Minimum Payment On Federal Student Loans

adminse

Apr 05, 2025 · 8 min read

Table of Contents

Decoding the Minimum Payment on Federal Student Loans: A Comprehensive Guide

What if navigating your federal student loan payments felt less daunting and more manageable? Understanding the nuances of minimum payments is key to responsible repayment and achieving long-term financial health.

Editor’s Note: This article on minimum payments for federal student loans was published [Date]. This comprehensive guide provides up-to-date information to help borrowers understand their repayment options and make informed decisions.

Why Minimum Payments on Federal Student Loans Matter:

Federal student loans represent a significant financial commitment for millions. Understanding your minimum payment isn't just about meeting the basic requirement; it's crucial for avoiding delinquency, preserving your credit score, and potentially saving money in the long run. Knowing your options, including the impact on interest accrual and total repayment cost, empowers borrowers to make strategic choices aligned with their financial goals. This knowledge becomes particularly important when considering different repayment plans, which drastically alter the minimum payment amount.

Overview: What This Article Covers:

This article provides a detailed exploration of minimum payments on federal student loans. We will examine different repayment plans, the factors influencing minimum payment calculations, the consequences of only making minimum payments, strategies for managing payments, and resources available to borrowers facing financial hardship. Readers will gain a comprehensive understanding of this critical aspect of student loan repayment.

The Research and Effort Behind the Insights:

This article is based on extensive research of official government websites, including the Federal Student Aid website (studentaid.gov), reputable financial publications, and analysis of relevant legislation. The information provided is intended to be accurate and up-to-date, but it is always advisable to verify details directly with your loan servicer.

Key Takeaways:

- Definition of Minimum Payment: A clear explanation of what constitutes the minimum payment and how it's calculated.

- Repayment Plan Variations: A detailed breakdown of the various federal student loan repayment plans and how they affect minimum payments.

- Interest Accrual and Capitalization: How interest impacts the total repayment cost and the implications of only paying the minimum.

- Strategies for Effective Repayment: Practical tips and strategies for managing payments efficiently.

- Resources for Borrowers in Hardship: Information about available options for those struggling to make payments.

Smooth Transition to the Core Discussion:

With a foundational understanding of the importance of minimum payments, let's delve into the specifics, examining the various factors that influence their calculation and the implications of different repayment strategies.

Exploring the Key Aspects of Minimum Payments on Federal Student Loans:

1. Definition and Core Concepts:

The minimum payment on a federal student loan is the smallest amount you are required to pay each month to remain in good standing. This amount is not fixed and varies depending on several factors, most notably the type of loan and the repayment plan chosen. Failing to make at least the minimum payment can lead to delinquency, negatively impacting your credit score and potentially resulting in collection actions.

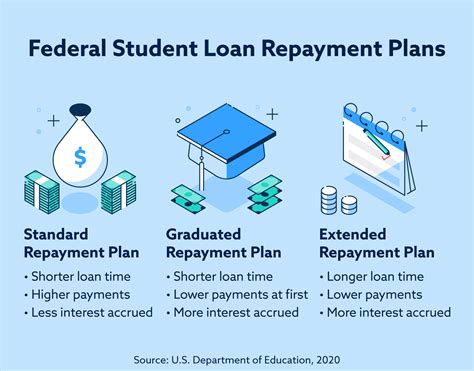

2. Repayment Plan Variations:

The federal government offers several repayment plans designed to cater to different financial situations. Each plan calculates the minimum payment differently, significantly impacting the total repayment cost and the monthly burden. The most common plans include:

-

Standard Repayment Plan: This plan typically involves fixed monthly payments over a 10-year period. The minimum payment is calculated based on the total loan amount and the interest rate.

-

Graduated Repayment Plan: Payments begin low and gradually increase over time, usually over a 10-year period. This can initially provide some relief but results in higher payments later in the repayment term.

-

Extended Repayment Plan: This plan extends the repayment period to up to 25 years, resulting in lower monthly payments but significantly higher total interest paid.

-

Income-Driven Repayment (IDR) Plans: These plans (Income-Based Repayment, Pay As You Earn, Revised Pay As You Earn, and Income-Driven Repayment) base your monthly payment on your income and family size. The minimum payment is recalculated annually based on your reported income. These plans often lead to loan forgiveness after 20 or 25 years, but this forgiveness is considered taxable income.

-

Income Contingent Repayment Plan: This plan was phased out but some borrowers are still on it. It’s similar to other IDR plans, basing the minimum payment on income and family size.

