What Is A Typical Grace Period For A Credit Card

adminse

Apr 02, 2025 · 8 min read

Table of Contents

What's the magic number? Decoding the typical grace period for credit cards.

Understanding your grace period is key to avoiding unnecessary interest charges and maintaining a healthy credit score.

Editor’s Note: This article on credit card grace periods was published today, providing up-to-date information on this crucial aspect of credit card management. This guide is designed to help you navigate the complexities of grace periods and utilize them to your financial advantage.

Why Grace Periods Matter: Relevance, Practical Applications, and Financial Significance

A credit card grace period is a crucial element of responsible credit card usage. It’s the time window between the end of your billing cycle and the due date of your payment, during which you can avoid paying interest on new purchases. Understanding this period is vital for managing debt, minimizing interest charges, and maintaining a positive credit history. Failing to grasp this concept can lead to accumulating unnecessary interest, impacting your credit score and overall financial well-being. The practical applications extend beyond simple interest avoidance; it allows for strategic financial planning and budgeting.

Overview: What This Article Covers

This article provides a comprehensive overview of credit card grace periods. We'll delve into the definition, factors influencing its length, how to calculate your grace period, the implications of missing payments, and how to maximize its benefits. We'll also address common misconceptions and offer actionable tips for effective credit card management.

The Research and Effort Behind the Insights

This article draws upon extensive research from reputable financial sources, including the Consumer Financial Protection Bureau (CFPB), leading credit bureaus, and authoritative financial publications. The information provided is based on a thorough analysis of credit card agreements, industry best practices, and expert opinions, ensuring accuracy and credibility.

Key Takeaways: Summarize the Most Essential Insights

- Definition and Core Concepts: A clear explanation of what constitutes a grace period and its fundamental principles.

- Factors Influencing Length: An examination of the elements that determine the duration of your grace period.

- Calculating Your Grace Period: A step-by-step guide on how to determine your specific grace period.

- Consequences of Missing Payments: Understanding the repercussions of failing to make timely payments.

- Maximizing Grace Period Benefits: Practical strategies for leveraging your grace period effectively.

- Common Misconceptions: Debunking common myths surrounding grace periods.

- Actionable Tips: Concrete steps to manage your credit card and grace period responsibly.

Smooth Transition to the Core Discussion

With a foundational understanding of why grace periods are crucial, let’s delve into the specifics, exploring how they work, the factors affecting their length, and how to best utilize them.

Exploring the Key Aspects of Credit Card Grace Periods

Definition and Core Concepts:

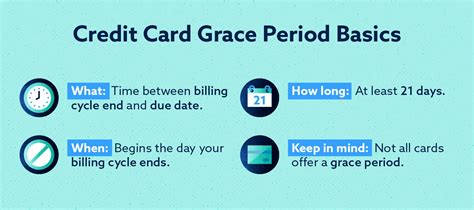

A grace period is the timeframe you have after your credit card billing cycle ends to pay your balance in full without incurring interest charges on new purchases. Crucially, this only applies to new purchases made during the billing cycle. Any existing balance from previous months will continue to accrue interest regardless of whether you pay your current balance in full. The length of the grace period is typically between 21 and 25 days, although this can vary depending on the issuer and the specific card agreement.

Factors Influencing the Length of the Grace Period:

Several factors can influence the length of your grace period:

- Credit Card Issuer: Different credit card companies have different policies regarding grace periods. Some may offer a longer grace period as an incentive, while others may have a shorter period.

- Card Type: The type of credit card (e.g., rewards card, balance transfer card) may impact the grace period offered.

- Individual Agreements: The specifics outlined in your credit card agreement will ultimately dictate the length of your grace period. It's vital to carefully review this document.

- Payment History: Consistently making on-time payments typically won't affect the length of your grace period, but a history of late payments can lead to the loss of your grace period altogether.

- Promotional Offers: Some introductory offers on new credit cards might temporarily extend the grace period. However, this usually reverts to the standard grace period after the promotional period expires.

Calculating Your Grace Period:

To determine your grace period, look for the following information on your credit card statement:

- Statement Closing Date: This is the date the billing cycle ends.

- Payment Due Date: This is the date your payment is due.

Subtract the statement closing date from the payment due date. The result is the length of your grace period. For example, if your statement closing date is August 15th and your payment due date is September 10th, your grace period is approximately 26 days.

Consequences of Missing Payments:

Missing a payment can have several serious consequences:

- Loss of Grace Period: Failure to pay your balance in full by the due date will likely result in the loss of your grace period for the next billing cycle. This means that you’ll start accruing interest on all new purchases.

- Late Payment Fees: Most credit card issuers charge late payment fees. These fees can significantly increase your overall cost.

