What Does Balance Transfer Mean On A Credit Card

adminse

Mar 31, 2025 · 8 min read

Table of Contents

What's the secret to conquering credit card debt without breaking the bank?

Balance transfers offer a powerful strategy for managing high-interest credit card debt, potentially saving you thousands in interest charges.

Editor’s Note: This article on balance transfers provides a comprehensive guide to understanding how balance transfers work, their advantages and disadvantages, and how to choose the right balance transfer offer. We’ve updated this information to reflect current industry practices and offer the most current advice available.

Why Balance Transfers Matter:

High-interest credit card debt can feel overwhelming. Minimum payments often barely touch the principal, leaving you trapped in a cycle of accumulating interest. Balance transfers offer a potential solution by allowing you to move your existing credit card debt to a new card with a lower interest rate, typically a 0% introductory APR (Annual Percentage Rate). This can provide crucial breathing room to pay down the principal balance faster, significantly reducing the overall cost of borrowing. Understanding balance transfers is crucial for anyone looking to strategically manage their credit card debt and improve their financial well-being.

Overview: What This Article Covers:

This article delves into the intricacies of balance transfers, covering their definition, mechanics, eligibility requirements, potential benefits and drawbacks, and strategies for maximizing their effectiveness. We’ll examine different types of balance transfer offers, how to choose the best one, and important considerations to avoid pitfalls. Furthermore, we'll discuss the relationship between balance transfers and credit scores, and how to use them responsibly to avoid further financial strain.

The Research and Effort Behind the Insights:

This article is the result of extensive research, drawing on information from reputable financial websites, consumer advocacy groups, credit card company disclosures, and relevant legal documentation. The information provided is intended to be factual and informative, helping readers make informed decisions about using balance transfers.

Key Takeaways:

- Definition and Core Concepts: A clear explanation of what a balance transfer is and how it works.

- Practical Applications: Real-world scenarios demonstrating the benefits of balance transfers in different financial situations.

- Challenges and Solutions: Potential drawbacks of balance transfers and strategies for mitigating risks.

- Future Implications: How the landscape of balance transfer offers might evolve and how consumers can adapt.

Smooth Transition to the Core Discussion:

With an understanding of the importance of balance transfers in debt management, let’s explore the key aspects of this financial tool.

Exploring the Key Aspects of Balance Transfers:

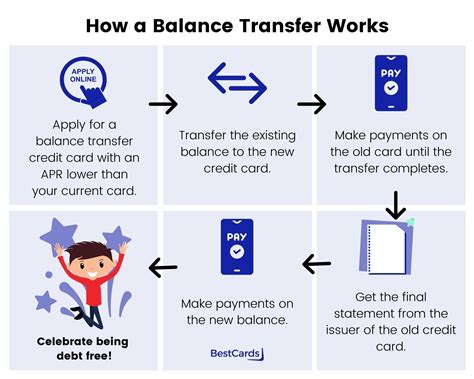

Definition and Core Concepts:

A balance transfer is the process of moving an outstanding balance from one credit card to another. This typically involves applying for a new credit card with a balance transfer offer, then transferring the existing debt from your old card to the new one. Many balance transfer offers include a promotional period with a 0% APR, meaning you won't accrue interest during that timeframe. However, this introductory period is temporary and usually lasts for a specific period (e.g., 12, 18, or 24 months), after which the standard APR of the new card will apply.

Applications Across Industries:

Balance transfers aren't restricted to a specific industry. They are a personal finance tool utilized by individuals across various income levels and professions. The applications vary depending on the individual's financial circumstances, but the core goal remains consistent – to reduce the cost of paying off existing high-interest debt.

Challenges and Solutions:

One major challenge is the balance transfer fee. Many cards charge a percentage of the transferred amount (typically 3-5%) as a fee. This fee adds to the overall cost, so it's crucial to weigh the savings from lower interest against the transfer fee. Another challenge is the potential impact on your credit score. Applying for a new credit card can temporarily lower your score, and failing to manage the transferred balance responsibly can severely damage it. Solutions involve careful planning, comparing offers meticulously, and maintaining excellent credit card management practices after the transfer.

Impact on Innovation:

The evolution of balance transfer offers reflects innovation within the credit card industry. The increasing competition among card issuers has led to more attractive offers, longer 0% APR periods, and more flexible terms. However, consumers need to remain vigilant and compare offers critically.

