How To Calculate Minimum Payment On Loan

adminse

Apr 05, 2025 · 8 min read

Table of Contents

Decoding the Minimum Loan Payment: A Comprehensive Guide

What if understanding your minimum loan payment unlocks significant long-term savings and financial peace of mind? Mastering this calculation is crucial for responsible debt management and achieving your financial goals.

Editor's Note: This article on calculating minimum loan payments was published today, providing you with the most up-to-date information and strategies for effectively managing your debt.

Why Understanding Minimum Loan Payments Matters:

Understanding your minimum loan payment is far more than simply knowing how much to pay each month. It’s a cornerstone of responsible financial management. It directly impacts your interest costs, loan repayment duration, and overall financial health. Failing to understand this calculation can lead to missed payments, penalties, damage to your credit score, and significantly increased debt burden. This knowledge empowers you to make informed decisions about your borrowing, budgeting, and long-term financial planning. The ability to accurately calculate and understand your minimum payments applies to various loan types, including mortgages, auto loans, personal loans, student loans, and credit card debt.

Overview: What This Article Covers:

This article provides a comprehensive guide to calculating minimum loan payments. We will explore different calculation methods, delve into the factors influencing these payments, analyze the implications of paying only the minimum versus making larger payments, and address frequently asked questions. You'll gain actionable insights and practical strategies for effective debt management.

The Research and Effort Behind the Insights:

This article draws upon established financial formulas, real-world examples, and widely accepted debt management principles. The information presented is based on commonly used calculation methods and aims to provide readers with a clear and accurate understanding of the topic.

Key Takeaways:

- Definition and Core Concepts: A clear explanation of minimum payment and its components.

- Calculation Methods: Step-by-step guides for calculating minimum payments using various formulas.

- Factors Influencing Minimum Payments: Understanding interest rates, loan terms, and principal amounts.

- Paying More Than the Minimum: The benefits and strategies for accelerating loan repayment.

- Consequences of Only Paying the Minimum: Long-term financial implications and potential pitfalls.

Smooth Transition to the Core Discussion:

Now that we've established the importance of understanding minimum loan payments, let's delve into the practical aspects of calculating them and the factors that influence their amount.

Exploring the Key Aspects of Minimum Loan Payment Calculation:

1. Definition and Core Concepts:

The minimum payment on a loan is the smallest amount you are required to pay each month to remain in good standing with your lender. Failing to meet this minimum payment can result in late fees, penalties, and a negative impact on your credit score. This minimum payment typically covers a portion of the principal (the original loan amount) and the accrued interest. The exact proportion varies depending on the loan type and terms.

2. Calculation Methods:

There isn't a single, universal formula for calculating minimum payments across all loan types. The method used depends on the loan agreement. However, two common approaches are used:

-

Simple Interest Calculation: This method is less common for longer-term loans like mortgages but is frequently used for short-term loans or credit cards. It involves calculating the interest accrued on the outstanding principal balance for a given period and adding it to a predetermined portion of the principal. The formula is simpler:

Minimum Payment = (Outstanding Principal Balance * (Interest Rate / 12)) + (Principal Payment)Where:

Outstanding Principal Balanceis the amount still owed on the loan.Interest Rateis the annual interest rate (expressed as a decimal).Principal Paymentis a fixed or percentage-based amount of the principal to be repaid each month. This often represents a small fraction of the principal.

-

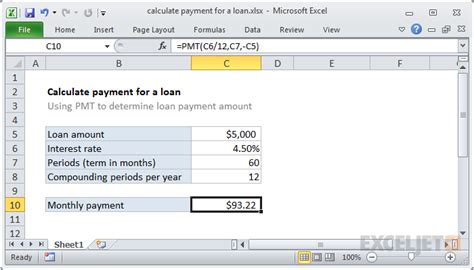

Amortization Schedule: This is the most common method for long-term loans such as mortgages and auto loans. An amortization schedule calculates equal monthly payments that cover both interest and principal over the loan's life. The formula is more complex and usually requires a financial calculator or spreadsheet software:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1]Where:

Mis the monthly payment.Pis the principal loan amount.iis the monthly interest rate (annual interest rate divided by 12).nis the total number of payments (loan term in months).

This formula is best used with a financial calculator or spreadsheet program due to its complexity. Many online loan calculators are available to simplify this calculation.

3. Factors Influencing Minimum Payments:

Several factors determine the minimum payment amount:

- Interest Rate: A higher interest rate results in a larger minimum payment, as a greater portion of the payment goes towards interest.

- Loan Term (Length): A longer loan term generally means smaller monthly payments, but you'll pay significantly more interest over the life of the loan.

- Principal Loan Amount: A larger loan amount naturally results in a higher minimum payment.

- Loan Type: Different loan types might have varying minimum payment calculation methods and requirements. Credit card minimum payments, for instance, are often a percentage of the outstanding balance (e.g., 2% or a minimum dollar amount, whichever is greater).