3. Interest Accrual and Capitalization:

Interest accrues on federal student loans even while you're making payments. If you only pay the minimum, a significant portion of your payment goes towards interest, leaving less to reduce the principal balance. This means it can take much longer to pay off your loans and results in a substantially higher overall cost. Capitalization, where unpaid interest is added to the principal balance, exacerbates this issue.

4. Impact on Credit Score:

Making consistent minimum payments is crucial for maintaining a healthy credit score. Missed or late payments severely damage your creditworthiness, making it difficult to secure loans, credit cards, or even rent an apartment in the future. A strong credit score is essential for accessing favorable financial opportunities.

Exploring the Connection Between Financial Literacy and Minimum Payments:

The relationship between financial literacy and understanding minimum student loan payments is paramount. A lack of financial literacy can lead borrowers to underestimate the long-term consequences of only making minimum payments. This can result in prolonged debt, increased interest charges, and a negative impact on credit scores. Conversely, strong financial literacy equips borrowers with the knowledge to choose the optimal repayment plan, make informed payment decisions, and proactively manage their debt.

Key Factors to Consider:

-

Roles and Real-World Examples: Many borrowers, especially those unfamiliar with student loan repayment, mistakenly believe that consistently making minimum payments is a sufficient repayment strategy. This often leads to unexpectedly high interest charges and extended repayment periods. For instance, a borrower with $30,000 in loans on a standard plan might pay significantly more over the long term than one who makes larger, consistent payments.

-

Risks and Mitigations: The primary risk associated with only making minimum payments is increased total repayment cost due to accumulating interest. Mitigation strategies include actively exploring different repayment plans, budgeting for higher payments, and actively pursuing avenues for additional income to reduce the burden.

-

Impact and Implications: The long-term implications of solely making minimum payments can severely limit financial flexibility. It might delay major life goals like homeownership, starting a family, or investing. Furthermore, it can increase stress and anxiety associated with persistent debt.

Conclusion: Reinforcing the Connection:

The connection between financial literacy and responsible student loan repayment cannot be overstated. By understanding the intricacies of minimum payments and their long-term implications, borrowers can make strategic decisions that promote financial well-being and contribute to a brighter financial future.

Further Analysis: Examining Financial Literacy Programs in Greater Detail:

Many organizations and government agencies offer resources to improve financial literacy. These programs often include educational materials, workshops, and online tools to help individuals understand budgeting, debt management, and long-term financial planning. Access to these resources is crucial for helping borrowers navigate the complexities of federal student loan repayment.

FAQ Section: Answering Common Questions About Minimum Payments on Federal Student Loans:

-

What happens if I miss a minimum payment? Missing a payment will lead to delinquency, negatively impacting your credit score. Your loan servicer will contact you, and additional fees may be applied.

-

Can I change my repayment plan? Yes, you can typically change your repayment plan once a year. Contact your loan servicer to explore your options.

-

How do I calculate my minimum payment? The calculation varies by repayment plan. You can use the loan servicer's website or contact them directly for assistance.

-

What if I can't afford my minimum payment? Contact your loan servicer immediately to discuss options like deferment, forbearance, or an income-driven repayment plan.

-

What is loan forgiveness? Some income-driven repayment plans offer loan forgiveness after a certain period (20 or 25 years), but the forgiven amount is considered taxable income.

Practical Tips: Maximizing the Benefits of Strategic Repayment:

-

Understand Your Loans: Consolidate your loans if you have multiple ones to simplify repayment. Understand the interest rates, repayment terms, and total amounts owed for each loan.

-

Choose the Right Repayment Plan: Carefully compare different repayment plans, considering your current financial situation and long-term goals.

-

Budget Strategically: Create a detailed budget that includes your minimum student loan payment and other essential expenses.

-

Explore Additional Income Streams: Consider part-time jobs or freelancing to supplement your income and accelerate loan repayment.

-

Automate Payments: Set up automatic payments to ensure timely payments and avoid late fees.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding minimum payments on federal student loans is a cornerstone of responsible debt management. By actively engaging with repayment options, utilizing available resources, and prioritizing financial literacy, borrowers can significantly improve their long-term financial well-being. Remember, strategic planning and consistent effort are key to successful repayment and achieving financial freedom.

Latest Posts

Latest Posts

-

What Does The Minimum Payment Amount On A Credit Card Statement Indicate

Apr 05, 2025

-

Whats The Minimum Payment For A Credit Card

Apr 05, 2025

-

What Would Be The Minimum Payment On A Credit Card

Apr 05, 2025

-

What Would Be My Minimum Payment On A Credit Card

Apr 05, 2025

-

What Will Be My Minimum Payment On Credit Card

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about Minimum Payment On Federal Student Loans . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.