Do Credit Cards Have A Grace Period

adminse

Apr 02, 2025 · 8 min read

Table of Contents

Do credit cards always offer a grace period? Unlocking the secrets to interest-free borrowing.

Understanding the grace period is crucial for managing credit card debt effectively and minimizing interest charges.

Editor’s Note: This article on credit card grace periods was published today, providing readers with the most up-to-date information on this critical aspect of credit card management. We'll explore the intricacies of grace periods, highlighting when they apply and when they don't.

Why Grace Periods Matter: Relevance, Practical Applications, and Financial Significance

A credit card grace period is a crucial component of responsible credit card use. It represents a period where cardholders can avoid paying interest charges on purchases made during the billing cycle. This interest-free period allows individuals to manage their finances more effectively, potentially saving significant amounts of money over time. Understanding how grace periods work is vital for budgeting, debt management, and maximizing the benefits of credit card usage. The impact extends beyond individual finances, influencing consumer spending patterns and overall economic activity.

Overview: What This Article Covers

This article will provide a comprehensive overview of credit card grace periods. It will examine the conditions under which a grace period applies, the factors that can affect its length, common misconceptions surrounding grace periods, and strategies for leveraging this benefit to manage debt effectively. We will also delve into specific scenarios where grace periods may not be available, offering clarity and actionable insights for responsible credit card management.

The Research and Effort Behind the Insights

This article is based on extensive research, incorporating information from leading financial institutions, consumer protection agencies, and legal resources relating to credit card agreements. The analysis presented here aims to provide accurate and unbiased information to empower readers with the knowledge needed to make informed financial decisions. All information is cross-referenced to ensure accuracy and clarity.

Key Takeaways: Summarize the Most Essential Insights

- Definition of Grace Period: A precise definition of a credit card grace period and its core function.

- Conditions for Grace Period: A detailed explanation of the conditions that must be met to qualify for a grace period.

- Factors Affecting Grace Period Length: An examination of elements that can influence the duration of the grace period.

- Situations Where Grace Periods Don't Apply: A discussion of specific scenarios where a grace period is not offered.

- Strategies for Maximizing Grace Periods: Practical tips for leveraging grace periods to manage credit card debt effectively.

- Common Misconceptions: Addressing common misunderstandings about grace periods.

Smooth Transition to the Core Discussion

Having established the importance of understanding credit card grace periods, let's delve into the specifics of how they work, the conditions that govern them, and the potential pitfalls to avoid.

Exploring the Key Aspects of Credit Card Grace Periods

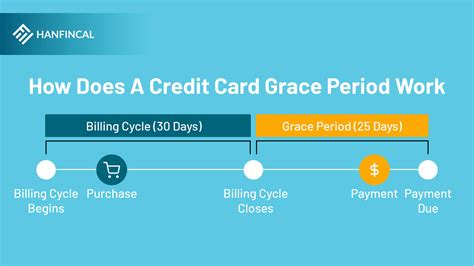

Definition and Core Concepts: A grace period is the time between the end of a billing cycle and the date your payment is due. During this period, if you pay your statement balance in full by the due date, you won't accrue any interest charges on purchases made during the previous billing cycle. This is a significant benefit, offering a period of interest-free financing. The length of the grace period varies depending on the credit card issuer and can range from 21 to 25 days.

Applications Across Industries: The concept of a grace period is primarily associated with credit cards issued by banks and financial institutions. While other types of credit may offer similar interest-free periods, the structure and conditions typically differ significantly. The availability and specifics of a grace period are clearly defined in the terms and conditions of the credit card agreement.

Challenges and Solutions: One of the primary challenges is understanding the conditions that need to be met to qualify for a grace period. Failure to pay the statement balance in full by the due date will eliminate the grace period for that billing cycle, and interest will be charged on the outstanding balance from the date of purchase. A solution is to carefully review credit card statements, setting up automatic payments or reminders to ensure timely payments.

Impact on Innovation: The existence of grace periods has influenced the design of credit card products and the strategies employed by issuers to manage risk and attract customers. Competition amongst credit card companies often involves offering more attractive grace period terms or other benefits to attract and retain customers.

Closing Insights: Summarizing the Core Discussion

Credit card grace periods are a valuable financial tool, but their effectiveness hinges on understanding the conditions for their application and the potential consequences of not meeting those conditions. Careful financial planning and responsible credit card use are essential to maximize this benefit.

