What Is The Statement Date On Your Credit Card

adminse

Apr 04, 2025 · 9 min read

Table of Contents

What's the secret code hidden on your credit card statement? Unlocking the power of the statement date!

Understanding your statement date is key to managing your finances effectively and avoiding unnecessary fees.

Editor’s Note: This article on understanding your credit card statement date was published today, providing you with the most up-to-date information to help you manage your credit effectively. We've covered everything from what the statement date actually means to how it impacts your credit score and spending habits.

Why Your Credit Card Statement Date Matters: Relevance, Practical Applications, and Financial Significance

Your credit card statement date might seem like a minor detail, but it significantly impacts your financial health. It's the cornerstone of understanding your spending, calculating interest, and even avoiding late payment fees. This seemingly small piece of information affects your credit utilization ratio, a crucial factor in your credit score. Ignoring it can lead to missed payments, increased interest charges, and damage to your creditworthiness. Understanding your statement date is essential for responsible credit card management and achieving long-term financial stability.

Overview: What This Article Covers

This in-depth article explores every facet of your credit card statement date. We'll define the statement date, explain how it's determined, illustrate its impact on interest calculations and payment deadlines, delve into its role in credit scoring, and offer practical tips for effective management. Finally, we'll address frequently asked questions and provide actionable strategies to maximize the benefits of understanding this critical date.

The Research and Effort Behind the Insights

This article draws upon extensive research from reputable financial institutions, consumer protection agencies, and credit reporting bureaus. We've analyzed various credit card agreements, examined industry best practices, and incorporated insights from financial experts to ensure accuracy and provide actionable advice. Our goal is to empower you with the knowledge needed to make informed decisions regarding your credit card usage.

Key Takeaways: Summarize the Most Essential Insights

- Definition and Core Concepts: A precise definition of the credit card statement date and its fundamental role in credit card management.

- Statement Date Calculation: How the statement date is determined and its relationship to your transaction posting dates.

- Impact on Interest Calculations: How the statement date influences the calculation of interest charges on outstanding balances.

- Payment Due Date Determination: The relationship between the statement date and the payment due date.

- Credit Score Implications: The effect of the statement date on your credit utilization ratio and, consequently, your credit score.

- Practical Strategies: Actionable tips and techniques for effective credit card statement date management.

Smooth Transition to the Core Discussion

Now that we've established the importance of understanding your statement date, let's delve into the specifics, examining its calculation, impact on finances, and strategies for effective management.

Exploring the Key Aspects of Your Credit Card Statement Date

Definition and Core Concepts:

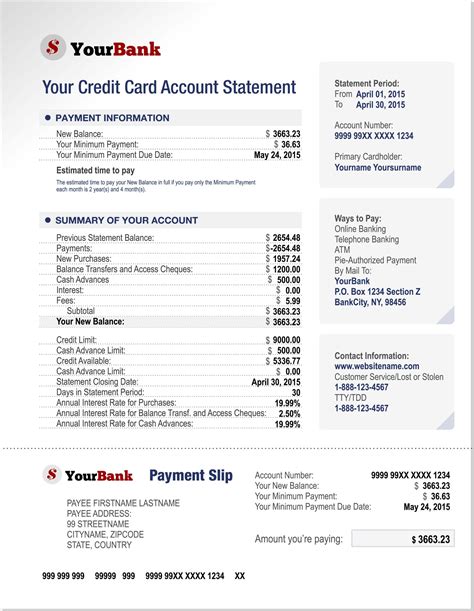

The statement date is the day each month your credit card company generates a summary of your account activity. This summary, your credit card statement, details all transactions made during the previous billing cycle, including purchases, payments, and any applicable fees or interest charges. The statement date is not the day you receive your statement in the mail or online; rather, it's the date the statement is generated. This is crucial because the statement date is the basis for calculating your payment due date and the period for which interest is calculated.

Statement Date Calculation:

The statement date is typically fixed, meaning it falls on the same day each month. This date is established when you open your credit card account and is usually specified in your credit card agreement. While many cards have a statement date near the end of the month, it can vary significantly. Some banks might choose the 1st, 15th, or even the 20th of the month. Your billing cycle, the period between statement dates, is usually 28-31 days, but this also depends on your card issuer. It's vital to check your credit card agreement to determine your precise statement date and billing cycle length.

Impact on Interest Calculations:

The statement date is critical in determining the interest charged on your outstanding balance. Most credit card companies calculate interest based on your average daily balance during the billing cycle. The statement date marks the end of that billing cycle, and the interest calculated is usually added to your balance on the following statement date. Understanding your statement date allows you to predict interest charges more accurately and helps in budget planning.