Exploring the Connection Between Balance Transfer Fees and Effective Debt Management:

The balance transfer fee is a significant factor affecting the overall cost-effectiveness of a balance transfer. While a lower APR can save substantial interest, a high transfer fee can offset these savings. It's vital to calculate the total cost, including the fee, to determine if a balance transfer is truly beneficial.

Key Factors to Consider:

Roles and Real-World Examples:

Let's say you have $10,000 in credit card debt with a 20% APR. A balance transfer to a card with a 0% APR for 18 months, charging a 3% transfer fee, would cost you $300 upfront. However, over those 18 months, you'd save thousands in interest that would have accrued at the 20% rate. This makes the balance transfer financially advantageous, despite the fee. Another example: someone with multiple high-interest cards could consolidate their debt into a single balance transfer card for easier management.

Risks and Mitigations:

A major risk is missing the 0% APR deadline. Failing to pay off the balance before the promotional period ends will result in high interest charges on the remaining amount. Mitigation strategies include creating a realistic repayment plan, automating payments, and diligently tracking the balance and due dates. Another risk is potential damage to your credit score due to multiple applications or poor management of the transferred balance. To mitigate this, ensure your credit score is healthy before applying, apply for only a few cards, and promptly pay off your balance as planned.

Impact and Implications:

The successful use of balance transfers can significantly improve your financial health. By reducing interest costs, you free up more of your income for other priorities. However, mismanagement can lead to escalating debt and further damage your credit standing. Therefore, a responsible approach is crucial.

Conclusion: Reinforcing the Connection:

The relationship between balance transfer fees and effective debt management is delicate. While the fees represent an upfront cost, they are often outweighed by the long-term savings achieved through lower interest rates. A careful comparison of offers and diligent planning are essential for maximizing the benefits of balance transfers.

Further Analysis: Examining Balance Transfer Fees in Greater Detail:

Balance transfer fees are usually a fixed percentage of the transferred amount, ranging from 3% to 5%. Some cards may waive the fee for a limited time as a promotional incentive. It's crucial to understand this fee upfront and incorporate it into your financial calculations. The fee's impact is more significant on smaller balance transfers, whereas the interest savings become more pronounced with larger balances.

FAQ Section: Answering Common Questions About Balance Transfers:

What is a balance transfer? A balance transfer is moving your credit card debt from one card to another, often to take advantage of a lower interest rate or 0% APR promotional period.

How do I find a good balance transfer offer? Use comparison websites, review card issuer websites, and check your existing credit card offers for balance transfer promotions.

What is a 0% APR? A 0% APR is a promotional interest rate of zero percent offered for a limited period. This allows you to pay down your balance without accruing interest during that time.

What happens after the 0% APR period ends? After the promotional period, the standard APR of the new card will apply, and interest will accrue on your remaining balance.

Can I transfer my balance multiple times? While possible, repeatedly transferring balances can negatively affect your credit score and may be viewed unfavorably by credit card issuers.

What if I can’t pay off the balance before the 0% APR expires? You'll begin accruing interest at the standard APR on the remaining balance, potentially negating any savings achieved through the balance transfer.

Practical Tips: Maximizing the Benefits of Balance Transfers:

- Compare Offers Carefully: Before applying, compare multiple offers, considering the APR, transfer fee, and the length of the promotional period.

- Check Your Credit Score: A high credit score increases your chances of approval and can help you secure better terms.

- Create a Repayment Plan: Develop a realistic plan to pay off your balance before the 0% APR expires.

- Automate Payments: Set up automatic payments to ensure timely repayments and avoid late fees.

- Monitor Your Account: Track your balance and due dates to avoid missing payments or the end of the promotional period.

Final Conclusion: Wrapping Up with Lasting Insights:

Balance transfers are a valuable tool for managing credit card debt. By understanding their mechanics, potential benefits, and risks, you can effectively utilize them to reduce interest costs and improve your financial health. However, responsible planning and diligent repayment are crucial to maximizing the benefits and avoiding the pitfalls. Remember to always compare offers, choose wisely, and develop a clear repayment strategy before initiating a balance transfer. A well-executed balance transfer can provide the breathing room needed to conquer high-interest debt and build a healthier financial future.

Latest Posts

Latest Posts

-

When To Start Retirement Planning

Apr 29, 2025

-

How To Set Up Retirement Planning When Young

Apr 29, 2025

-

How Do You Add Cash Savings To Retirement Planning

Apr 29, 2025

-

Risk Based Mortgage Pricing Definition

Apr 29, 2025

-

Risk Based Haircut Definition

Apr 29, 2025

Related Post

Thank you for visiting our website which covers about What Does Balance Transfer Mean On A Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.