What's A Signature Loan

adminse

Mar 31, 2025 · 8 min read

Table of Contents

Unlocking the Mystery: A Deep Dive into Signature Loans

What if securing funds for your needs didn't require mountains of paperwork and collateral? Signature loans, often called unsecured personal loans, offer a streamlined approach to borrowing, providing financial flexibility without the burden of securing assets.

Editor’s Note: This article on signature loans was published today, providing readers with up-to-date information and insights into this increasingly popular financing option.

Why Signature Loans Matter: Flexibility, Accessibility, and Financial Freedom

Signature loans are gaining popularity because they offer a simpler, faster alternative to secured loans. Unlike mortgages or auto loans that require collateral (your house or car), signature loans are based solely on your creditworthiness and your promise to repay. This accessibility makes them a valuable tool for various financial needs, from debt consolidation and home improvements to medical expenses and unexpected emergencies. Their significance lies in their ability to provide financial flexibility when other options might be unavailable or impractical. Understanding the nuances of signature loans is crucial for navigating personal finance effectively. The industry is seeing increased competition and innovation, leading to more favorable terms for borrowers.

Overview: What This Article Covers

This article provides a comprehensive overview of signature loans, exploring their core features, eligibility criteria, application process, advantages and disadvantages, and potential risks. We'll examine how interest rates are determined, compare them to other loan types, and offer practical tips for securing the best possible terms. Finally, we'll address frequently asked questions and provide actionable advice to help readers make informed decisions.

The Research and Effort Behind the Insights

This article is the product of extensive research, incorporating information from reputable financial institutions, consumer advocacy groups, and legal resources. Data on interest rates, loan terms, and application processes has been sourced from multiple providers to offer a comprehensive and unbiased perspective. The analysis aims to provide readers with accurate, reliable, and actionable information to navigate the world of signature loans effectively.

Key Takeaways:

- Definition and Core Concepts: A clear understanding of what constitutes a signature loan and its fundamental principles.

- Eligibility Criteria: The factors lenders consider when assessing loan applications.

- Application Process: A step-by-step guide to applying for a signature loan.

- Interest Rates and Fees: How interest rates are calculated and what other fees might apply.

- Advantages and Disadvantages: Weighing the pros and cons of signature loans compared to other options.

- Risks and Mitigation Strategies: Understanding potential risks and how to minimize them.

- Practical Tips: Actionable advice for securing favorable loan terms and responsible borrowing.

Smooth Transition to the Core Discussion:

Now that we understand the importance of signature loans, let's delve into the specifics, beginning with a clear definition and exploring the factors that influence their accessibility and cost.

Exploring the Key Aspects of Signature Loans

1. Definition and Core Concepts:

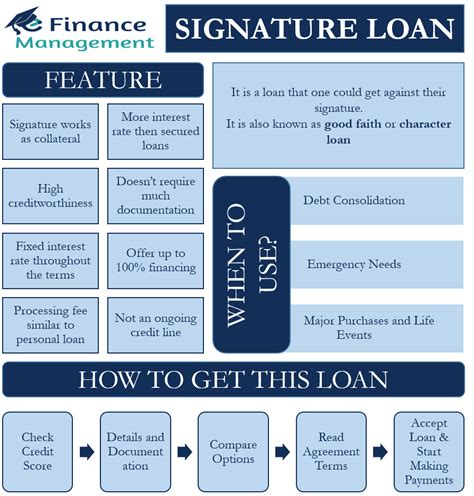

A signature loan, also known as an unsecured personal loan, is a type of loan that doesn't require collateral. The lender approves the loan based on the borrower's credit history, income, and debt-to-income ratio. The borrower "signs" for the loan, signifying their commitment to repay the principal and interest as agreed upon in the loan agreement. The repayment schedule is typically structured in fixed monthly installments over a predetermined period.

2. Eligibility Criteria:

Lenders use various criteria to assess a borrower's eligibility for a signature loan. These typically include:

- Credit Score: A high credit score demonstrates a history of responsible borrowing and repayment, making it easier to qualify for a loan with favorable terms.

- Income: Lenders want assurance that you have the financial capacity to repay the loan. They will review your income statements and bank records.

- Debt-to-Income Ratio (DTI): This ratio represents your monthly debt payments compared to your gross monthly income. A lower DTI indicates a greater capacity to handle additional debt.

- Employment History: A stable employment history demonstrates financial stability and reliability.

- Length of Residence: Lenders often assess how long you've lived at your current address.

3. Application Process:

The application process typically involves:

- Online Application: Many lenders offer online applications, simplifying the process.

- Credit Check: The lender will perform a credit check to assess your creditworthiness.

- Income Verification: You'll need to provide documentation to verify your income.

- Loan Approval: Upon approval, you'll receive a loan offer outlining the terms and conditions.

- Loan Disbursement: Once you accept the offer, the funds will be disbursed to your account.

4. Interest Rates and Fees:

Signature loan interest rates vary depending on several factors, including:

- Credit Score: A higher credit score generally qualifies you for a lower interest rate.

