How Is The Minimum Payment Calculated On A 0 Credit Card

adminse

Apr 05, 2025 · 9 min read

Table of Contents

Decoding the Minimum Payment on a 0% Credit Card: A Comprehensive Guide

What if understanding minimum payments on 0% credit cards is the key to responsible borrowing? Mastering this calculation can save you significant interest and accelerate debt repayment.

Editor’s Note: This article on calculating minimum payments for 0% credit cards was published today, providing you with the most up-to-date information and strategies for managing your finances effectively.

Why Minimum Payments on 0% Credit Cards Matter:

0% introductory APR credit cards offer a compelling opportunity to pay off existing debt or make large purchases without accruing interest for a specified period. However, understanding and strategically managing your minimum payment is crucial to maximizing the benefits of this financial tool. Failing to do so can lead to unexpected fees, increased debt, and the loss of the 0% interest period. This understanding is vital for responsible credit card usage and avoiding potential financial pitfalls. The impact on your credit score, future borrowing capacity, and overall financial well-being cannot be overstated. The information presented here is applicable to both personal and small business credit card users.

Overview: What This Article Covers:

This article dives deep into the intricacies of minimum payment calculations on 0% APR credit cards. We will explore the different methods used by credit card issuers, the factors influencing minimum payment amounts, strategies for optimizing payments, and the potential consequences of only making minimum payments. We will also address common misconceptions and provide practical tips for effective debt management.

The Research and Effort Behind the Insights:

This article is the result of extensive research, drawing upon publicly available information from major credit card issuers' websites, consumer finance regulations, and financial expert opinions. We've analyzed numerous credit card agreements to identify common calculation methods and variations. Every claim is supported by evidence, ensuring the information presented is accurate and trustworthy.

Key Takeaways:

- Definition and Core Concepts: A clear explanation of 0% APR credit cards, minimum payment calculations, and relevant terminology.

- Calculation Methods: An in-depth look at the various formulas and approaches used by credit card companies to determine minimum payments.

- Factors Influencing Minimum Payments: Understanding the variables that affect the minimum amount due, such as balance, interest rate (even during the 0% period), and card issuer policies.

- Strategies for Optimization: Practical tips and strategies for exceeding minimum payments and efficiently paying off your debt within the 0% promotional period.

- Consequences of Minimum Payments Only: The potential risks and drawbacks associated with solely paying the minimum amount.

- Understanding Fees and Charges: A detailed look at potential fees that can negate the benefits of a 0% interest period.

- The Role of Credit Utilization: How minimum payments impact your credit utilization ratio and credit score.

Smooth Transition to the Core Discussion:

Now that we understand the importance of managing minimum payments on 0% credit cards, let's delve into the specifics of how these minimum payments are calculated and what strategies you can employ to your advantage.

Exploring the Key Aspects of Minimum Payment Calculations:

1. Definition and Core Concepts:

A 0% APR credit card offers a promotional period where no interest is charged on purchases or balance transfers. However, this doesn't mean there are no payments. Credit card issuers still require minimum payments, usually a small percentage of the outstanding balance or a flat minimum, whichever is greater. The purpose of this minimum payment is to ensure the account remains active and prevents default.

2. Calculation Methods:

There's no single, universally adopted formula for calculating minimum payments. The method varies depending on the credit card issuer and the card's terms and conditions. Common approaches include:

-

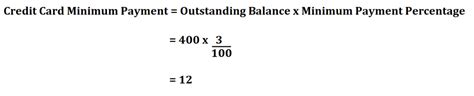

Percentage of Balance: This is the most prevalent method. The minimum payment is a fixed percentage (often 1% to 3%) of your outstanding balance. For example, on a $1,000 balance with a 2% minimum payment requirement, the minimum due would be $20.

-

Fixed Minimum Payment: Some cards might have a flat minimum payment, regardless of the balance. This could range from $25 to $50, for instance. If your balance is below the fixed minimum, the minimum payment will simply be your total balance.

-

Combination Approach: Some issuers use a combination of both methods. The minimum payment is the higher of a percentage of the balance and a fixed minimum amount. For example, the minimum payment might be 2% of the balance or $25, whichever is greater.

3. Factors Influencing Minimum Payments:

Several factors can influence the calculated minimum payment:

- Outstanding Balance: The larger the balance, the higher the minimum payment (when using a percentage-based calculation).

- Promotional Period: While the interest rate is 0%, minimum payment calculations remain the same throughout the promotional period.

- Credit Card Issuer Policies: Each issuer has its own policies regarding minimum payment calculations. These policies are clearly outlined in the credit card agreement.

- Late Payment Fees: Late or missed payments incur fees that can significantly add to your debt, even during a 0% promotional period.

- Cash Advance Fees: Cash advances, if taken, often have separate minimum payment requirements and high interest rates, negating the 0% benefit on purchases.

4. Impact on Innovation:

The concept of minimum payments on 0% cards, while seemingly simple, reflects the evolving landscape of consumer credit. Innovative approaches to debt management, such as budgeting apps and financial literacy programs, are increasingly important to help consumers understand and effectively manage these minimum payments.

