Grace Period In Health Insurance

adminse

Apr 02, 2025 · 9 min read

Table of Contents

Navigating the Grace Period in Health Insurance: A Comprehensive Guide

What if a lapse in your health insurance coverage could be temporarily bridged, offering a safety net during unexpected circumstances? Understanding the grace period in health insurance is crucial for safeguarding your financial well-being and access to vital medical care.

Editor’s Note: This article on grace periods in health insurance was published today, providing up-to-date information and insights for consumers seeking clarity on this critical aspect of their health coverage.

Why Grace Periods Matter: Protection Against Unforeseen Circumstances

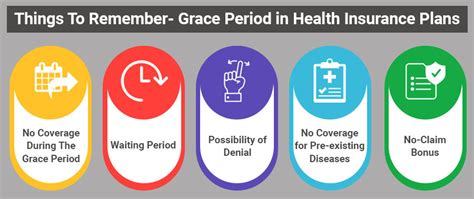

A grace period in health insurance is a short window of time after your premium payment is due, during which your coverage remains active even if payment hasn't been received. This crucial period provides a buffer against accidental or unintentional lapses in coverage, preventing the disruption of essential healthcare access. It's a safety net, particularly important during financial hardships or simple oversight. Understanding its intricacies is vital for protecting your health and finances. The implications of a lapse in coverage, particularly during a medical emergency, can be severe, impacting access to treatment and potentially leading to significant out-of-pocket expenses. The grace period minimizes this risk.

Overview: What This Article Covers

This article delves into the intricacies of health insurance grace periods, exploring their duration, variations across different plans and states, the implications of exceeding the grace period, and strategies to avoid coverage lapses. Readers will gain actionable insights, backed by illustrative examples and real-world scenarios.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon data from the National Association of Insurance Commissioners (NAIC), leading health insurance providers, and legal interpretations of state regulations. The information presented here aims to provide accurate and comprehensive guidance on navigating the complexities of grace periods in health insurance.

Key Takeaways:

- Definition and Core Concepts: A precise definition of a grace period and its fundamental principles.

- Variations Across Plans and States: Exploring the differences in grace period durations depending on the insurer and geographic location.

- Implications of Exceeding the Grace Period: Understanding the consequences of missing the grace period deadline.

- Strategies for Avoiding Coverage Lapses: Practical tips for managing payments and ensuring continuous coverage.

- Special Circumstances and Considerations: Examining exceptions and nuances related to specific situations.

- The Role of the Affordable Care Act (ACA): How the ACA impacts grace periods and continuous coverage.

Smooth Transition to the Core Discussion

Having established the importance of understanding grace periods, let's delve into the specifics, exploring the nuances and potential pitfalls associated with this critical aspect of health insurance.

Exploring the Key Aspects of Grace Periods in Health Insurance

1. Definition and Core Concepts: A grace period is a temporary extension granted by health insurance providers after a premium payment is due. It allows insured individuals to maintain their coverage without interruption even if their payment is slightly delayed. The duration of this period varies depending on the insurer, the type of plan, and, importantly, the state's regulations. It's not an indefinite extension; it’s a limited-time window offering protection against accidental lapses.

2. Variations Across Plans and States: There is no single, universally mandated grace period length. While some plans might offer a 30-day grace period, others may offer only 15 days or even less. State regulations play a significant role in determining the minimum grace period length. Consumers should consult their insurance policy documents or contact their insurer to determine the precise length of their grace period. It’s also critical to check state insurance regulations to understand the minimum standards.

3. Implications of Exceeding the Grace Period: Once the grace period expires and the premium remains unpaid, coverage is typically terminated. This means the insured individual is no longer protected against medical expenses. Any medical services received after the grace period ends will likely be the insured's full responsibility. This can lead to substantial out-of-pocket costs, potentially impacting an individual's financial stability. Reinstating coverage after a lapse may also involve a waiting period, further delaying access to necessary care.

4. Strategies for Avoiding Coverage Lapses: Proactive measures are essential to prevent coverage lapses. These include:

- Setting up automatic payments: Automating premium payments ensures timely submission and eliminates the risk of forgetting due dates.

- Using online bill pay: Online bill pay systems offer convenience and reminders, minimizing the chance of missed payments.

- Setting calendar reminders: Using electronic calendars or reminders can provide timely alerts about upcoming due dates.

- Budgeting for premiums: Incorporating health insurance premiums into a monthly budget ensures funds are available when payments are due.

- Communicating with the insurer: Contacting the insurer immediately if facing financial difficulties can lead to potential payment arrangements or alternative solutions.

5. Special Circumstances and Considerations: Certain situations may influence the application of grace periods. For instance, some insurers may offer extended grace periods in cases of documented hardship, such as unemployment or severe illness. It's important to contact your insurer to discuss individual circumstances and potential options. Individuals experiencing unexpected changes in their financial situation should proactively communicate with their insurer to explore available options.

6. The Role of the Affordable Care Act (ACA): The Affordable Care Act (ACA) plays a role in maintaining continuous coverage. While it doesn't directly dictate the length of grace periods, it emphasizes the importance of maintaining continuous coverage to avoid significant gaps in health insurance. The ACA's open enrollment periods and special enrollment opportunities provide avenues for individuals to obtain or renew coverage, minimizing the risk of prolonged periods without insurance. Understanding how these provisions interact with grace periods is important.

