What Is The Minimum Payment On A Credit Card With A $6000 Balance

adminse

Apr 05, 2025 · 10 min read

Table of Contents

Decoding Minimum Credit Card Payments: A $6000 Balance Deep Dive

What happens if you only pay the minimum on a $6000 credit card balance?

Ignoring minimum payments on a significant debt like $6000 can lead to a financial spiral of accumulating interest and fees, ultimately costing far more than the initial balance.

Editor’s Note: This article provides a comprehensive analysis of minimum credit card payments, focusing on a $6000 balance. We'll explore the intricacies of interest calculations, the long-term financial implications of minimum payments, and strategies for managing high-balance credit card debt effectively. Updated October 26, 2023.

Why Understanding Minimum Payments Matters

Understanding minimum payments on credit cards is crucial for responsible financial management. For many, a $6000 credit card balance represents a significant debt burden. Failing to grasp the implications of only paying the minimum can lead to a cycle of debt that's difficult to escape. This article will delve into the mechanics of minimum payments, highlighting the hidden costs and providing actionable strategies for debt reduction. It's important to remember that minimum payment amounts are not fixed; they vary based on your card's terms and your outstanding balance.

Overview: What This Article Covers

This article will dissect the complexities of minimum payments on a $6000 credit card balance. We will explore:

- Calculating Minimum Payments: Understanding how minimum payments are determined.

- The High Cost of Minimum Payments: Analyzing the impact of interest accrual over time.

- Factors Influencing Minimum Payment Amounts: Exploring variables like APR, balance, and card issuer policies.

- Strategies for Reducing a $6000 Credit Card Balance: Exploring effective debt management techniques.

- The Dangers of Only Paying the Minimum: Highlighting the potential consequences of prolonged minimum payments.

- Alternative Debt Management Options: Investigating options like balance transfers and debt consolidation.

- Frequently Asked Questions (FAQ): Addressing common queries about minimum credit card payments.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon information from leading financial institutions, consumer protection agencies, and reputable financial websites. Data on average credit card interest rates and minimum payment calculations have been sourced from publicly available information to ensure accuracy and credibility. The analysis presented here is designed to provide readers with a clear and comprehensive understanding of this critical financial topic.

Key Takeaways:

- Minimum payments are deceptively low: They often only cover a fraction of the interest accrued, meaning you'll pay down very little of the principal balance.

- High APRs exacerbate the problem: A high annual percentage rate (APR) significantly increases the interest charged, prolonging the repayment period.

- The longer you only pay the minimum, the more you'll pay in interest: This can easily result in paying thousands of dollars more than the original debt.

- Proactive debt management is crucial: Strategies like budgeting, debt consolidation, and balance transfers can help you escape the cycle of minimum payments.

Smooth Transition to the Core Discussion

Now that we've established the importance of understanding minimum credit card payments, let's delve into the specifics, focusing on the implications of a $6000 balance.

Exploring the Key Aspects of Minimum Credit Card Payments

1. Calculating Minimum Payments:

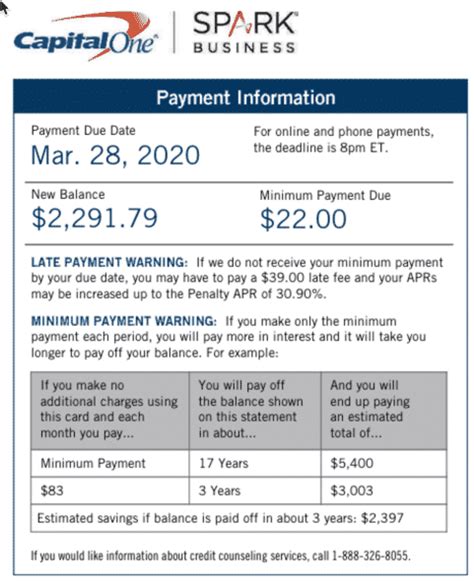

The minimum payment on a credit card is typically a percentage of your outstanding balance, often between 1% and 3%, or a fixed minimum dollar amount, whichever is greater. For a $6000 balance, a 2% minimum payment would be $120. However, this varies from card to card and sometimes depends on your payment history. It's crucial to check your credit card statement for the precise amount. Some issuers might use a more complex formula, taking into account factors like your credit score and payment history.

2. The High Cost of Minimum Payments:

Paying only the minimum on a $6000 balance can trap you in a cycle of debt. Let's illustrate this with an example. Assume a 19% APR. If you only pay the minimum ($120), a significant portion of that payment will go towards interest, leaving a small amount to reduce the principal balance. Over time, this results in paying considerably more in interest than the original $6000 debt. Using a credit card payment calculator (easily found online), you can simulate different payment scenarios and observe how the interest accrues over various periods. The difference between paying the minimum versus making larger payments is substantial.

3. Factors Influencing Minimum Payment Amounts:

Several factors influence the minimum payment amount calculated on your credit card statement:

- Annual Percentage Rate (APR): A higher APR leads to higher interest charges, potentially increasing the minimum payment to cover at least the interest accrued.

- Outstanding Balance: As your balance increases, so does the minimum payment (percentage-based calculations).

- Card Issuer Policies: Different credit card issuers have varying policies regarding minimum payment calculations. Some might have a fixed minimum dollar amount, regardless of the balance.

- Payment History: Consistent on-time payments might not influence the minimum payment amount directly, but a history of late or missed payments could affect your APR and thus the overall cost.

4. Strategies for Reducing a $6000 Credit Card Balance:

Effectively managing a $6000 credit card balance requires proactive strategies:

- Create a Budget: Track your income and expenses to identify areas where you can cut back. This frees up funds to allocate toward debt repayment.

