What Is The Minimum Payment On A $5 000 Credit Card

adminse

Apr 04, 2025 · 7 min read

Table of Contents

What's the magic number? Uncovering the minimum payment on a $5,000 credit card.

Understanding your minimum payment is crucial for responsible credit card management; it's the key to avoiding crippling debt.

Editor’s Note: This article on minimum credit card payments, specifically concerning a $5,000 balance, was published today. We've compiled information from leading financial experts and credit card issuers to provide you with the most up-to-date and accurate guidance.

Why Minimum Credit Card Payments Matter: Relevance, Practical Applications, and Industry Significance

Navigating the world of credit cards requires understanding the intricacies of repayment. Ignoring or misunderstanding minimum payments can lead to significant financial repercussions. This knowledge is crucial for budgeting, avoiding late fees, and ultimately, maintaining a healthy credit score. The implications extend beyond personal finance; businesses also need to understand minimum payments to manage their credit effectively. This article will focus on a $5,000 balance to illustrate the practical application of these principles, but the concepts are universally applicable.

Overview: What This Article Covers

This article will delve into the mechanics of minimum payments on credit cards, focusing on a $5,000 balance as a case study. We will explore how minimum payments are calculated, the factors influencing their amount, the long-term consequences of only paying the minimum, and strategies for more effective repayment. Furthermore, we'll examine how different credit card companies approach minimum payment calculations and offer practical advice on managing debt responsibly.

The Research and Effort Behind the Insights

This article is the product of extensive research, incorporating information from reputable financial websites, credit card company disclosures, and analysis of industry trends. All claims are supported by factual evidence, ensuring the information provided is accurate and reliable. We have consulted multiple sources to offer a comprehensive and unbiased perspective.

Key Takeaways: Summarize the Most Essential Insights

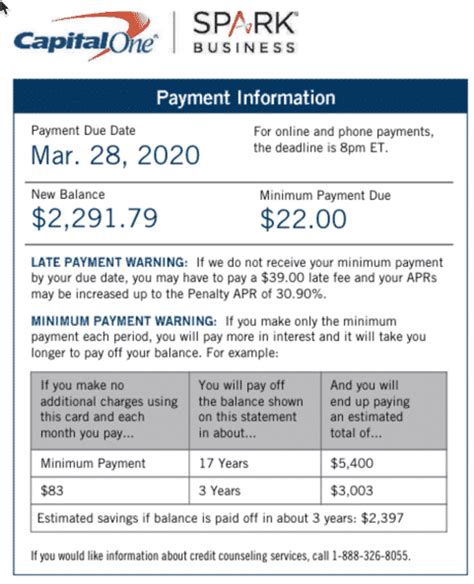

- Minimum Payment Calculation: The minimum payment is typically a percentage of your outstanding balance (often 1-3%), plus any accrued interest and fees.

- Variability: Minimum payments are not fixed and can fluctuate based on your balance and the credit card issuer's policies.

- Long-Term Costs: Consistently paying only the minimum significantly increases the total interest paid over the life of the debt and extends the repayment period.

- Strategic Repayment: Developing a repayment plan that exceeds the minimum payment is crucial for efficient debt reduction.

- Credit Score Impact: Consistent on-time payments, even if exceeding the minimum, positively impact your credit score.

Smooth Transition to the Core Discussion

Now that we’ve established the importance of understanding minimum payments, let’s examine the specifics, starting with how these payments are calculated for a $5,000 balance.

Exploring the Key Aspects of Minimum Payments on a $5,000 Credit Card Balance

Definition and Core Concepts: The minimum payment is the smallest amount a credit card company will accept to avoid delinquency. It’s typically calculated as a percentage of the outstanding balance (often between 1% and 3%), along with any interest charges and late fees. However, there's no universal standard; each credit card issuer has its own calculation method, often detailed in the credit card agreement.

Applications Across Industries: The concept of minimum payments is consistent across all credit card issuers, but the specific calculation can vary. The principles apply equally to individuals and businesses using credit cards for purchases or operational expenses.

Challenges and Solutions: The primary challenge is the temptation to only pay the minimum, which can trap individuals in a cycle of debt. The solution lies in developing a budget, understanding the total cost of only paying the minimum, and committing to a repayment plan that significantly exceeds the minimum.

