What Will My Minimum Payment Be

adminse

Apr 04, 2025 · 8 min read

Table of Contents

Decoding Your Minimum Payment: Understanding the Mechanics and Avoiding the Pitfalls

What if your understanding of minimum payments could save you thousands of dollars over your lifetime? Mastering minimum payments is crucial for responsible credit card management and achieving long-term financial health.

Editor’s Note: This comprehensive guide to minimum payments was updated today to reflect the latest practices and regulations surrounding credit card debt. Understanding your minimum payment is a key step towards building a strong financial future.

Why Understanding Your Minimum Payment Matters:

Credit cards offer convenience, but carrying a balance can lead to significant debt if not managed effectively. The minimum payment, often a small percentage of your total balance, seems innocuous, yet it's a critical factor influencing your overall debt repayment timeline and the total interest you pay. Failing to understand how minimum payments are calculated and the long-term consequences of only paying the minimum can trap you in a cycle of debt, hindering your financial goals. This article will illuminate the mechanics behind minimum payments, their hidden costs, and strategies for responsible credit card management.

Overview: What This Article Covers:

This article provides a detailed exploration of minimum payments on credit cards. We'll delve into how they're calculated, the impact of interest accrual, the dangers of only making minimum payments, strategies for paying down debt faster, and proactive steps to avoid accumulating high-interest debt. Readers will gain actionable insights to manage credit effectively and build a strong financial foundation.

The Research and Effort Behind the Insights:

This article draws upon extensive research from reputable financial institutions, consumer protection agencies, and academic studies on consumer debt. We have consulted widely available data on credit card interest rates, payment calculations, and the impact of minimum payment strategies on long-term debt. Every point is supported by evidence to ensure the information presented is accurate and trustworthy.

Key Takeaways:

- Definition and Core Concepts: Understanding what constitutes a minimum payment and how it's determined.

- Interest Accrual and its Impact: The significant role of compounding interest when only making minimum payments.

- Strategies for Faster Debt Repayment: Methods to accelerate debt reduction and minimize interest charges.

- Avoiding the Minimum Payment Trap: Proactive measures to prevent accumulating overwhelming credit card debt.

- The Role of Credit Reports and Scores: How minimum payment behaviors affect your creditworthiness.

Smooth Transition to the Core Discussion:

Now that we've established the importance of understanding minimum payments, let's delve into the specifics. We will explore the intricacies of minimum payment calculations, the hidden costs of delayed repayment, and practical strategies for achieving financial freedom.

Exploring the Key Aspects of Minimum Payments:

1. Definition and Core Concepts:

Your minimum payment is the smallest amount your credit card issuer requires you to pay each billing cycle. This amount is usually stated clearly on your monthly statement. It often comprises a percentage of your outstanding balance (typically 1-3%, but it can vary), plus any accrued interest and fees. Some issuers might set a minimum payment amount regardless of your balance, but this is less common.

2. Interest Accrual and its Impact:

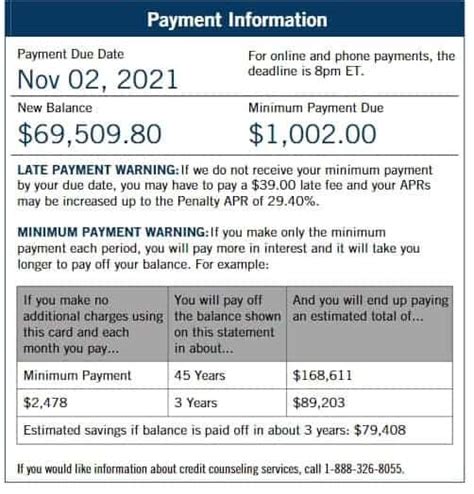

This is where the "minimum payment trap" takes hold. While you're making payments, interest continues to accrue on your outstanding balance. Crucially, this interest is calculated daily on the average daily balance. If you only pay the minimum, a significant portion of your payment goes towards interest, leaving only a small fraction to reduce the principal balance. This means you're essentially paying interest on interest, slowing down your repayment progress significantly and leading to substantially higher overall costs. This effect is amplified by compounding, where interest is charged not only on your initial balance but also on the accumulated interest.

3. Calculating Your Minimum Payment:

The exact calculation of your minimum payment isn't always transparent, but generally, it involves a combination of factors:

- Percentage of outstanding balance: This is the most common component, usually ranging from 1% to 3% of your balance.

- Accrued interest: The interest charges calculated on your average daily balance during the billing cycle.

- Fees: Any late payment fees, over-limit fees, or other charges incurred.

Some issuers might have a predetermined minimum payment amount (e.g., $25), regardless of your balance. If the calculated minimum payment is lower than this set minimum, you'll be required to pay the higher amount.

4. The Dangers of Only Making Minimum Payments:

Paying only the minimum payment may seem like a manageable approach, but it can lead to significant financial difficulties. The interest charges alone can quickly dwarf any progress made in reducing the principal balance, creating a never-ending cycle of debt. This can significantly impact your credit score, limit your access to credit in the future, and cause considerable financial stress.