- Increase Your Payments: Pay more than the minimum payment each month. Even small increases significantly reduce the overall interest paid.

- Debt Consolidation: Consider consolidating your debt into a lower-interest loan, simplifying payments and potentially reducing your monthly expenses.

- Balance Transfer: Transfer your balance to a credit card with a 0% introductory APR, giving you time to pay down the principal without incurring further interest (be aware of balance transfer fees).

- Negotiate with Your Credit Card Company: Contact your credit card company and discuss options like lowering your interest rate or setting up a payment plan.

The Dangers of Only Paying the Minimum:

Paying only the minimum on a $6000 credit card balance over an extended period carries significant financial risks:

- Accumulating Interest: The primary risk is accruing substantial interest charges, greatly increasing the total cost of the debt.

- Prolonged Debt: Paying only the minimum significantly extends the repayment period, potentially tying up your finances for years.

- Negative Impact on Credit Score: High credit utilization (the percentage of your available credit that you're using) negatively impacts your credit score. A high balance can significantly lower your score.

- Financial Stress: The weight of a large credit card balance can create significant financial stress and anxiety.

Alternative Debt Management Options:

Besides the strategies mentioned above, consider these options:

- Debt Management Plans (DMPs): A DMP involves working with a credit counseling agency to create a plan to manage and pay off your debts.

- Debt Settlement: Negotiating with creditors to settle your debt for a lower amount than you owe. This negatively impacts your credit score, but it can help you avoid bankruptcy.

- Bankruptcy: In extreme cases, bankruptcy might be considered as a last resort to manage overwhelming debt. However, it has severe long-term consequences on your credit history.

Exploring the Connection Between Interest Rates and Minimum Payments

The relationship between interest rates and minimum payments is directly proportional. A higher APR means more interest is charged on your outstanding balance, which in turn increases the minimum payment to cover at least the interest accrued. This creates a vicious cycle; the higher the interest, the longer it takes to pay off the debt even with consistent minimum payments, and the more you will ultimately pay in interest.

Key Factors to Consider:

-

Roles and Real-World Examples: Consider a scenario where the APR is 25%. The minimum payment would be insufficient to significantly decrease the principal balance, causing a snowball effect of accruing interest. Conversely, a lower APR, like 10%, would allow more of the minimum payment to go towards the principal, shortening the repayment period and lessening the total interest paid.

-

Risks and Mitigations: The risk of paying only the minimum with a high APR is substantial. Mitigation strategies include negotiating a lower APR with your credit card company, consolidating debts, or utilizing a balance transfer to a card with a promotional 0% APR period.

-

Impact and Implications: The long-term impact of continuously paying only the minimum at a high APR can be devastating. It can lead to years of debt, a severely damaged credit score, and substantial financial stress. Conversely, proactive debt management leads to financial stability and peace of mind.

Conclusion: Reinforcing the Connection

The relationship between interest rates and minimum payments is paramount in managing credit card debt. Understanding this connection empowers consumers to make informed decisions regarding their debt repayment strategies. A proactive approach, which involves considering lower-APR options and making payments that exceed the minimum, is crucial for avoiding the pitfalls of a high-interest debt burden.

Further Analysis: Examining Interest Calculation in Greater Detail

Credit card interest is usually calculated using the average daily balance method. This means the interest is calculated daily on the balance you carry each day of the billing cycle. Understanding this calculation is essential to grasp the impact of carrying a high balance. It highlights why even small differences in APR or payment amounts can lead to significant differences in the total cost of borrowing.

FAQ Section: Answering Common Questions About Minimum Credit Card Payments

Q: What happens if I consistently pay only the minimum on my credit card? A: You will pay significantly more in interest over the long term, extending the repayment period considerably. Your credit utilization will remain high, negatively affecting your credit score.

Q: Can I negotiate my minimum payment amount? A: You can't directly negotiate the calculated minimum payment, but you can negotiate with your credit card company to create a payment plan that works within your budget.

Q: What's the best way to get out of credit card debt? A: A combination of budgeting, increasing your payments, debt consolidation, balance transfers, and potentially working with a credit counselor are the most effective strategies.

Q: How does paying more than the minimum affect my credit score? A: Paying more than the minimum reduces your credit utilization ratio, improving your credit score. It also shortens the repayment period, reducing the total amount of interest paid.

Practical Tips: Maximizing the Benefits of Responsible Credit Card Management

-

Track Your Spending: Use budgeting apps or spreadsheets to monitor your spending habits and identify areas for reduction.

-

Pay More Than the Minimum: Aim to pay at least double the minimum payment, or even more, if financially feasible.

-

Negotiate with Creditors: Don't hesitate to contact your credit card company to explore options for lowering your interest rate or creating a payment plan.

-

Explore Debt Consolidation Options: Consider consolidating high-interest debts into a lower-interest loan to streamline payments and reduce your overall cost.

-

Seek Professional Help: If you're struggling to manage your credit card debt, contact a reputable credit counseling agency for assistance.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding minimum credit card payments, especially when dealing with a significant balance like $6000, is critical for responsible financial management. Failing to grasp the implications of only making minimum payments can lead to a cycle of debt that is both costly and stressful. By employing the strategies and insights provided in this article, individuals can effectively manage their credit card debt, paving the way for improved financial health and stability. Remember, proactive debt management is key to avoiding the long-term financial consequences of consistently paying only the minimum.

Latest Posts

Latest Posts

-

Apps To Help Manage Money

Apr 06, 2025

-

Money Management Apps

Apr 06, 2025

-

How To Create A Personal Finance App

Apr 06, 2025

-

How To Create A Budget App

Apr 06, 2025

-

How To Set Up Money Manager App

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about What Is The Minimum Payment On A Credit Card With A $6000 Balance . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.