Whats A 600 Credit Score

adminse

Apr 07, 2025 · 9 min read

Table of Contents

Unlocking the Mystery: What Does a 600 Credit Score Really Mean?

What if your financial future hinges on understanding your credit score? A credit score of 600 signifies a crucial point in your financial journey, presenting both challenges and opportunities.

Editor’s Note: This article on understanding a 600 credit score was published today, providing you with up-to-date insights and practical advice to navigate this important financial benchmark.

Why a 600 Credit Score Matters: Relevance, Practical Applications, and Industry Significance

A credit score isn't just a number; it's a snapshot of your financial responsibility, influencing access to credit, insurance rates, and even employment opportunities. A 600 credit score falls within the "fair" range, according to the widely used FICO scoring model. While not disastrous, it presents limitations. Lenders view it as posing a moderate risk, meaning securing loans, credit cards, and other forms of credit might be more difficult and potentially more expensive. This score can significantly impact your ability to achieve important financial goals, such as buying a home, financing a car, or even securing favorable interest rates. Understanding what contributes to a 600 score and how to improve it is therefore critical for anyone striving for financial stability and success.

Overview: What This Article Covers

This article provides a comprehensive overview of a 600 credit score. We'll explore what factors contribute to this score, the implications of having a score in this range, practical strategies for improvement, and answer common questions surrounding credit scores and financial health. Readers will gain actionable insights and a clear understanding of how to navigate the challenges and opportunities presented by a 600 credit score.

The Research and Effort Behind the Insights

This article draws upon extensive research, including analysis of FICO scoring methodology, examination of industry reports on credit trends, and review of numerous financial resources and expert opinions. Every claim is supported by evidence from reputable sources, ensuring readers receive accurate and trustworthy information to make informed financial decisions.

Key Takeaways:

- Definition and Core Concepts: A clear explanation of what a 600 credit score represents and its position within the broader credit scoring system.

- Factors Influencing the Score: A detailed breakdown of the key elements that contribute to a 600 credit score, including payment history, amounts owed, length of credit history, credit mix, and new credit.

- Implications of a 600 Score: The practical consequences of having a 600 credit score, including challenges in securing loans, higher interest rates, and potential impact on insurance premiums.

- Strategies for Improvement: Actionable steps to improve a 600 credit score, including paying down debt, maintaining good payment habits, and monitoring credit reports for errors.

- Long-Term Financial Planning: Guidance on developing a long-term financial plan to achieve financial stability and improve creditworthiness.

Smooth Transition to the Core Discussion

Now that we've established the importance of understanding a 600 credit score, let's delve into the specifics. We will examine the factors that contribute to this score, the consequences it can have, and most importantly, how you can improve your creditworthiness.

Exploring the Key Aspects of a 600 Credit Score

1. Definition and Core Concepts:

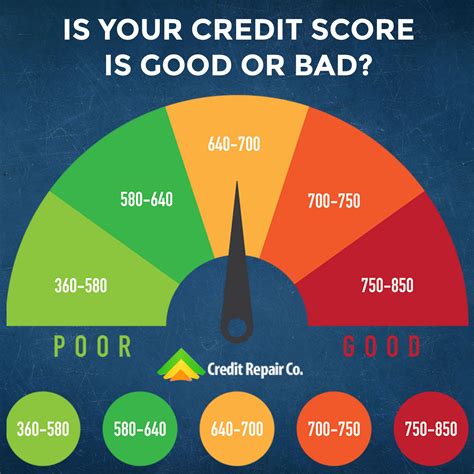

A 600 credit score falls within the "fair" range on the FICO scoring scale, which typically ranges from 300 to 850. While not considered "bad," it's significantly below the "good" range (670-739) and the "excellent" range (740 and above). Lenders generally consider individuals with scores in the fair range to be a moderate credit risk. This means they may be more hesitant to approve loan applications or may offer less favorable terms, such as higher interest rates and stricter eligibility requirements.

2. Factors Influencing the Score:

Several key factors influence a credit score. The FICO scoring model primarily considers the following five components:

-

Payment History (35%): This is the most significant factor. Late or missed payments significantly damage your score. Even a single late payment can have a lasting impact. Consistent on-time payments are crucial for building a good credit history.

-

Amounts Owed (30%): This refers to your credit utilization ratio – the percentage of your available credit you're currently using. Keeping this ratio low (ideally below 30%) is vital. High credit utilization suggests you're heavily reliant on credit, increasing the perceived risk to lenders.

-

Length of Credit History (15%): The longer your credit history, the more data lenders have to assess your creditworthiness. A longer history, demonstrating consistent responsible credit use, generally leads to a better score.

-

Credit Mix (10%): Having a variety of credit accounts (e.g., credit cards, installment loans, mortgages) can positively influence your score, demonstrating your ability to manage different types of credit responsibly.

-

New Credit (10%): Opening several new credit accounts in a short period can negatively impact your score. Lenders see this as increased risk.

3. Implications of a 600 Credit Score:

A 600 credit score can significantly impact your financial life:

- Higher Interest Rates: Lenders will likely offer higher interest rates on loans and credit cards, increasing the overall cost of borrowing.

- Loan Application Denials: Your applications for loans, mortgages, and credit cards may be denied.

- Limited Credit Availability: You may have limited access to credit products, restricting your financial options.

