Can You Remove A Cosigner From A Private Student Loan

adminse

Apr 04, 2025 · 6 min read

Table of Contents

Can You Remove a Cosigner from a Private Student Loan? Unlocking Financial Freedom

Is it possible to shed the weight of a cosigner on your private student loan, paving the way for independent financial management? Removing a cosigner from a private student loan is a complex but achievable goal, requiring careful planning and strategic execution.

Editor’s Note: This article provides up-to-date information on removing cosigners from private student loans. The information presented here is for guidance only and should not be considered financial advice. Always consult with your lender and a financial advisor before making any decisions regarding your loans.

Why Removing a Cosigner Matters:

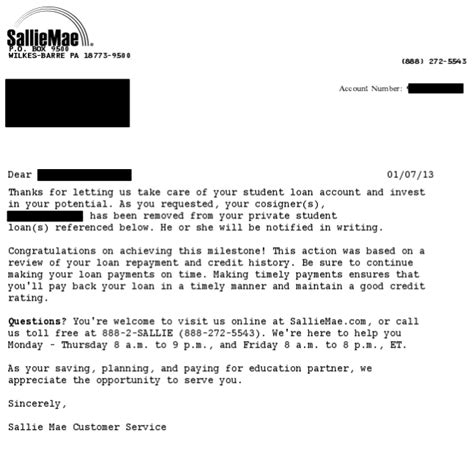

Carrying a cosigner on a private student loan often means relying on another person's creditworthiness for approval and favorable interest rates. While this initial support is invaluable, maintaining a cosigner long-term can limit your financial independence. Removing a cosigner demonstrates improved creditworthiness and allows for sole responsibility over loan repayment, potentially even leading to better loan terms in the future. Furthermore, it frees the cosigner from the liability should you default on your loan payments. This is a significant benefit for both borrower and cosigner.

Overview: What This Article Covers:

This comprehensive guide will explore the process of removing a cosigner from a private student loan, examining the eligibility requirements, steps involved, and potential challenges. We'll also analyze different lender policies, explore alternative strategies, and discuss the importance of maintaining responsible borrowing habits throughout the process. Finally, we'll address frequently asked questions to provide a complete understanding of this crucial financial topic.

The Research and Effort Behind the Insights:

This article is the result of extensive research, drawing upon information from leading financial institutions, reputable consumer advocacy groups, and legal resources specializing in student loan management. The information presented is based on current industry practices and regulations, aiming to provide readers with accurate and reliable guidance.

Key Takeaways:

- Understanding the Cosigner Release Process: The process varies significantly depending on the lender.

- Eligibility Criteria: Meeting certain financial milestones is crucial for cosigner release.

- Documentation and Application: The required documents and application procedure can be complex.

- Alternative Strategies: If immediate release isn't feasible, explore other options.

- Long-Term Financial Planning: Maintaining excellent credit is essential for future loan management.

Smooth Transition to the Core Discussion:

Now that we understand why removing a cosigner is important, let's delve into the specifics of how it's done and the factors that influence the success of this endeavor.

Exploring the Key Aspects of Removing a Cosigner:

1. Definition and Core Concepts:

A cosigner on a private student loan assumes joint responsibility for repayment. Their creditworthiness significantly influences loan approval and interest rates. Removing a cosigner means transferring sole responsibility for repayment to the original borrower. This process isn't automatic and requires meeting specific criteria set by the lender.

2. Applications Across Industries:

Private student loan lenders vary widely in their cosigner release policies. Some may have more stringent requirements than others. There isn't a universal standard, highlighting the importance of individual lender research.

3. Challenges and Solutions:

The primary challenge lies in demonstrating sufficient creditworthiness and repayment history to satisfy the lender's requirements. Building strong credit through responsible credit card usage and consistent on-time loan payments is crucial. Other challenges can include navigating the lender's specific application process and meeting their documentation demands.

