What Is The Minimum Monthly Payment On 2000 Credit Card

adminse

Apr 05, 2025 · 7 min read

Table of Contents

Decoding the Minimum Payment on a $2,000 Credit Card: A Comprehensive Guide

What if your minimum credit card payment is obscuring a path to financial freedom? Understanding the true cost of minimum payments on a $2,000 balance can dramatically alter your financial strategy.

Editor’s Note: This article provides an in-depth analysis of minimum credit card payments on a $2,000 balance, updated for 2024. It's designed to help you understand the implications and develop a responsible repayment plan.

Why Minimum Payments Matter: The Hidden Costs of Convenience

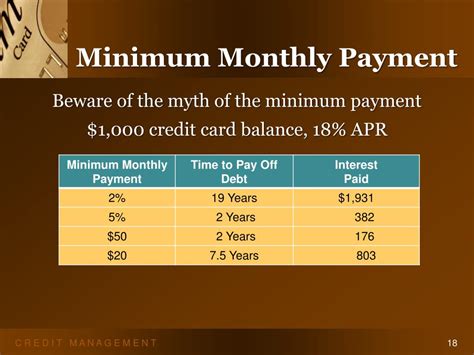

Many cardholders focus solely on making the minimum payment, believing it’s a simple way to manage debt. However, this approach often masks a significant financial burden. The minimum payment, typically a small percentage of the outstanding balance (often 1-3%), barely covers the accrued interest. This means that with each minimum payment on a $2,000 credit card balance, you're primarily paying interest, extending the repayment period considerably and ultimately costing you far more in the long run. Ignoring the implications of minimum payments can lead to a cycle of debt that's difficult to break, impacting your credit score and overall financial health. Understanding the factors that determine your minimum payment and the long-term consequences is crucial for responsible credit management.

Overview: What This Article Covers

This comprehensive guide explores the intricacies of minimum credit card payments on a $2,000 balance. We will examine:

- The calculation of minimum payments.

- The impact of interest rates on repayment time and total cost.

- Strategies for accelerating debt repayment.

- The effect of minimum payments on your credit score.

- Alternatives to minimum payment strategies.

- The role of credit utilization in credit scoring.

- How to negotiate lower interest rates.

- The importance of budgeting and financial planning.

- The consequences of consistently making only minimum payments.

- Understanding the terms and conditions of your credit card agreement.

The Research and Effort Behind the Insights

This article is based on extensive research, drawing upon industry reports, financial regulations, and expert opinions from credit counseling agencies and financial analysts. We utilize real-world examples and illustrative calculations to ensure clarity and provide practical guidance for managing credit card debt effectively.

Key Takeaways:

- Variable Minimum Payments: The minimum payment isn't a fixed amount; it fluctuates based on your balance and credit card agreement.

- Interest Accumulation: Making only the minimum payment significantly increases the total interest paid over the life of the debt.

- Extended Repayment: Minimum payments prolong the repayment period, potentially for years.

- Impact on Credit Score: While making any payment avoids late payment penalties, consistently paying only the minimum can negatively affect your credit score due to high credit utilization.

- Strategic Repayment: Aggressive repayment strategies, like the debt avalanche or snowball method, can save substantial amounts of money and time.

Smooth Transition to the Core Discussion

Now that we understand the importance of comprehending minimum payments, let's delve into the specifics of calculating minimum payments and analyzing their long-term implications on a $2,000 balance.

Exploring the Key Aspects of Minimum Payments on a $2,000 Credit Card

1. Definition and Core Concepts:

The minimum payment is the smallest amount a credit card company requires you to pay each month to avoid late payment fees. This amount is usually a percentage of your outstanding balance (often between 1% and 3%) or a fixed minimum amount (typically $25-$35), whichever is greater. The exact calculation varies depending on the terms and conditions specified in your credit card agreement.

2. Applications Across Industries:

While the concept of minimum payments is consistent across credit card issuers, the specific calculation method and the minimum payment amount can vary. Some credit card companies may offer options to increase your minimum payment, which can expedite the repayment process.

3. Challenges and Solutions:

The biggest challenge associated with minimum payments is the significant accumulation of interest. The solution lies in developing a robust repayment strategy that involves paying more than the minimum each month.