5. Strategies for Faster Debt Repayment:

Several strategies can help you pay off your credit card debt more quickly and efficiently:

- Debt Avalanche Method: Prioritize paying off the highest-interest debt first, regardless of the balance. This minimizes the total interest paid over time.

- Debt Snowball Method: Focus on paying off the smallest debt first, regardless of the interest rate. This provides a sense of accomplishment and momentum, motivating you to continue paying down your debts.

- Balance Transfer: Transfer your high-interest balance to a credit card with a lower introductory APR. This can save you money on interest during the promotional period. However, be mindful of balance transfer fees and the eventual return to a higher APR.

- Debt Consolidation: Combine multiple debts into a single loan with a lower interest rate. This simplifies payments and can potentially reduce your overall interest expenses.

6. Avoiding the Minimum Payment Trap:

Proactive measures can help you avoid the pitfalls of minimum payments:

- Budgeting and Financial Planning: Create a realistic budget to track your income and expenses. This will help you understand your spending habits and identify areas where you can cut back to allocate more funds towards debt repayment.

- Regular Monitoring of Credit Card Statements: Review your statements thoroughly to understand the interest charges, fees, and payment due dates. Early detection of discrepancies can help you avoid accumulating extra charges.

- Paying More Than the Minimum: Always aim to pay more than the minimum payment each month. Even small extra payments can significantly reduce the total interest paid and shorten the repayment timeline.

- Seeking Professional Financial Advice: If you're struggling to manage your credit card debt, consider seeking guidance from a financial advisor or credit counselor.

Exploring the Connection Between Credit Scores and Minimum Payments:

Your credit score is a crucial factor influencing your financial well-being. Consistent minimum payments (especially if coupled with late payments) significantly impact your creditworthiness. Credit reporting agencies consider your payment history a major component of your score. Regularly paying only the minimum demonstrates poor credit management, lowering your score and making it harder to obtain loans or secure favorable interest rates in the future.

Key Factors to Consider:

- Roles and Real-World Examples: Individuals who only pay minimum payments often find themselves struggling financially, facing higher interest charges, and ultimately paying significantly more for their purchases.

- Risks and Mitigations: The risk is prolonged debt, higher interest payments, and a damaged credit score. Mitigation involves budgeting, prioritizing debt repayment, and exploring debt management strategies.

- Impact and Implications: The long-term impact includes financial instability, limited access to credit, and potential legal repercussions.

Conclusion: Reinforcing the Connection:

The connection between minimum payments and long-term financial health is undeniable. Consistent minimum payments contribute to a cycle of debt, increasing overall costs and damaging credit scores. Proactive planning, responsible spending habits, and strategically addressing credit card debt are critical for achieving long-term financial stability.

Further Analysis: Examining Interest Rates in Greater Detail:

High interest rates on credit cards significantly exacerbate the problems associated with minimum payments. The higher the interest rate, the more rapidly interest accrues, making it exceedingly difficult to reduce the principal balance when only paying the minimum. Understanding the APR (Annual Percentage Rate) on your credit card is essential for making informed decisions about repayment strategies.

FAQ Section: Answering Common Questions About Minimum Payments:

Q: What happens if I miss a minimum payment?

A: Missing a minimum payment can result in late fees, increased interest charges, and a negative impact on your credit score.

Q: Can I negotiate a lower minimum payment with my credit card issuer?

A: While it's not always guaranteed, you can try contacting your credit card issuer to discuss your situation. They might offer options like a hardship program or a temporary reduction in your minimum payment.

Q: Is it always better to pay off the entire balance each month?

A: Yes, paying off your balance in full each month avoids interest charges altogether and protects your credit score.

Practical Tips: Maximizing the Benefits of Responsible Credit Card Use:

- Track your spending: Use budgeting apps or spreadsheets to monitor your expenses and ensure you stay within your limits.

- Pay more than the minimum: Make extra payments whenever possible to accelerate debt repayment.

- Set up automatic payments: This ensures you never miss a payment and helps maintain a good payment history.

- Consider debt consolidation or balance transfers: Explore options to reduce your interest rates and simplify your payments.

- Seek professional help if needed: Don’t hesitate to contact a credit counselor or financial advisor if you're struggling with debt.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding your minimum payment is a crucial step toward responsible credit card management. While minimum payments provide a seemingly convenient option, they often lead to a cycle of accumulating interest and debt. By adopting proactive strategies, understanding the hidden costs, and prioritizing debt repayment, you can break free from the minimum payment trap and build a strong foundation for your financial future. Remember, financial responsibility is key to achieving lasting financial success.

Latest Posts

Latest Posts

-

What Is My Jcpenney Credit Card Number

Apr 05, 2025

-

Jcpenney How Much Do They Pay

Apr 05, 2025

-

Minimum Penarikan Paypal

Apr 05, 2025

-

How Much Paypal Transaction Fee

Apr 05, 2025

-

Paypal Minimum Withdrawal Indonesia

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about What Will My Minimum Payment Be . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.