What Is The Minimum Payment On A 500 Credit Card

adminse

Apr 04, 2025 · 7 min read

Table of Contents

What's the magic number? Unlocking the mysteries of minimum credit card payments.

Understanding your minimum payment is crucial for responsible credit card use and avoiding crippling debt.

Editor’s Note: This article on minimum credit card payments, specifically focusing on a $500 credit limit card, was published today. We aim to provide clear, actionable advice to help you manage your credit responsibly.

Why Minimum Credit Card Payments Matter: Relevance, Practical Applications, and Financial Well-being

Navigating the world of credit cards can feel overwhelming, especially when dealing with minimum payments. Understanding this seemingly small detail is paramount to maintaining good credit health and avoiding a spiral of debt. While a $500 credit limit might seem modest, the principles of minimum payment calculation and their implications apply to all credit cards, regardless of the credit limit. This article focuses on a $500 card to provide a clear, relatable example for many consumers, particularly those new to credit or managing a smaller credit line. Understanding minimum payments protects your credit score, prevents late fees and interest accumulation, and empowers you to make informed financial decisions.

Overview: What This Article Covers

This article provides a comprehensive guide to minimum credit card payments on a $500 credit limit card. We'll explore how minimum payments are calculated, the hidden costs of only making minimum payments, strategies for managing your payments effectively, and the potential long-term consequences of consistently paying only the minimum. We'll also examine the differences between various credit card issuers and the impact of promotional periods (such as 0% APR offers) on minimum payment calculations.

The Research and Effort Behind the Insights

This article draws upon research from reputable financial institutions, consumer protection agencies, and credit reporting bureaus. Data on average interest rates, late fees, and the impact of minimum payments on credit scores have been analyzed to ensure accuracy and provide actionable insights. The information presented is based on commonly accepted financial principles and industry practices.

Key Takeaways:

- Minimum Payment Calculation: Understanding the factors that determine the minimum payment amount.

- Cost of Minimum Payments: Analyzing the long-term financial implications of only paying the minimum.

- Effective Payment Strategies: Developing a plan to manage credit card debt effectively.

- Avoiding Late Fees and Penalties: Strategies to ensure timely payments and avoid additional charges.

- Impact on Credit Score: The correlation between minimum payments and creditworthiness.

Smooth Transition to the Core Discussion

Now that we understand the importance of minimum payments, let's delve into the specifics of how they are calculated and the potential consequences of relying solely on minimum payments.

Exploring the Key Aspects of Minimum Payments on a $500 Credit Card

1. Definition and Core Concepts:

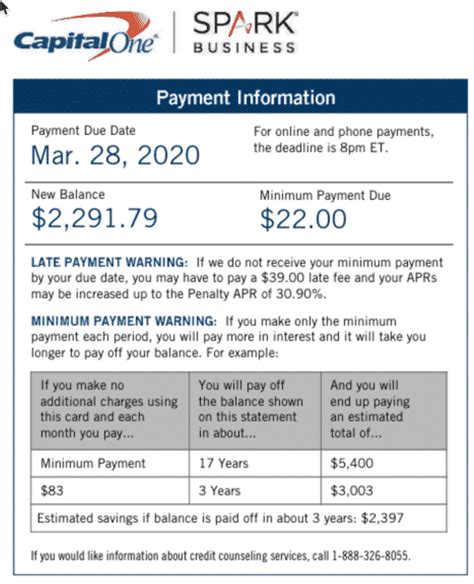

The minimum payment on a credit card is the smallest amount a cardholder can pay each billing cycle without incurring a late payment fee. This amount is typically a percentage of the outstanding balance (often between 1% and 3%) or a fixed minimum dollar amount, whichever is greater. For a $500 credit card, if the minimum payment is 2%, the minimum due would be $10. However, the issuer may impose a higher minimum payment floor (e.g., $25), which would be the amount owed in that case.

2. Applications Across Industries:

The minimum payment calculation is fairly standardized across the credit card industry. However, specific details – the percentage used, the minimum dollar amount, and the calculation method – can vary slightly from one credit card issuer to another. Some issuers may have different minimum payment structures for different card products (e.g., secured vs. unsecured cards).

3. Challenges and Solutions:

One major challenge is the misconception that consistently paying only the minimum payment is a viable long-term strategy. This is far from the truth. Paying only the minimum keeps a significant portion of the balance outstanding, meaning interest charges accumulate rapidly, leading to substantially higher overall costs.