4. Impact on Innovation:

The credit card industry is constantly evolving, with new products and features designed to help consumers manage their debt. However, the fundamental principle of minimum payments remains consistent, highlighting the importance of understanding its implications.

Closing Insights: Summarizing the Core Discussion

Making only the minimum payment on a $2,000 credit card can trap you in a cycle of debt. The seemingly small minimum payment masks a significant financial burden due to accumulating interest, extended repayment periods, and potential negative impacts on your credit score. Understanding these implications is crucial for managing your finances responsibly.

Exploring the Connection Between Interest Rates and Minimum Payments

The interest rate on your credit card dramatically impacts the minimum payment calculation and the overall cost of repayment. A higher interest rate means a larger portion of your minimum payment goes towards interest, leaving a smaller amount to reduce the principal balance.

Key Factors to Consider:

- Roles and Real-World Examples: Consider two scenarios: one with a 15% APR and another with a 25% APR. With a $2,000 balance, the interest accrued each month will be significantly higher with the 25% APR, resulting in a larger minimum payment and a much longer repayment period.

- Risks and Mitigations: The risk of high interest rates is prolonged debt and increased overall cost. Mitigation strategies involve seeking lower interest rates through balance transfers or negotiating with your credit card company.

- Impact and Implications: High interest rates lead to substantial additional costs, potentially delaying your ability to achieve financial goals. This highlights the importance of comparing interest rates before choosing a credit card and diligently managing your credit card debt.

Conclusion: Reinforcing the Connection

The relationship between interest rates and minimum payments is undeniable. High interest rates significantly increase the cost and duration of repayment, emphasizing the need for proactive debt management strategies.

Further Analysis: Examining Interest Calculation in Greater Detail

Credit card interest is typically calculated using the average daily balance method. This means the interest is calculated on the average balance outstanding throughout the billing cycle. Understanding this calculation is vital to accurately assess the true cost of minimum payments.

FAQ Section: Answering Common Questions About Minimum Payments

-

What is the typical minimum payment percentage on a credit card? It generally ranges from 1% to 3% of your outstanding balance, but it can be higher or lower depending on your credit card agreement.

-

How is the minimum payment calculated? Most issuers calculate it as a percentage of the balance or a fixed minimum, whichever is greater.

-

Does making only the minimum payment hurt my credit score? While it won't directly cause a late payment penalty if made on time, consistently making only the minimum payment can negatively impact your credit score due to high credit utilization.

-

How long will it take to pay off a $2,000 credit card balance making only minimum payments? This depends heavily on your interest rate and the minimum payment amount, but it could take several years, sometimes even a decade or more.

-

What are the alternatives to making only the minimum payment? Consider debt avalanche or snowball methods, balance transfers to lower interest cards, or debt consolidation loans.

Practical Tips: Maximizing the Benefits of Strategic Repayment

-

Understand the Basics: Know your interest rate, minimum payment, and total balance.

-

Create a Budget: Track your income and expenses to identify extra funds for debt repayment.

-

Choose a Repayment Method: Select a strategy (debt avalanche or snowball) that aligns with your financial goals and preferences.

-

Automate Payments: Set up automatic payments to ensure you consistently pay more than the minimum.

-

Monitor Progress: Regularly review your progress to stay motivated and adjust your strategy if needed.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding the implications of minimum payments on a $2,000 credit card balance is critical for achieving financial stability. While minimum payments provide a safety net, relying solely on them can lead to years of debt and significantly increased costs. By proactively developing a repayment strategy and utilizing resources like budgeting tools and debt consolidation options, you can break free from the cycle of minimum payments and pave the way for a more secure financial future. Remember, informed financial decisions today directly impact your financial well-being tomorrow.

Latest Posts

Latest Posts

-

Money Management Dalam Trading

Apr 06, 2025

-

Money Management Mql4

Apr 06, 2025

-

Money Management Xauusd

Apr 06, 2025

-

Money Management Problem

Apr 06, 2025

-

Tools To Manage Finances

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about What Is The Minimum Monthly Payment On 2000 Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.