- Loan Amount: Larger loan amounts may carry higher interest rates.

- Loan Term: Longer loan terms typically result in higher overall interest costs.

- Lender: Different lenders have varying lending practices and interest rate structures.

In addition to interest, you may incur fees such as origination fees, late payment fees, and prepayment penalties. It's crucial to carefully review all fees before accepting a loan offer.

5. Advantages and Disadvantages:

Advantages:

- No Collateral Required: This is the primary advantage. You don't risk losing assets if you fail to repay the loan.

- Faster Approval Process: The application process is often quicker than secured loans.

- Flexibility: Signature loans can be used for various purposes.

- Improved Credit Score: Responsible repayment can boost your credit score.

Disadvantages:

- Higher Interest Rates: Unsecured loans typically have higher interest rates than secured loans due to the increased risk for the lender.

- Stricter Eligibility Criteria: Borrowers with poor credit scores may find it difficult to qualify.

- Limited Loan Amounts: The loan amounts available are often smaller compared to secured loans.

6. Risks and Mitigation Strategies:

The primary risk is defaulting on the loan, which can negatively impact your credit score and potentially lead to debt collection actions. To mitigate these risks:

- Borrow Responsibly: Only borrow what you can comfortably afford to repay.

- Shop Around: Compare interest rates and fees from multiple lenders to secure the best terms.

- Budget Carefully: Create a realistic budget to ensure you can make your monthly payments.

- Establish an Emergency Fund: Having savings can help you manage unexpected expenses and avoid relying solely on loans.

Exploring the Connection Between Credit Score and Signature Loans

The relationship between your credit score and your ability to secure a signature loan is paramount. A higher credit score significantly improves your chances of approval and secures more favorable terms, including lower interest rates.

Key Factors to Consider:

- Roles and Real-World Examples: A borrower with a 750 credit score will likely receive a lower interest rate and a higher loan amount than a borrower with a 600 score. This is because lenders perceive the higher-scoring borrower as less risky.

- Risks and Mitigations: A low credit score significantly increases the risk of loan rejection or higher interest rates. To mitigate this, borrowers can work on improving their credit scores before applying for a loan.

- Impact and Implications: Your credit score acts as a predictor of your repayment ability, directly impacting the terms and conditions of your signature loan.

Conclusion: Reinforcing the Connection

The interplay between credit score and signature loan approval highlights the importance of responsible credit management. By maintaining a good credit history, borrowers can access favorable lending options and secure their financial well-being.

Further Analysis: Examining Credit Repair in Greater Detail

Improving your credit score can substantially improve your chances of securing a signature loan with attractive terms. Strategies include paying bills on time, reducing debt, and monitoring your credit report for errors. Credit counseling services can also provide guidance and support.

FAQ Section: Answering Common Questions About Signature Loans

What is a signature loan? A signature loan is an unsecured personal loan that doesn't require collateral. The lender bases the approval on your creditworthiness and your promise to repay.

How is a signature loan different from a secured loan? A secured loan requires collateral, such as a house or car, to secure the loan. A signature loan is unsecured, meaning no collateral is needed.

What factors affect the interest rate on a signature loan? Credit score, loan amount, loan term, and lender policies all influence the interest rate.

Can I use a signature loan for any purpose? While there aren't usually restrictions on how you use the funds, lenders might ask about the intended use during the application process.

What happens if I default on a signature loan? Defaulting can severely damage your credit score and may lead to debt collection actions.

How can I improve my chances of approval for a signature loan? Maintaining a good credit score, having a stable income, and demonstrating a low debt-to-income ratio are key factors.

Practical Tips: Maximizing the Benefits of Signature Loans

- Check your credit report: Before applying, review your credit report for any errors.

- Compare lenders: Shop around and compare offers from different lenders.

- Understand the terms: Carefully review the loan agreement before signing.

- Create a repayment plan: Develop a budget to ensure you can make your monthly payments.

- Pay on time: Consistent on-time payments will protect your credit score.

Final Conclusion: Wrapping Up with Lasting Insights

Signature loans offer a valuable financial tool for various needs, providing a flexible and accessible way to borrow money. However, responsible borrowing is essential to avoid the risks associated with unsecured debt. By understanding the factors that influence loan approval, interest rates, and repayment, borrowers can make informed decisions and leverage the benefits of signature loans while safeguarding their financial well-being. Remember, proactive credit management is key to unlocking the full potential of this financing option.

Latest Posts

Latest Posts

-

Richmond Manufacturing Index Definition

Apr 28, 2025

-

The Goal Of Tax Planning Is To Minimize Taxes Explain Why This Statement Is Not True

Apr 28, 2025

-

Why Is Income Shifting Considered Such A Major Tax Planning Concept

Apr 28, 2025

-

Explain How Tax Compliance Differs From Tax Planning

Apr 28, 2025

-

Rich Valuation Definition

Apr 28, 2025

Related Post

Thank you for visiting our website which covers about What's A Signature Loan . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.