What Is The Minimum Irs Payment Plan

adminse

Apr 06, 2025 · 9 min read

Table of Contents

Decoding the IRS Minimum Payment Plan: A Comprehensive Guide

What if navigating IRS tax debt felt less daunting and more manageable? The IRS minimum payment plan offers a lifeline for taxpayers struggling to pay their tax liabilities, providing a structured pathway toward debt resolution.

Editor’s Note: This article on IRS minimum payment plans was updated today to reflect the latest IRS guidelines and procedures. We aim to provide clear, accurate, and up-to-date information to help taxpayers understand their options and navigate the process effectively.

Why the IRS Minimum Payment Plan Matters:

Facing a significant tax bill can be overwhelming. Many taxpayers, however, are unaware of the various payment options available through the IRS. The minimum payment plan, often called an installment agreement, provides a crucial safety net. It allows individuals and businesses to pay off their tax debt in manageable installments over a period of time, preventing penalties and further complications. Understanding this option is essential for maintaining financial stability and avoiding severe consequences, like wage garnishment or asset seizure. This plan isn't just about avoiding immediate penalties; it's about regaining financial control and restoring a positive relationship with the IRS.

Overview: What This Article Covers:

This comprehensive guide explores the intricacies of the IRS minimum payment plan. We'll delve into eligibility requirements, the application process, calculating minimum payments, understanding potential penalties, and exploring alternative solutions. Readers will gain a clear understanding of their rights and responsibilities, empowering them to make informed decisions about their tax debt.

The Research and Effort Behind the Insights:

This article draws upon extensive research, including the official IRS website, publications, and relevant legal interpretations. We've meticulously reviewed IRS guidelines and procedures to ensure the accuracy and reliability of the information presented. Our goal is to provide a clear and accessible resource for taxpayers seeking to navigate the complex landscape of IRS payment plans.

Key Takeaways:

- Definition and Core Concepts: A clear explanation of the IRS installment agreement and its core principles.

- Eligibility Requirements: A detailed outline of the criteria taxpayers must meet to qualify.

- Application Process: A step-by-step guide on how to apply for an installment agreement.

- Calculating Minimum Payments: Understanding how the IRS calculates minimum monthly payments.

- Penalties and Interest: Clarifying the implications of late payments and outstanding interest.

- Alternative Solutions: Exploring other IRS payment options, such as Offer in Compromise (OIC).

- Common Mistakes to Avoid: Highlighting frequent errors taxpayers make during the application process.

Smooth Transition to the Core Discussion:

Now that we've established the importance of understanding IRS minimum payment plans, let's explore the specifics of this crucial program.

Exploring the Key Aspects of the IRS Minimum Payment Plan:

1. Definition and Core Concepts:

An IRS installment agreement, or payment plan, is a formal arrangement with the IRS allowing taxpayers to pay their tax debt in monthly installments over a set period. The "minimum" payment refers to the lowest amount the IRS will accept each month. This amount is not fixed but depends on several factors, including the total tax debt, the taxpayer's ability to pay, and the length of the agreement. The IRS offers short-term payment plans (up to 180 days) and long-term payment plans (generally up to 72 months). The longer the payment plan, the stricter the eligibility requirements.

2. Eligibility Requirements:

To be eligible for an installment agreement, taxpayers generally must meet the following criteria:

- Owe a combined total of under $50,000: This includes taxes, penalties, and interest.

- Have filed all required tax returns: Unfiled returns are a significant barrier to approval.

- Be current on their tax filing requirements: This means filing all required returns for the current year and previous years.

- Demonstrate the ability to pay: The IRS will assess the taxpayer's income and expenses to determine their ability to make regular payments. This often involves providing financial documentation.

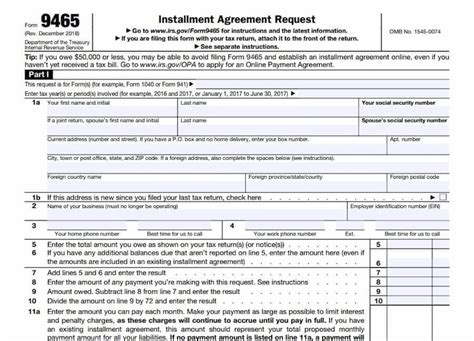

3. Application Process:

Applying for an installment agreement is primarily done online through the IRS's Online Payment Agreement (OPA) system. However, taxpayers can also apply via mail using Form 9465, Installment Agreement Request. The OPA system offers a quicker and more efficient process. Here's a general overview:

- Gather necessary information: This includes tax information (notice or CP letter), bank statements, pay stubs, and other financial documents.

- Complete the application: The online application requires entering relevant personal and financial information. Accuracy is crucial.

- Submit the application: Once completed, submit the application online or via mail.

- IRS Review and Approval: The IRS will review the application, often within a few weeks.

- Payment Schedule: Upon approval, the IRS will provide a payment schedule outlining monthly payments and due dates.

