Do You Pay Interest If You Make The Minimum Payment

adminse

Apr 04, 2025 · 7 min read

Table of Contents

Do You Pay Interest If You Make the Minimum Payment? Uncovering the Hidden Costs of Minimum Payments

What if the seemingly simple act of making only the minimum payment on your credit card could significantly impact your financial future? Understanding the mechanics of minimum payments and their impact on interest charges is crucial for responsible credit card management.

Editor’s Note: This article on minimum credit card payments and interest accrual was published today, providing readers with up-to-date information and actionable advice on managing credit card debt effectively.

Why Minimum Payments Matter: The High Cost of Convenience

Many credit card holders find the minimum payment option appealing due to its convenience. It seems manageable, a small amount to pay each month without feeling the pinch. However, this seemingly benign choice can lead to a financial quagmire, significantly increasing the overall cost of your purchases. This article explores the intricate relationship between minimum payments and interest charges, offering readers actionable strategies to avoid the debt trap. Understanding terms like APR (Annual Percentage Rate), interest capitalization, and credit utilization ratio is essential in this context.

Overview: What This Article Covers

This comprehensive guide delves into the complexities of minimum credit card payments. We'll explore the mechanics of interest calculation, the impact of various factors on the total interest paid, strategies for minimizing interest charges, and the long-term financial consequences of relying solely on minimum payments. Readers will gain a practical understanding of responsible credit card management and develop strategies for effective debt reduction.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon data from reputable financial institutions, consumer protection agencies, and academic studies on consumer debt. We’ve analyzed various interest calculation methods employed by different credit card companies and incorporated insights from financial experts to provide accurate and unbiased information.

Key Takeaways:

- Definition of Minimum Payment: A minimum payment is the smallest amount a credit card company allows you to pay each month without incurring late payment fees.

- Interest Accrual on Minimum Payments: Even if you pay the minimum, you still accrue interest on your outstanding balance. This interest is calculated daily on the outstanding principal.

- The Snowball Effect: Making only minimum payments can lead to a snowball effect, where the interest quickly surpasses the principal repayment, significantly extending the repayment period.

- Strategies for Reducing Interest: This includes making payments larger than the minimum, paying off high-interest debt first, and exploring balance transfer options.

- Long-Term Financial Implications: The prolonged repayment period associated with minimum payments can severely impact your credit score and financial well-being.

Smooth Transition to the Core Discussion

Having established the importance of understanding minimum payments, let's delve into the specific mechanisms that govern interest accrual and explore the consequences of consistently making only the minimum payment.

Exploring the Key Aspects of Minimum Payments and Interest

1. Definition and Core Concepts: The minimum payment is calculated as a percentage of your outstanding balance (usually 1-3%), with a minimum dollar amount often specified. This means that even if the percentage calculation results in a very low dollar amount, the credit card company will require at least that minimum dollar amount.

2. Applications Across Industries: The minimum payment calculation methodology is consistent across most major credit card issuers, though the specific percentage and minimum dollar amount can vary. The impact, however, remains uniformly negative if only minimum payments are made.

3. Challenges and Solutions: The primary challenge is the high cost of interest and the prolonged repayment period. Solutions include budgeting for higher payments, debt consolidation, and seeking financial counseling.

4. Impact on Innovation: The financial technology (fintech) industry is developing innovative tools and apps to help consumers manage credit card debt more effectively, including automated payment scheduling and debt tracking tools.

Closing Insights: Summarizing the Core Discussion

The convenience of minimum payments masks a significant financial risk. While seemingly manageable initially, they perpetuate a cycle of debt by allowing interest to compound rapidly. Understanding the mechanics of interest calculation and adopting a proactive approach to debt management are essential for long-term financial health.

Exploring the Connection Between APR and Minimum Payments

The Annual Percentage Rate (APR) is a crucial factor in determining the amount of interest you pay. A higher APR means a higher interest charge for the same outstanding balance. The relationship between APR and minimum payments is directly proportional – the higher the APR, the more significant the interest accumulation even with minimum payments.