4. Impact on Innovation (Debt Management Strategies):

The credit card industry is increasingly leveraging technology to help consumers manage their debt. Many credit card issuers offer online tools and mobile apps that allow cardholders to track their spending, view their minimum payments, and manage their accounts effectively. This can be an invaluable tool for consumers to remain in control of their finances.

Closing Insights: Summarizing the Core Discussion

Understanding your minimum credit card payment is not just about avoiding late fees; it's about developing a responsible financial strategy. While the minimum payment might seem manageable initially, the accumulation of interest can quickly transform a manageable debt into a substantial financial burden.

Exploring the Connection Between Interest Rates and Minimum Payments

The relationship between interest rates and minimum payments is crucial. Higher interest rates mean a larger portion of your minimum payment goes towards interest, leaving a smaller amount to reduce the principal balance. This can significantly extend the repayment period and increase the overall cost of borrowing. For a $500 credit card with a high interest rate, paying only the minimum could mean paying significantly more over time than the initial balance.

Key Factors to Consider:

-

Roles and Real-World Examples: A $500 credit card with a 20% APR and a $10 minimum payment will see most of the payment going towards interest, leading to slow balance reduction. A $100 balance after one year could be entirely due to accumulated interest.

-

Risks and Mitigations: The risk is a long repayment period and significantly increased cost. Mitigation involves paying more than the minimum each month and potentially considering balance transfer options to lower interest rates.

-

Impact and Implications: The longer it takes to repay the debt, the higher the overall interest paid. This impacts future financial planning, potentially hindering savings and other investments.

Conclusion: Reinforcing the Connection

The interplay between interest rates and minimum payments highlights the importance of making informed decisions when using credit cards. Ignoring this relationship can lead to a debt trap that takes years to escape.

Further Analysis: Examining Interest Rates in Greater Detail

Understanding how interest is calculated is vital. Credit card interest is typically compounded daily, meaning interest is calculated on the outstanding balance each day. This daily compounding is then added to the principal balance to create the next day's base interest amount, leading to a rapid growth of interest over time. Understanding this concept is essential to appreciating the long-term effects of making only minimum payments.

Example: If you only pay the minimum payment each month on a $500 credit card with a high interest rate, the interest will accumulate quickly. After just a year or two, your total repayment amount could exceed the initial $500 due to accrued interest alone, meaning you’ll be paying considerably more for a smaller initial borrowing amount.

FAQ Section: Answering Common Questions About Minimum Payments

What is the typical minimum payment percentage on a credit card? It ranges from 1% to 3% of the outstanding balance, or a fixed minimum dollar amount, whichever is greater.

What happens if I only pay the minimum payment? You'll pay more in interest over time and extend the repayment period.

Can I pay more than the minimum payment? Absolutely! Paying more than the minimum reduces your principal balance faster, saving you money on interest in the long run.

What if I miss a minimum payment? You'll likely incur a late fee and it will negatively impact your credit score.

How do minimum payments affect my credit score? Consistently paying only the minimum can negatively affect your credit utilization ratio, which is a factor in your credit score. Ideally, keep your credit utilization ratio under 30%.

Practical Tips: Maximizing the Benefits of Responsible Credit Card Use

-

Budgeting: Create a realistic monthly budget that accounts for credit card payments and other expenses.

-

Tracking Expenses: Monitor your credit card spending to avoid exceeding your credit limit and to help prioritize debt repayment.

-

Paying More Than the Minimum: Make a conscious effort to pay more than the minimum payment each month, reducing your principal balance faster.

-

Debt Consolidation: Explore options like debt consolidation loans to potentially lower your interest rate and simplify repayments.

-

Seeking Financial Advice: Don't hesitate to seek help from financial advisors if you need assistance managing your credit card debt.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding minimum credit card payments is crucial for responsible financial management. While paying the minimum might seem convenient in the short term, it can lead to a cycle of debt that’s difficult to escape. By understanding how minimum payments are calculated, the implications of only paying the minimum, and adopting responsible credit card use strategies, you can avoid financial pitfalls and maintain good credit health. Remember, responsible credit card use empowers you to build a strong financial future.

Latest Posts

Latest Posts

-

What Is The Minimum Salary For American Express Credit Card

Apr 05, 2025

-

What Is The Lowest American Express Credit Card

Apr 05, 2025

-

What Is The Minimum Payment For Amex Credit Card

Apr 05, 2025

-

What Is The Minimum Payment On A American Express Credit Card

Apr 05, 2025

-

Minimum Payment 0 Dollars

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about What Is The Minimum Payment On A 500 Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.