4. Impact on Innovation:

The increasing sophistication of credit scoring and loan underwriting technologies may lead to more streamlined cosigner release processes in the future. However, lenders' risk assessments will always play a crucial role in these decisions.

Closing Insights: Summarizing the Core Discussion:

Successfully removing a cosigner requires proactive financial management and a thorough understanding of the lender's requirements. It's a process that demands patience and consistent effort in building a strong credit history.

Exploring the Connection Between Credit Score and Removing a Cosigner:

The relationship between your credit score and the ability to remove a cosigner is paramount. A higher credit score significantly increases your chances of success. A strong credit score demonstrates your ability to manage debt responsibly, reducing the lender's perceived risk.

Key Factors to Consider:

-

Roles and Real-World Examples: A high credit score (ideally above 700) shows a history of responsible borrowing, making lenders more willing to release the cosigner. Case studies show borrowers with excellent credit history and consistent on-time payments successfully removing their cosigners within 1-3 years of loan origination.

-

Risks and Mitigations: A low credit score increases the likelihood of rejection. To mitigate this, focus on improving your credit score before applying. This might involve paying down existing debts, correcting any errors on your credit report, and consistently making on-time payments.

-

Impact and Implications: Successfully removing a cosigner improves your financial independence and demonstrates creditworthiness. It can lead to better loan terms in the future, such as lower interest rates on subsequent loans.

Conclusion: Reinforcing the Connection:

The credit score is the cornerstone for removing a cosigner. Building and maintaining a strong credit profile is not just beneficial for cosigner release but also crucial for long-term financial stability.

Further Analysis: Examining Credit Score Improvement Strategies in Greater Detail:

Improving your credit score requires consistent effort and responsible financial behavior. Strategies include:

- Paying down existing debt: Reduce your credit utilization ratio by paying down credit card balances.

- Making on-time payments: Consistent on-time payments are critical for a positive credit history.

- Monitoring your credit report: Regularly check your credit report for errors and take steps to correct them.

- Using credit responsibly: Avoid applying for too much credit at once.

- Considering a secured credit card: If you have limited credit history, a secured credit card can help build credit.

FAQ Section: Answering Common Questions About Removing a Cosigner:

-

Q: What is the typical timeframe for cosigner release? A: There is no set timeframe. It varies greatly depending on the lender and your creditworthiness. It can range from a few months to several years.

-

Q: What documents are typically required? A: Lenders usually require proof of income, employment history, credit reports, and tax returns. Specific requirements vary by lender.

-

Q: What if my request is denied? A: If your request is denied, review your credit report, address any issues, and reapply after improving your credit score.

-

Q: Can I refinance my loan to remove the cosigner? A: Refinancing is a possibility, but it depends on your creditworthiness and the lender's policies.

Practical Tips: Maximizing the Benefits of Cosigner Removal:

-

Understand the Lender's Requirements: Contact your lender directly to understand their specific requirements for cosigner release.

-

Improve Your Credit Score: Focus on building a strong credit history before applying for cosigner release.

-

Maintain Consistent On-Time Payments: Demonstrate responsible financial behavior through consistent on-time loan payments.

-

Gather Required Documentation: Prepare all necessary documents in advance to streamline the application process.

-

Be Patient and Persistent: The process may take time; don't get discouraged if it's not immediate.

Final Conclusion: Wrapping Up with Lasting Insights:

Removing a cosigner from a private student loan is achievable but requires diligent planning and execution. By understanding the process, building a strong credit history, and following the lender's guidelines, you can achieve financial independence and relieve the burden from your cosigner. Remember, responsible financial behavior is key to long-term success.

Latest Posts

Latest Posts

-

Tjx Rewards Card Worth It

Apr 05, 2025

-

How To Find My Minimum Payment

Apr 05, 2025

-

Minimum Payment On Federal Student Loans

Apr 05, 2025

-

How To Find The Monthly Payment Of A Loan

Apr 05, 2025

-

How To Calculate Minimum Payment On Loan

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about Can You Remove A Cosigner From A Private Student Loan . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.