Closing Insights: Summarizing the Core Discussion

Grace periods in health insurance are a vital safety net, providing a temporary buffer against unintentional lapses in coverage. However, their duration varies considerably depending on the insurer, the type of plan, and state regulations. Understanding the intricacies of these periods, taking proactive steps to prevent lapses, and knowing the consequences of exceeding the grace period are crucial for maintaining continuous health insurance coverage and protecting financial well-being.

Exploring the Connection Between Financial Hardship and Grace Periods

Financial hardship is a significant factor influencing the timely payment of health insurance premiums. The connection between financial hardship and grace periods is direct: individuals experiencing financial difficulties are more likely to miss premium payments, potentially leading to coverage lapses during a time when access to healthcare is most crucial.

Key Factors to Consider:

-

Roles and Real-World Examples: Many individuals facing unemployment, medical emergencies, or unexpected financial setbacks may struggle to meet their premium obligations. This can result in missed payments, leading to reliance on the grace period. For example, a person losing their job might rely on the grace period while searching for new employment and securing alternative income.

-

Risks and Mitigations: The risk associated with missed payments is the termination of coverage, leaving the individual vulnerable to significant medical expenses. Mitigation strategies include contacting the insurer to explore payment plans or hardship programs. Many insurers have programs designed to help individuals facing financial difficulty maintain their coverage.

-

Impact and Implications: The impact of exceeding the grace period can be profound, potentially leading to substantial medical debt and negatively affecting credit scores. This can have long-term consequences, making it harder to obtain insurance or other financial products in the future.

Conclusion: Reinforcing the Connection

The interplay between financial hardship and grace periods underscores the vulnerability of individuals facing financial challenges. While grace periods provide a temporary safety net, proactive planning, communication with the insurer, and exploring available assistance programs are essential for mitigating the risk of coverage lapses and protecting access to vital healthcare.

Further Analysis: Examining Payment Plans and Hardship Programs in Greater Detail

Many health insurance providers offer payment plans and hardship programs to assist individuals experiencing financial difficulties. These programs typically involve negotiating a payment schedule that accommodates the individual's financial situation. Hardship programs may offer temporary premium reductions or waivers based on documented financial hardship. Eligibility criteria and the specific terms of these programs vary depending on the insurer and the individual's circumstances. These programs offer crucial support to help prevent coverage lapses during times of financial stress.

FAQ Section: Answering Common Questions About Grace Periods

-

Q: What happens if I miss my premium payment and don't use my grace period?

- A: Your coverage will be terminated, and you will be responsible for all medical expenses incurred after the termination date.

-

Q: How long is a typical grace period?

- A: The length of a grace period varies depending on the insurer, the plan type, and state regulations. It can range from 15 to 30 days.

-

Q: Can I extend my grace period?

- A: It depends on your insurer and your circumstances. Contacting your insurer to explain your situation may lead to options for payment arrangements or hardship programs.

-

Q: What if I'm facing financial hardship?

- A: Contact your insurer immediately to discuss your situation. Many insurers offer payment plans or hardship programs to help individuals experiencing financial difficulties.

-

Q: How can I prevent a lapse in coverage?

- A: Set up automatic payments, utilize online bill pay, set calendar reminders, and budget for your premiums.

-

Q: Is the grace period the same for all types of health insurance plans?

- A: No, the grace period duration may vary among different insurance plans offered by the same provider and different providers altogether. Always check your policy for specific details.

Practical Tips: Maximizing the Benefits of Grace Periods

-

Understand Your Policy: Carefully review your health insurance policy documents to determine the exact length of your grace period and understand the implications of exceeding it.

-

Set Up Automatic Payments: Automate your premium payments to ensure timely submission and prevent accidental lapses in coverage.

-

Utilize Online Bill Pay: Take advantage of online bill pay systems for convenience and reminders.

-

Budget for Premiums: Incorporate health insurance premiums into your monthly budget to ensure sufficient funds are available when payments are due.

-

Communicate with Your Insurer: If you are facing financial difficulties, contact your insurer immediately to discuss potential payment arrangements or hardship programs.

-

Keep Records: Maintain accurate records of all premium payments and communication with your insurer.

Final Conclusion: Wrapping Up with Lasting Insights

Grace periods in health insurance offer a critical safety net, providing temporary protection against unintentional coverage lapses. However, understanding their limitations, taking proactive steps to ensure timely payments, and communicating with your insurer when facing financial challenges are essential for maintaining continuous coverage and protecting your access to vital healthcare. By proactively managing your health insurance, you can safeguard your financial well-being and ensure access to essential medical care when you need it most.

Latest Posts

Latest Posts

-

Can You Pay Electric Bill Late

Apr 04, 2025

-

Late Payment Charges For Electricity Bill

Apr 04, 2025

-

How Much Is The Late Fee For Electricity Bill

Apr 04, 2025

-

What Is The Penalty For Late Payment Of Electricity Bill In Ap

Apr 04, 2025

-

What Is The Penalty For Late Payment Of Electricity Bill In Up

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about Grace Period In Health Insurance . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.