4. Paying More Than the Minimum:

Paying more than the minimum payment each month offers substantial benefits:

- Reduced Interest Payments: A larger payment reduces the principal faster, leading to lower interest charges over the life of the loan.

- Shorter Repayment Period: Paying extra reduces the loan's overall repayment time, saving you money on interest.

- Improved Financial Health: Faster debt repayment improves your credit score and frees up cash flow sooner.

5. Consequences of Only Paying the Minimum:

While convenient, only paying the minimum payment carries significant risks:

- Higher Total Interest Paid: You'll pay far more in interest over the loan's life.

- Prolonged Debt Burden: It takes significantly longer to pay off the loan, extending the debt's impact on your finances.

- Increased Vulnerability to Financial Hardship: Unexpected expenses or income changes can easily overwhelm you when burdened with long-term debt.

- Negative Impact on Credit Score: While consistently paying the minimum avoids late payment penalties, it doesn't necessarily reflect positive creditworthiness. A higher debt-to-credit ratio can harm your score.

Exploring the Connection Between Interest Rates and Minimum Loan Payments:

The relationship between interest rates and minimum loan payments is directly proportional. A higher interest rate means a larger portion of your monthly payment goes toward interest, leaving less to reduce the principal. This results in a higher minimum payment and a longer repayment period. Conversely, a lower interest rate allows for a smaller minimum payment and faster debt repayment.

Key Factors to Consider:

-

Roles and Real-World Examples: Consider a $20,000 auto loan. A 5% interest rate over 60 months will have a lower minimum payment than a 10% interest rate over the same period. The higher interest rate necessitates a larger minimum payment to cover the increased interest charges.

-

Risks and Mitigations: The risk of paying only the minimum is prolonged debt and high interest costs. Mitigation strategies include budgeting for larger payments, exploring debt consolidation options, or refinancing to lower the interest rate.

-

Impact and Implications: The long-term impact of only paying the minimum is significant, potentially adding thousands of dollars to your total interest paid and delaying your financial freedom.

Conclusion: Reinforcing the Connection:

The connection between interest rates and minimum loan payments is critical. Understanding this relationship enables you to make informed decisions about borrowing and repayment strategies. By considering different interest rates and loan terms, you can effectively manage your debt and minimize long-term costs.

Further Analysis: Examining Interest Rate Fluctuations in Greater Detail:

Interest rates are dynamic; they fluctuate based on various economic factors. Understanding these fluctuations is crucial for effective financial planning. Borrowers should be aware that changes in interest rates can influence their minimum payments. Refinancing a loan when interest rates decline can significantly lower your monthly payment and reduce the overall cost of borrowing.

FAQ Section: Answering Common Questions About Minimum Loan Payments:

-

Q: What happens if I miss a minimum payment?

- A: Missing a minimum payment can result in late fees, damage to your credit score, and potential collection actions by the lender.

-

Q: Can I negotiate my minimum payment with the lender?

- A: In some cases, you might be able to negotiate a modified payment plan, but this depends on your lender's policies and your financial circumstances.

-

Q: How can I calculate my minimum payment if my loan statement doesn't show the calculation?

- A: You can use online loan calculators, providing the loan amount, interest rate, and loan term to determine the minimum payment.

-

Q: Is it always best to pay more than the minimum?

- A: While paying more than the minimum is generally beneficial, you should always ensure you have sufficient funds for other essential expenses. Overextending yourself financially can have negative consequences.

Practical Tips: Maximizing the Benefits of Understanding Minimum Payments:

- Understand the Basics: Learn how minimum payments are calculated for your specific loan type.

- Analyze Your Loan Statement: Carefully review your statements to understand the breakdown of your payments (principal vs. interest).

- Budget Strategically: Create a realistic budget that allows you to pay more than the minimum payment whenever possible.

- Explore Debt Consolidation Options: Consolidating high-interest debts into a single loan with a lower interest rate can reduce your overall minimum payment and accelerate debt repayment.

- Consider Refinancing: If interest rates fall, consider refinancing your loan to secure a lower interest rate and a potentially lower minimum payment.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding how to calculate your minimum loan payment is a fundamental skill for responsible financial management. By grasping the factors that influence these payments and actively managing your debt, you can save money, improve your credit score, and achieve your financial goals faster. Don't just pay the minimum; strive for more, and secure your long-term financial well-being.

Latest Posts

Latest Posts

-

How To Calculate Amex Payment

Apr 05, 2025

-

How Does Amex Calculate Minimum Payment Due

Apr 05, 2025

-

How Is American Express Minimum Payment Calculated

Apr 05, 2025

-

How Does American Express Calculate Minimum Payment

Apr 05, 2025

-

What Is The Minimum Repayment On Barclaycard

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about How To Calculate Minimum Payment On Loan . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.