Exploring the Connection Between Cash Advances and Grace Periods

Cash advances are a significant factor affecting grace periods. Cash advances are essentially short-term loans obtained from your credit card account. Unlike purchases, cash advances typically do not qualify for a grace period. Interest charges begin accruing from the date you take out the cash advance. This is a crucial distinction to remember when considering using your credit card for short-term borrowing.

Key Factors to Consider:

Roles and Real-World Examples: Consider a scenario where you need emergency funds. A cash advance might seem tempting, but the immediate accrual of interest significantly diminishes its appeal compared to using a personal loan or alternative financial resources. This highlights the importance of understanding the differences between purchases and cash advances and their impact on grace periods.

Risks and Mitigations: The risk associated with cash advances lies in the high interest rates and lack of a grace period. Mitigation strategies include exploring other borrowing options with lower interest rates and focusing on responsible budgeting to avoid the need for cash advances.

Impact and Implications: The widespread use of cash advances without understanding their implications on grace periods can lead to rapid accumulation of debt and increased interest charges. This highlights the need for financial literacy and responsible use of credit products.

Conclusion: Reinforcing the Connection

The connection between cash advances and the absence of a grace period is crucial for responsible credit card management. Avoiding cash advances or carefully considering alternatives can significantly improve your financial health by preventing the rapid accumulation of interest charges.

Further Analysis: Examining Balance Transfers in Relation to Grace Periods

Balance transfers involve moving outstanding balances from one credit card to another. While some balance transfer offers might include a promotional period with a 0% APR, this is not technically the same as a grace period. The promotional period has a fixed duration and requires adherence to specific terms and conditions. It’s vital to distinguish between a promotional 0% APR period and the standard grace period offered on purchases.

FAQ Section: Answering Common Questions About Credit Card Grace Periods

What is a credit card grace period? A grace period is the time you have to pay your credit card balance in full before interest charges start accruing on purchases.

How long is a typical grace period? Grace periods usually range from 21 to 25 days, but this can vary depending on your credit card issuer.

What happens if I don't pay my balance in full by the due date? If you don't pay your statement balance in full by the due date, you will lose your grace period for that billing cycle, and interest will be applied to your outstanding balance.

Do all credit cards have grace periods? Most credit cards offer a grace period, but it’s crucial to check the terms and conditions of your specific card.

Does a grace period apply to cash advances? No, cash advances typically do not have a grace period; interest starts accruing immediately.

Can I still use my grace period if I make only a minimum payment? No, you must pay your statement balance in full to benefit from the grace period. Making only a minimum payment will result in interest being charged on the remaining balance.

What if my statement arrives late, affecting my grace period? Contact your credit card issuer immediately if you have concerns about late statements and their impact on your grace period.

Practical Tips: Maximizing the Benefits of Credit Card Grace Periods

-

Pay your statement balance in full and on time: This is the most crucial step to ensure you benefit from the grace period.

-

Set up automatic payments: This can help prevent missed payments and ensure you always meet the due date.

-

Monitor your spending: Track your credit card spending closely to avoid exceeding your budget and accumulating excessive debt.

-

Review your statement carefully: Check your statement for errors and discrepancies. A quick review can help identify any issues affecting your grace period or balance.

-

Understand your credit card agreement: Familiarize yourself with the terms and conditions of your credit card to fully grasp the specifics of your grace period.

-

Avoid cash advances: Cash advances typically don't come with a grace period, resulting in higher overall costs.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding credit card grace periods is fundamental to responsible credit card use. By carefully managing your spending, making timely payments, and understanding the conditions for grace period application, you can significantly reduce your interest expenses and maximize the value of your credit card. Remembering that cash advances and failure to pay the balance in full will negate this benefit is crucial. This knowledge empowers informed financial decision-making and promotes long-term financial well-being.

Latest Posts

Latest Posts

-

What Is Liquidity Pool

Apr 04, 2025

-

Liquidity Pool Crypto Adalah

Apr 04, 2025

-

What Is Liquidity Pool In Blockchain

Apr 04, 2025

-

What Is A Liquidity Pool In Cryptocurrency

Apr 04, 2025

-

Quickbooks Late Fees

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about Do Credit Cards Have A Grace Period . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.