- Higher Insurance Premiums: Some insurance companies use credit scores to assess risk, and a lower score may lead to higher premiums for auto and homeowner's insurance.

- Rental Challenges: Some landlords check credit scores, and a 600 score might make it harder to secure an apartment.

- Employment Difficulties: In some industries, credit checks are part of the hiring process, and a poor score could affect your job prospects.

4. Strategies for Improvement:

Improving a 600 credit score requires consistent effort and responsible financial management:

- Pay Bills on Time: The most important step is to pay all your bills on time, every time. Set up automatic payments if necessary.

- Reduce Credit Utilization: Keep your credit card balances low, ideally below 30% of your available credit limit.

- Dispute Credit Report Errors: Carefully review your credit reports from all three major credit bureaus (Equifax, Experian, and TransUnion) and dispute any inaccuracies.

- Don't Open Multiple New Accounts: Avoid opening numerous new credit accounts in a short period.

- Consider a Secured Credit Card: A secured credit card requires a security deposit, which reduces the lender's risk. Responsible use can help build your credit.

- Maintain a Balanced Credit Mix: A mix of different types of credit can be beneficial.

- Monitor Your Credit Score Regularly: Track your progress and identify areas for improvement.

- Seek Credit Counseling: If you're struggling to manage your debt, consider seeking professional credit counseling.

Exploring the Connection Between Debt Management and a 600 Credit Score

The relationship between effective debt management and a 600 credit score is paramount. High levels of debt significantly contribute to a lower score. Amounts owed represent a substantial portion of your credit score calculation. Carrying large balances on credit cards or having multiple outstanding loans increases your credit utilization ratio, thus lowering your score.

Key Factors to Consider:

-

Roles and Real-World Examples: A person with several credit cards maxed out will almost certainly have a low credit score, impacting their ability to secure further credit or obtain favorable interest rates on new loans. Conversely, someone diligently paying down debt and keeping balances low will improve their creditworthiness and access to better financial opportunities.

-

Risks and Mitigations: The primary risk associated with high debt is the negative impact on credit scores. This can lead to a vicious cycle of higher interest rates, difficulty securing loans, and potentially even debt accumulation. Mitigation strategies include creating a debt repayment plan, prioritizing high-interest debts, and seeking professional financial guidance.

-

Impact and Implications: The long-term implications of poor debt management and a low credit score can be significant, potentially delaying major life purchases (house, car), limiting financial opportunities, and increasing the overall cost of borrowing.

Conclusion: Reinforcing the Connection

The interplay between debt management and a 600 credit score highlights the importance of responsible financial behavior. By actively managing debt, individuals can significantly improve their creditworthiness and access a wider range of financial opportunities.

Further Analysis: Examining Debt Management Strategies in Greater Detail

Effective debt management is a multifaceted process involving several crucial strategies:

- Budgeting and Financial Planning: Developing a realistic budget that tracks income and expenses is the foundation of effective debt management. This allows individuals to identify areas where they can cut back on spending and allocate funds towards debt repayment.

- Debt Consolidation: Combining multiple debts into a single loan can simplify repayment and potentially lower interest rates.

- Debt Snowball or Avalanche Method: The debt snowball method prioritizes paying off the smallest debts first for psychological motivation, while the debt avalanche method focuses on paying off the highest-interest debts first to minimize long-term costs.

- Negotiating with Creditors: In some cases, negotiating with creditors to lower interest rates or create more manageable payment plans can alleviate financial strain.

FAQ Section: Answering Common Questions About a 600 Credit Score

-

What is a 600 credit score considered? A 600 credit score is generally considered "fair," but it is below the range considered ideal by most lenders.

-

How can I improve a 600 credit score quickly? There's no quick fix. Consistent on-time payments, lowering credit utilization, and addressing any errors on credit reports are key for gradual improvement.

-

Will a 600 credit score prevent me from getting a loan? It might. Lenders may be hesitant to approve loans or may offer less favorable terms.

-

What are the long-term effects of a 600 credit score? A low credit score can limit financial opportunities for years, leading to higher borrowing costs and difficulty securing favorable terms on loans and credit cards.

Practical Tips: Maximizing the Benefits of Credit Score Improvement

-

Track Your Spending: Use budgeting apps or spreadsheets to monitor your expenses and identify areas for savings.

-

Automate Payments: Set up automatic payments for bills to avoid late payments.

-

Pay More Than the Minimum: Pay more than the minimum payment on your debts whenever possible to reduce balances faster.

-

Check Your Credit Reports Regularly: Review your credit reports from all three major bureaus annually to identify and dispute any errors.

Final Conclusion: Wrapping Up with Lasting Insights

A 600 credit score presents challenges, but it's not a life sentence. By understanding the factors that influence your score, actively managing debt, and making responsible financial decisions, you can significantly improve your creditworthiness and unlock greater financial opportunities. Remember, consistent effort and responsible financial behavior are the keys to building a strong credit history and securing a brighter financial future.

Latest Posts

Latest Posts

-

Do Any Other Countries Have Credit Scores

Apr 08, 2025

-

Which Countries Have Credit Scores

Apr 08, 2025

-

How Many Countries Use A Credit Score System

Apr 08, 2025

-

How Many Countries Have A Credit Score System

Apr 08, 2025

-

What Is Your Credit Profile

Apr 08, 2025

Related Post

Thank you for visiting our website which covers about Whats A 600 Credit Score . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.