What Does A Liquidity Ratio Measure In A Company

adminse

Apr 04, 2025 · 9 min read

Table of Contents

Decoding Liquidity: What Liquidity Ratios Measure in a Company

What if a company's ability to meet its short-term obligations determined its very survival? Liquidity ratios are the critical financial gauges that reveal a company's capacity to navigate the immediate demands of its operations and debts, providing invaluable insights for investors, creditors, and management alike.

Editor’s Note: This article on liquidity ratios provides a comprehensive overview of their calculation, interpretation, and significance in assessing a company's financial health. We've included real-world examples and actionable insights to help readers better understand this crucial aspect of financial analysis.

Why Liquidity Ratios Matter: Relevance, Practical Applications, and Industry Significance

Liquidity, simply put, refers to a company's ability to convert assets into cash quickly to meet its short-term financial obligations. These obligations typically include salaries, supplier payments, loan repayments, and other expenses due within a year. A company with strong liquidity can comfortably meet these obligations, while one with weak liquidity may face financial distress, potentially leading to bankruptcy. Understanding liquidity ratios is crucial for:

- Investors: Assessing the financial stability and risk associated with investing in a company.

- Creditors: Evaluating the creditworthiness of a company before extending loans or credit lines.

- Management: Monitoring the company's financial health, identifying potential liquidity issues, and making informed decisions regarding operations and financing.

- Suppliers: Determining the reliability of a company's ability to pay for goods and services.

Overview: What This Article Covers

This article will delve deep into the world of liquidity ratios. We will explore the most commonly used ratios, their calculation methods, interpretation, limitations, and the crucial insights they offer. We'll also examine the relationship between liquidity and profitability, and how different industries may exhibit varying levels of acceptable liquidity. Finally, we'll address frequently asked questions and provide practical tips for using liquidity ratios effectively.

The Research and Effort Behind the Insights

This article draws upon extensive research from reputable financial sources, including academic publications, industry reports, and financial statements of publicly traded companies. The analysis presented is data-driven and aims to provide a clear and accurate understanding of liquidity ratios and their significance.

Key Takeaways:

- Definition and Core Concepts: A clear explanation of liquidity and the types of liquidity ratios.

- Calculation and Interpretation: Step-by-step guides on calculating and interpreting key liquidity ratios.

- Industry Benchmarks: Understanding how liquidity ratios vary across different industries.

- Limitations of Liquidity Ratios: Recognizing the potential drawbacks and limitations of relying solely on liquidity ratios.

- Practical Applications: Real-world examples demonstrating the use of liquidity ratios in financial analysis.

Smooth Transition to the Core Discussion:

Now that we understand the importance of liquidity ratios, let's explore the key aspects of these critical financial metrics.

Exploring the Key Aspects of Liquidity Ratios

Several ratios are used to assess a company's liquidity. The most common are:

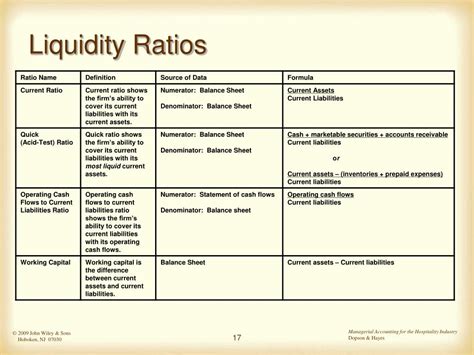

1. Current Ratio: This is the most widely used liquidity ratio. It measures a company's ability to pay its short-term liabilities (due within one year) with its current assets (assets expected to be converted into cash within one year).

- Formula: Current Ratio = Current Assets / Current Liabilities

- Interpretation: A higher current ratio generally indicates stronger liquidity. A ratio of 1.0 or higher is typically considered acceptable, although the ideal ratio varies by industry. A ratio below 1.0 suggests the company may struggle to meet its short-term obligations.

Example: If a company has current assets of $1,000,000 and current liabilities of $500,000, its current ratio is 2.0 (1,000,000 / 500,000). This indicates strong liquidity.

2. Quick Ratio (Acid-Test Ratio): This ratio is a more stringent measure of liquidity than the current ratio. It excludes inventories from current assets because inventories may not be easily or quickly converted into cash.

- Formula: Quick Ratio = (Current Assets - Inventories) / Current Liabilities

- Interpretation: Similar to the current ratio, a higher quick ratio indicates stronger short-term liquidity. A ratio of 1.0 or higher is often considered healthy, but the ideal level depends on the specific industry and company circumstances.

Example: Using the same company example above, if inventories are $300,000, the quick ratio would be 1.4 ((1,000,000 - 300,000) / 500,000). This still suggests good liquidity, but less than the current ratio because inventory is excluded.

3. Cash Ratio: This is the most conservative measure of liquidity. It considers only the most liquid assets – cash and cash equivalents – to assess the ability to meet short-term obligations.

- Formula: Cash Ratio = (Cash + Cash Equivalents) / Current Liabilities

- Interpretation: A higher cash ratio is always preferable, indicating a greater ability to meet immediate obligations. However, a very high cash ratio might suggest the company is not efficiently using its assets.

Example: If the company has $200,000 in cash and cash equivalents, its cash ratio would be 0.4 ($200,000 / $500,000). This indicates a relatively lower level of immediate liquidity compared to the other ratios.

4. Operating Cash Flow Ratio: This ratio measures the company's ability to pay off current liabilities using its operating cash flow.