Key Factors to Consider:

-

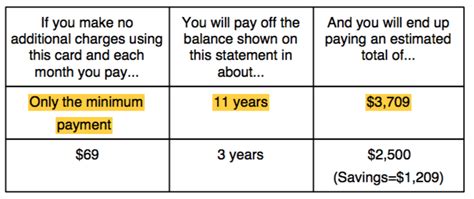

Roles and Real-World Examples: Consider a credit card with a 20% APR and a $1000 balance. If only the minimum payment (e.g., $25) is made, a substantial portion of the payment goes towards interest, leaving only a small amount to reduce the principal. Over time, this minimal principal reduction prolongs the debt.

-

Risks and Mitigations: The primary risk is prolonged debt and significantly increased total interest paid. Mitigation strategies include increasing monthly payments, exploring balance transfers to lower-interest cards, or using debt consolidation loans.

-

Impact and Implications: Consistently making minimum payments can severely damage your credit score, limit your access to future credit, and negatively affect your overall financial well-being.

Conclusion: Reinforcing the Connection

The APR is a critical component in the calculation of interest charges, and its direct relationship with minimum payments necessitates a conscious approach to debt management. By understanding how APR influences interest accrual, consumers can make informed decisions to minimize their overall cost of borrowing.

Further Analysis: Examining Interest Capitalization in Greater Detail

Interest capitalization is a critical aspect of credit card interest calculations. This occurs when unpaid interest is added to the principal balance, thus increasing the amount on which future interest is calculated. This accelerates the growth of debt and dramatically increases the total amount paid.

FAQ Section: Answering Common Questions About Minimum Payments and Interest

-

What is the impact of making only the minimum payment for an extended period? Making only the minimum payment for an extended period significantly increases the total amount of interest paid and prolongs the repayment period, potentially for years or even decades.

-

How does interest capitalization affect my total interest paid? Interest capitalization adds unpaid interest to the principal balance, increasing the amount on which future interest is calculated, resulting in a much higher total interest paid compared to if only the principal was charged interest.

-

Can I avoid paying interest altogether? Yes, you can avoid paying interest by paying your balance in full each month before the due date.

-

What are some strategies for paying off credit card debt faster? Strategies include increasing monthly payments, using the debt snowball or avalanche methods, and exploring balance transfers or debt consolidation options.

-

What is the impact of a high credit utilization ratio on my interest rate? A high credit utilization ratio (the amount of credit you use compared to your credit limit) can negatively affect your credit score and potentially lead to a higher interest rate.

Practical Tips: Maximizing the Benefits of Responsible Credit Card Management

-

Budgeting and Financial Planning: Create a detailed budget to track your income and expenses, identifying areas where you can cut back to allocate more funds towards credit card repayment.

-

Debt Snowball or Avalanche Method: Prioritize high-interest debt first (avalanche) or tackle the smallest debt first to build momentum (snowball). Both strategies can motivate you to keep pushing towards a debt-free life.

-

Negotiating with Credit Card Companies: Contact your credit card company to negotiate a lower interest rate or a payment plan.

-

Balance Transfer Cards: Explore balance transfer cards with introductory 0% APR periods to temporarily reduce or eliminate interest charges. However, be mindful of balance transfer fees and the eventual return to a higher APR.

-

Seek Financial Counseling: If you're struggling to manage your credit card debt, seek professional advice from a certified financial counselor. They can provide personalized guidance and support.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding the mechanics of minimum payments and their impact on interest accrual is paramount for responsible credit card management. While the convenience of minimum payments might seem appealing, the long-term financial implications can be devastating. By adopting proactive strategies, including budgeting, debt management techniques, and potentially seeking professional guidance, consumers can avoid the debt trap and achieve long-term financial well-being. Making more than the minimum payment consistently is the key to breaking free from the high cost of credit card debt.

Latest Posts

Latest Posts

-

How Does Chase Calculate Minimum Payment

Apr 05, 2025

-

Whats The Minimum Payment For Ssi

Apr 05, 2025

-

What Is The Minimum Ssdi Disability Payment

Apr 05, 2025

-

What Is The Minimum Social Security Disability Payment Per Month

Apr 05, 2025

-

What Is The Minimum Payment For Disability

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about Do You Pay Interest If You Make The Minimum Payment . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.