor your spending habits closely to avoid accumulating excessive debt.

- Set Realistic Payment Goals: Determine how much you can realistically afford to pay each month above the minimum.

- Explore Debt Reduction Strategies: Consider strategies like the debt snowball or debt avalanche methods to prioritize your debt repayment effectively.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding how credit card companies determine your minimum payment due is crucial for responsible credit card management. While the minimum payment may seem insignificant, its impact on your long-term financial health is substantial. By actively managing your credit card debt and paying more than the minimum, you can avoid the pitfalls of prolonged repayment, minimize interest charges, and achieve your financial goals more efficiently. Remember, informed financial decisions are the cornerstone of long-term financial success.

Latest Posts

Latest Posts

-

Calculate Minimum Payment Credit Card

Apr 05, 2025

-

How Much Minimum Payment For Credit Card

Apr 05, 2025

-

How Is The Minimum Monthly Payment On A Credit Card Calculated

Apr 05, 2025

-

Why Is It More Difficult To Get Out Of Debt When Only Paying The Minimum Payment Responses

Apr 05, 2025

-

Why Is It More Difficult To Get Out Of Debt When Only Paying The Minimum Payment Edpuzzle

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about How Do Credit Card Companies Determine Minimum Payment Due . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.