- Higher Interest Rates: Repeated late payments can lead to an increase in your interest rate, making it more expensive to manage your debt.

- Damaged Credit Score: Late payments are negatively reflected on your credit report, impacting your credit score and potentially making it harder to obtain loans or other forms of credit in the future.

Maximizing Grace Period Benefits:

To maximize the benefits of your grace period:

- Pay in Full and On Time: Always aim to pay your balance in full by the due date to avoid interest charges.

- Track Your Spending: Monitor your spending throughout the billing cycle to ensure you don't exceed your budget.

- Set Payment Reminders: Use online banking features, calendar reminders, or budgeting apps to remind yourself of your payment due date.

- Understand Your Statement: Carefully review your statement each month to ensure accuracy and identify any discrepancies.

- Read Your Credit Card Agreement: Familiarize yourself with the terms and conditions of your credit card agreement, including the specifics regarding your grace period.

Common Misconceptions:

- Myth 1: The grace period applies to all balances. Reality: The grace period only applies to new purchases made during the billing cycle. Existing balances will continue to accrue interest.

- Myth 2: Making a partial payment will preserve the grace period. Reality: To maintain the grace period, the entire balance of new purchases must be paid in full by the due date.

- Myth 3: The grace period is a fixed 30 days. Reality: The grace period varies between 21 and 25 days depending on the issuer and your agreement.

Exploring the Connection Between Payment Timing and Grace Periods

The relationship between the timing of your payments and the grace period is directly proportional. Making timely payments is the key to maximizing the benefits of the grace period. Any delay in payment eliminates the grace period for the subsequent billing cycle, resulting in immediate interest accrual on new purchases.

Key Factors to Consider

Roles and Real-World Examples:

A student using their credit card for textbooks and paying in full before the due date benefits from the grace period, avoiding interest. Conversely, a consumer making numerous purchases and only making a minimum payment loses the grace period and incurs interest charges.

Risks and Mitigations:

The risk lies in assuming a longer grace period than what is offered, leading to unexpected interest charges. Mitigation involves carefully reviewing the credit card agreement, setting payment reminders, and utilizing online banking tools to track spending and payment deadlines.

Impact and Implications:

The impact of understanding and utilizing the grace period can be substantial. Responsible management results in savings on interest payments and contributes to a healthy credit score. Ignoring it leads to debt accumulation and a potential negative impact on creditworthiness.

Conclusion: Reinforcing the Connection

Timely payment is paramount in leveraging the grace period. Understanding the nuances of the grace period empowers consumers to make informed financial decisions.

Further Analysis: Examining Payment Habits in Greater Detail

Analyzing payment habits reveals a clear correlation between timely payments and the successful utilization of the grace period. Consumers who prioritize consistent on-time payments benefit most from this feature, whereas those with inconsistent payment patterns incur unnecessary interest expenses.

FAQ Section: Answering Common Questions About Credit Card Grace Periods

What is a grace period? A grace period is the time you have to pay your credit card balance in full after your billing cycle ends without incurring interest on new purchases.

How long is a typical grace period? The typical grace period is between 21 and 25 days, but it can vary.

What happens if I miss a payment? You will likely lose your grace period for the next cycle, incur late payment fees, and may face interest rate increases.

Does making a partial payment preserve my grace period? No, you must pay the entire balance of new purchases to maintain the grace period.

Where can I find my grace period information? Check your credit card agreement or your monthly statement.

Practical Tips: Maximizing the Benefits of Your Credit Card Grace Period

- Understand Your Statement: Carefully review your credit card statement each month to know your payment due date and the amount you owe.

- Set Up Payment Reminders: Utilize online banking features, calendar alerts, or budgeting apps to set reminders for your payment due date.

- Automate Payments: Consider setting up automatic payments to ensure your payment is always made on time.

- Pay in Full: Always strive to pay your entire balance in full by the due date to avoid interest charges.

- Monitor Your Spending: Track your credit card expenses throughout the billing cycle to avoid overspending.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding and utilizing your credit card grace period is a cornerstone of responsible credit management. By paying attention to your statement, setting payment reminders, and diligently paying your balance in full, you can significantly reduce your interest expenses and maintain a healthy financial standing. The grace period is a valuable tool; make sure you’re using it to your advantage.

Latest Posts

Latest Posts

-

How Much Is The Late Fee For Electricity Bill

Apr 04, 2025

-

What Is The Penalty For Late Payment Of Electricity Bill In Ap

Apr 04, 2025

-

What Is The Penalty For Late Payment Of Electricity Bill In Up

Apr 04, 2025

-

What Is The Penalty For Late Electricity Bill Payment

Apr 04, 2025

-

What Is The Grace Period For Electric Bill

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about What Is A Typical Grace Period For A Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.