Payment Due Date Determination:

Your payment due date is not the same as your statement date. It is usually a fixed number of days after the statement date (e.g., 21 days). This grace period gives you time to review your statement, make a payment, and avoid late payment fees. The payment due date is clearly indicated on your statement. Missing this deadline can result in penalties, negatively impacting your credit score and potentially incurring further interest charges.

Credit Score Implications:

Your statement date indirectly influences your credit score through its effect on your credit utilization ratio. This ratio represents the proportion of your available credit that you're currently using. A high credit utilization ratio (over 30%) negatively impacts your credit score. Understanding your statement date allows you to monitor your spending throughout the billing cycle, ensuring you don't exceed your credit limit just before the statement date, thus minimizing the negative impact on your credit score.

Exploring the Connection Between Payment Due Date and Your Credit Card Statement Date

The payment due date is inextricably linked to the statement date. It’s the deadline for paying your credit card balance without incurring late payment fees. The exact number of days between the statement date and payment due date varies depending on the card issuer, but it's typically between 21 and 25 days. Understanding this connection ensures you can make timely payments and avoid damaging your credit score.

Key Factors to Consider

Roles and Real-World Examples: Let's say your statement date is the 20th of each month, and your due date is 21 days later. If your statement is generated on the 20th of October, your payment due date will be November 10th. Failure to pay by this date will result in a late payment fee and a negative mark on your credit report.

Risks and Mitigations: The primary risk associated with misunderstanding your statement date is late payments. Mitigation involves carefully noting your statement date and payment due date in your calendar or using automatic payment options to ensure on-time payments.

Impact and Implications: Failing to understand the connection between statement date and payment due date can lead to late fees, higher interest charges, and ultimately a lower credit score. This can make it harder to obtain loans or credit in the future.

Conclusion: Reinforcing the Connection

The relationship between the statement date and payment due date is paramount in responsible credit card management. By understanding this connection and planning accordingly, you can avoid late payment fees and maintain a healthy credit score. Regularly reviewing your statement and setting payment reminders is crucial for avoiding financial penalties.

Further Analysis: Examining Credit Utilization Ratio in Greater Detail

The credit utilization ratio is a significant factor influencing your credit score. It's calculated by dividing your outstanding credit card balance by your total credit limit. A high credit utilization ratio (above 30%) suggests you're using a large portion of your available credit, which can signal financial instability to lenders. Conversely, keeping your credit utilization ratio low (ideally below 10%) demonstrates responsible credit management and positively impacts your credit score. Understanding your statement date allows you to strategically manage your spending and keep your credit utilization ratio low, thereby protecting your creditworthiness.

FAQ Section: Answering Common Questions About Credit Card Statement Dates

What happens if I miss my payment due date?

Missing your payment due date will likely result in late payment fees, negatively impacting your credit score. You may also be charged additional interest on your outstanding balance.

How can I find my statement date?

Your statement date is usually printed on your credit card statement and can be found in your credit card agreement. You can also find it by logging into your online banking account.

Can I change my statement date?

Some credit card companies allow you to change your statement date, although it may require contacting customer service.

How does my statement date affect my interest rate?

Your statement date marks the end of your billing cycle, and interest is calculated based on your average daily balance during that period. The statement date does not directly affect your interest rate itself; however, the interest accrued is reflected on your next statement.

What if I have multiple credit cards with different statement dates?

Managing multiple credit cards with different statement dates requires careful planning and organization. Use a calendar or budgeting app to track each card's statement date and due date.

Practical Tips: Maximizing the Benefits of Understanding Your Statement Date

- Note your statement date and payment due date: Write these dates down in your planner or set reminders on your phone or computer.

- Review your statement carefully: Check for any errors or unauthorized transactions.

- Pay your bill on time: Avoid late fees and protect your credit score by making timely payments.

- Monitor your credit utilization ratio: Track your spending throughout the billing cycle to keep your credit utilization ratio low.

- Utilize automatic payments: Set up automatic payments to ensure you never miss a due date.

- Consider budgeting tools: Many budgeting apps can help you track your spending and manage your credit card payments effectively.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding your credit card statement date is not just about avoiding fees; it's about proactively managing your finances and building a strong credit history. By implementing the strategies outlined in this article, you can effectively control your spending, avoid penalties, and improve your overall financial well-being. Take control of your financial future by paying close attention to this crucial date on your credit card statement.

Latest Posts

Latest Posts

-

How Is The Minimum Monthly Payment On A Credit Card Calculated

Apr 05, 2025

-

Why Is It More Difficult To Get Out Of Debt When Only Paying The Minimum Payment Responses

Apr 05, 2025

-

Why Is It More Difficult To Get Out Of Debt When Only Paying The Minimum Payment Edpuzzle

Apr 05, 2025

-

Why Is It More Difficult To Get Out Of Debt When Only Paying The Minimum Payment Quizlet

Apr 05, 2025

-

Minimum Payment Home Depot Card

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about What Is The Statement Date On Your Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.