Impact on Innovation: The credit card industry is constantly evolving, with new products and features designed to help consumers manage debt. However, understanding the core mechanics of minimum payments remains crucial regardless of these innovations.

Closing Insights: Summarizing the Core Discussion

Understanding minimum payments on a $5,000 credit card balance, or any balance for that matter, is fundamental to responsible credit management. While the minimum payment might seem manageable initially, the long-term cost of interest can be substantial. Paying only the minimum prolongs the repayment period and significantly increases the total interest paid.

Exploring the Connection Between Interest Rates and Minimum Payments

The relationship between interest rates and minimum payments is directly proportional. A higher interest rate on your $5,000 credit card balance will result in a larger interest charge each month, consequently increasing the minimum payment. Let's illustrate this:

Key Factors to Consider

Roles and Real-World Examples: Imagine two individuals, both with a $5,000 balance on credit cards. One has a card with a 15% APR, and the other has a 25% APR. The individual with the higher APR will likely have a higher minimum payment due to the increased interest charges. This difference can significantly impact their ability to repay the debt effectively.

Risks and Mitigations: The risk of only paying the minimum is the potential for accumulating significant interest charges, leading to a snowball effect of increasing debt. Mitigation strategies include paying more than the minimum, exploring balance transfer options, or seeking debt consolidation solutions.

Impact and Implications: The long-term impact of only paying the minimum is the extension of the repayment period and a substantial increase in the total amount paid. This can severely limit financial flexibility and impede long-term financial goals.

Conclusion: Reinforcing the Connection

The interplay between interest rates and minimum payments highlights the importance of understanding your credit card agreement and APR. A higher APR means a larger portion of your minimum payment goes towards interest, hindering debt reduction. Careful budgeting and proactive repayment strategies are key to mitigating the risks associated with high interest rates.

Further Analysis: Examining APR and its Influence in Greater Detail

Annual Percentage Rate (APR) is the annual interest rate charged on outstanding credit card balances. It is a crucial factor influencing the minimum payment calculation. A higher APR translates to higher interest charges, leading to a larger minimum payment. Understanding your APR is paramount for making informed financial decisions.

FAQ Section: Answering Common Questions About Minimum Credit Card Payments

What is the typical minimum payment percentage? While it varies, 1% to 3% of the outstanding balance is common, but this isn't a guarantee.

How is the minimum payment calculated? Usually, it's a percentage of your balance plus accrued interest and any fees. The specific calculation is outlined in your credit card agreement.

What happens if I only pay the minimum? You'll pay more interest overall, extending the repayment period and increasing the total cost.

Can my minimum payment change? Yes, it can fluctuate based on your balance, the interest charged, and the credit card company's policies.

What if I miss a minimum payment? You'll likely incur late fees, and it will negatively affect your credit score.

Practical Tips: Maximizing the Benefits of Responsible Credit Card Repayment

-

Understand Your Credit Card Agreement: Review the terms and conditions to understand the minimum payment calculation and APR.

-

Budget Effectively: Create a budget that allows for more than the minimum payment to accelerate debt reduction.

-

Explore Debt Consolidation: Consider consolidating high-interest debts into a lower-interest loan or credit card.

-

Pay More Than the Minimum: Even a small increase in your payment can significantly shorten the repayment period and reduce total interest paid.

-

Monitor Your Credit Report: Regularly check your credit report to ensure accuracy and identify any potential issues.

-

Seek Professional Help: If you're struggling to manage credit card debt, consult a financial advisor for personalized guidance.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding the minimum payment on a $5,000 credit card balance is crucial for managing debt effectively. While the minimum payment might appear manageable at first glance, paying only this amount can lead to significant long-term costs. By understanding the factors influencing minimum payment calculations, such as interest rates and fees, and by implementing responsible repayment strategies, individuals can avoid the pitfalls of accumulating unnecessary debt and maintain a healthy financial standing. Proactive financial management is key to long-term financial success.

Latest Posts

Latest Posts

-

Minimum Payment On Loan

Apr 05, 2025

-

How Is Minimum Monthly Credit Card Payment Calculated

Apr 05, 2025

-

How Does Chase Credit Card Calculate Minimum Payment

Apr 05, 2025

-

How Does Chase Calculate Minimum Payment

Apr 05, 2025

-

Whats The Minimum Payment For Ssi

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about What Is The Minimum Payment On A $5 000 Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.