- Formula: Operating Cash Flow Ratio = Operating Cash Flow / Current Liabilities

- Interpretation: A higher ratio indicates a stronger ability to meet short-term obligations using cash generated from operations. A ratio greater than 1.0 is usually considered favorable.

Example: If the company's operating cash flow is $700,000, the operating cash flow ratio would be 1.4 ($700,000 / $500,000), indicating robust liquidity supported by strong operating cash flow.

Applications Across Industries:

The appropriate level of liquidity varies significantly across industries. Companies in industries with high inventory turnover, like grocery stores, might have lower current ratios than companies in industries with lower turnover, like manufacturing. Similarly, companies with stable and predictable cash flows might maintain lower liquidity ratios than those with volatile cash flows.

Challenges and Solutions:

While high liquidity ratios suggest a company's financial strength, excessively high ratios might indicate inefficient asset management. The company may be holding too much cash or inventory, which could be invested more profitably. Conversely, low liquidity ratios can signal potential financial distress. Companies facing such challenges may need to improve cash flow management, reduce expenses, secure additional financing, or sell assets to improve their liquidity position.

Impact on Innovation:

While not a direct measure of innovation, strong liquidity provides the financial breathing room for companies to pursue innovation initiatives. Companies with sufficient liquidity can invest in research and development, acquire new technologies, or expand into new markets, without jeopardizing their ability to meet short-term obligations.

Exploring the Connection Between Profitability and Liquidity

While liquidity and profitability are distinct concepts, they are interconnected. Profitable companies generally generate strong cash flows, which contribute positively to liquidity. However, a highly profitable company can still face liquidity problems if its cash flows are not efficiently managed or if its receivables are not collected promptly.

Key Factors to Consider:

Roles and Real-World Examples: Companies like Walmart, with their high inventory turnover and efficient supply chain, often maintain lower current ratios compared to companies in capital-intensive industries like manufacturing. A startup company might initially exhibit low liquidity ratios as it invests in growth, while a mature company with stable cash flows might demonstrate consistently high liquidity.

Risks and Mitigations: A decline in the current ratio over time may signal a deterioration in liquidity and warrant further investigation into the company's operations and financial policies. Mitigating such risks might involve improving collection processes, negotiating better payment terms with suppliers, or securing additional financing.

Impact and Implications: Sustained low liquidity can result in difficulties in meeting short-term obligations, leading to financial distress, loss of investor confidence, and potentially bankruptcy. Conversely, strong liquidity provides resilience against economic downturns and allows for strategic opportunities.

Conclusion: Reinforcing the Connection Between Profitability and Liquidity

The interplay between profitability and liquidity underscores the importance of holistic financial analysis. While profitability fuels liquidity, efficient management of working capital and cash flows is crucial to ensure a company's ability to meet its short-term obligations.

Further Analysis: Examining Working Capital Management in Greater Detail

Effective working capital management is vital for maintaining strong liquidity. This involves optimizing the management of current assets (cash, accounts receivable, inventory) and current liabilities (accounts payable, short-term debt). Strategies include improving inventory management techniques (e.g., Just-in-Time inventory), implementing efficient collection procedures for accounts receivable, and negotiating favorable payment terms with suppliers.

FAQ Section: Answering Common Questions About Liquidity Ratios

Q: What is the best liquidity ratio to use?

A: There's no single "best" ratio. The most appropriate ratio depends on the specific circumstances and the nature of the business. Analysts often use multiple ratios in conjunction to gain a more comprehensive understanding of a company's liquidity.

Q: What constitutes a "good" liquidity ratio?

A: A "good" liquidity ratio varies by industry. A ratio of 1.0 or higher for the current and quick ratios is generally considered acceptable, but industries with high inventory turnover might have lower ratios. The operating cash flow ratio above 1.0 is generally viewed as positive.

Q: How can I improve my company's liquidity?

A: Strategies include improving cash flow management, reducing expenses, negotiating better payment terms with suppliers, selling off non-essential assets, and securing additional financing.

Practical Tips: Maximizing the Benefits of Liquidity Ratio Analysis

- Compare ratios over time: Analyze trends in liquidity ratios over several periods to identify potential problems or improvements.

- Compare to industry benchmarks: Compare the company's liquidity ratios to those of its competitors to assess its relative position.

- Consider qualitative factors: Liquidity ratios should be considered alongside other qualitative factors, such as management expertise, market conditions, and overall economic outlook.

- Use multiple ratios: Don't rely on just one ratio; use several to get a complete picture of the company's liquidity.

Final Conclusion: Wrapping Up with Lasting Insights

Liquidity ratios are essential tools for assessing a company's short-term financial health. By understanding how to calculate and interpret these ratios, investors, creditors, and managers can gain valuable insights into a company's ability to meet its financial obligations and navigate unforeseen challenges. A well-rounded analysis considering both quantitative (liquidity ratios) and qualitative factors provides the most comprehensive and reliable assessment of a company's financial standing. Effective liquidity management is crucial not only for short-term survival but also for long-term success and growth.

Latest Posts

Latest Posts

-

What Will Be My Minimum Payment On Credit Card

Apr 05, 2025

-

How Is Minimum Payment Calculated Wells Fargo Credit Card

Apr 05, 2025

-

How Is The Minimum Payment Calculated On A 0 Credit Card

Apr 05, 2025

-

How Is The Minimum Payment Calculated On Chase Credit Cards

Apr 05, 2025

-

How Is The Minimum Payment Calculated For Credit Card

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about What Does A Liquidity Ratio Measure In A Company . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.