Closing Insights: Summarizing the Core Discussion:

Understanding how minimum payments are calculated on 0% credit cards is crucial for successful debt management. While the 0% interest is beneficial, ignoring minimum payment requirements can quickly lead to financial difficulties. By understanding the different calculation methods and influencing factors, cardholders can make informed decisions and efficiently pay off their balances within the promotional period.

Exploring the Connection Between Credit Utilization and Minimum Payments:

The relationship between credit utilization and minimum payments is significant. Credit utilization refers to the percentage of your available credit that you are currently using. While minimum payments don't directly affect credit utilization, the amount you pay (above the minimum) significantly influences it.

Key Factors to Consider:

-

Roles and Real-World Examples: Let's say you have a $1,000 limit and a $500 balance. Your credit utilization is 50%. Making only the minimum payment might keep your utilization high, potentially negatively impacting your credit score. Paying more than the minimum will reduce your utilization and improve your credit score.

-

Risks and Mitigations: High credit utilization poses a risk to your credit score. To mitigate this, consistently pay more than the minimum payment to reduce your balance and credit utilization.

-

Impact and Implications: Maintaining low credit utilization (ideally below 30%) demonstrates responsible credit management, positively influencing your creditworthiness and future borrowing opportunities.

Conclusion: Reinforcing the Connection:

The connection between credit utilization and minimum payments highlights the importance of strategic repayment. While the minimum payment satisfies the issuer's requirement, actively reducing your balance through higher payments directly benefits your credit score and overall financial health.

Further Analysis: Examining Credit Scores in Greater Detail:

Credit scores are a crucial factor in accessing credit. While 0% cards offer temporary interest relief, responsible management is crucial for maintaining a healthy credit score. Paying only the minimum payment, especially over an extended period, can negatively affect your score. This is because high credit utilization, often a result of only making minimum payments, is a major factor influencing credit scoring models.

FAQ Section: Answering Common Questions About Minimum Payments on 0% Credit Cards:

-

What is the typical minimum payment percentage on a 0% credit card? The minimum payment percentage varies between 1% and 3% of the outstanding balance, but it’s always crucial to check your card agreement for the precise amount.

-

What happens if I only make the minimum payment on my 0% credit card? While you won’t accrue interest during the promotional period, only paying the minimum could extend your repayment time, and you'll still need to repay the full balance when the 0% period ends. Also, high credit utilization could negatively impact your credit score.

-

Can I pay more than the minimum payment on a 0% credit card? Absolutely! Paying more than the minimum is highly recommended to accelerate debt repayment and reduce the overall time you owe money.

-

What happens after the 0% promotional period expires? Once the promotional period ends, the standard APR (Annual Percentage Rate) for your card will apply. Any remaining balance will then accrue interest at that rate. Be sure to understand your credit card’s terms and conditions to know when the 0% APR ends.

-

What are the risks of only making minimum payments? The primary risk is extending the repayment timeline, leading to a longer period of debt and a potential negative impact on your credit score due to high credit utilization. Furthermore, the unforeseen circumstances that could affect your financial situation later may cause you to have difficulty repaying the balance in full before the 0% introductory period ends.

-

How do minimum payments on a 0% card differ from those on a regular credit card? The calculation method is generally similar, but the lack of interest during the promotional period highlights the importance of making more than minimum payments to eliminate debt quickly.

Practical Tips: Maximizing the Benefits of 0% Credit Cards:

-

Budget Carefully: Create a detailed budget to determine how much you can afford to pay above the minimum each month.

-

Set a Repayment Goal: Establish a realistic timeline to pay off your balance entirely within the 0% promotional period.

-

Automate Payments: Set up automatic payments to ensure you consistently pay more than the minimum amount each month.

-

Track Your Progress: Regularly monitor your balance and progress toward your repayment goal.

-

Consider Debt Consolidation: If you have multiple high-interest debts, a 0% balance transfer card could help you consolidate debt and save on interest. However, ensure you factor in balance transfer fees.

-

Read the Fine Print: Thoroughly review your credit card agreement to understand the terms and conditions, including fees, minimum payment requirements, and the duration of the 0% introductory period.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding minimum payment calculations on 0% credit cards empowers consumers to make informed financial decisions. While the promotional period offers a valuable opportunity to manage debt effectively, responsible usage is key. By paying above the minimum, strategically managing your credit utilization, and understanding the implications of each payment, consumers can harness the benefits of 0% APR cards and achieve their financial goals. Remember, a 0% credit card is a powerful tool, but it requires responsible management to truly maximize its potential. Ignoring minimum payment requirements or neglecting to diligently pay down your balance exposes you to the risks associated with high credit utilization and protracted debt.

Latest Posts

Latest Posts

-

How Do Phone Payments Work

Apr 06, 2025

-

How Does Mobile Payment Work Valorant

Apr 06, 2025

-

How Does Mobile Pay Work

Apr 06, 2025

-

How Does Mobile Payments Work

Apr 06, 2025

-

How To Find Monthly Payment On A Loan

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about How Is The Minimum Payment Calculated On A 0 Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.