4. Calculating Minimum Payments:

The IRS doesn't have a fixed formula for calculating the minimum monthly payment. It's based on a combination of factors, primarily the taxpayer's ability to pay. Generally, the minimum payment will be enough to cover the total tax liability within the chosen payment plan period (e.g., 72 months). The IRS may consider several factors, including:

- Total tax liability: The overall amount of tax owed, including penalties and interest.

- Income and expenses: A thorough review of the taxpayer's financial situation to determine affordability.

- Assets and liabilities: An assessment of the taxpayer's overall financial position.

- Chosen payment plan length: Longer payment plans typically result in lower monthly payments.

5. Penalties and Interest:

While an installment agreement helps avoid further penalties for non-payment, taxpayers are still responsible for paying interest on the outstanding tax debt. Interest accrues daily until the debt is fully paid. Failure to make timely payments under the installment agreement will result in penalties and potential termination of the agreement. The IRS may take more aggressive collection actions, such as wage garnishment or levy of assets.

6. Alternative Solutions:

The installment agreement isn't the only option for resolving IRS tax debt. Other alternatives include:

- Offer in Compromise (OIC): An OIC allows taxpayers to settle their tax debt for a lower amount than what is owed. This is usually considered when the taxpayer can't afford to pay the full amount. Eligibility for an OIC is stringent and requires demonstrating significant financial hardship.

- Short-Term Payment Plan: This allows for a shorter payment period, typically up to 180 days, to pay the tax debt in full. This is a suitable option for those who expect to have the funds soon.

7. Common Mistakes to Avoid:

- Inaccurate Information: Providing false or misleading information on the application is a serious offense.

- Missed Payments: Consistent timely payments are essential to maintaining the agreement.

- Ignoring IRS Communication: Respond promptly to all IRS communication regarding the payment plan.

- Failing to Update Financial Information: Notify the IRS of any significant changes in your financial circumstances.

Exploring the Connection Between Credit Score and IRS Minimum Payment Plan:

The relationship between a taxpayer's credit score and their eligibility for an IRS minimum payment plan is indirect but significant. While the IRS doesn't explicitly require a minimum credit score for approval, a strong credit history often reflects financial responsibility, increasing the likelihood of approval. Conversely, a poor credit score might indicate a higher risk to the IRS, potentially leading to stricter scrutiny and a higher bar for approval.

Key Factors to Consider:

- Roles and Real-World Examples: Taxpayers with excellent credit scores often find the application process smoother and more likely to be approved for longer-term payment plans. Conversely, individuals with poor credit may be limited to shorter payment plans or may need to provide more comprehensive financial documentation to demonstrate their ability to pay.

- Risks and Mitigations: A low credit score doesn't automatically disqualify you. By providing detailed financial documentation, demonstrating a consistent income, and outlining a realistic payment plan, taxpayers can mitigate the risks associated with a low credit score.

- Impact and Implications: A rejected installment agreement due to poor credit can lead to more aggressive collection actions by the IRS, negatively impacting credit scores further.

Conclusion: Reinforcing the Connection

The connection between credit score and IRS minimum payment plan highlights the importance of maintaining good financial health. While a low credit score doesn’t preclude eligibility, it emphasizes the need for meticulous documentation and a realistic payment plan to secure approval and successfully resolve tax debt.

Further Analysis: Examining Credit Repair Strategies

Improving credit scores before applying for an installment agreement is advisable. Strategies include paying down existing debt, paying bills on time, and disputing any inaccuracies on credit reports. These steps enhance the likelihood of approval and potentially secure more favorable terms.

FAQ Section: Answering Common Questions About the IRS Minimum Payment Plan:

Q: What happens if I miss a payment on my installment agreement?

A: Missing a payment will result in penalties and could lead to termination of the agreement. Contact the IRS immediately if you anticipate difficulty making a payment to explore possible solutions.

Q: How long can I have an installment agreement?

A: Long-term installment agreements typically last up to 72 months. Shorter-term plans are also available.

Q: Can I modify my installment agreement if my financial situation changes?

A: Yes, you can request a modification to your payment agreement if your financial circumstances change significantly. You'll need to contact the IRS and provide updated financial documentation.

Q: What if I can’t afford the minimum payment?

A: If you can't afford the minimum payment, explore alternative options like an Offer in Compromise (OIC) or contact a tax professional for guidance.

Practical Tips: Maximizing the Benefits of the IRS Minimum Payment Plan:

- Act promptly: Don't delay applying for an installment agreement if you’re facing tax debt.

- Be accurate: Ensure all information provided on the application is accurate and complete.

- Communicate with the IRS: Maintain open communication with the IRS throughout the process.

- Seek professional help: Consider consulting a tax professional for assistance.

Final Conclusion: Wrapping Up with Lasting Insights:

The IRS minimum payment plan offers a critical lifeline for taxpayers struggling with tax debt. By understanding the eligibility criteria, application process, and potential implications, individuals and businesses can navigate this process effectively and regain control of their financial situation. Remember, proactive planning and open communication with the IRS are vital to successfully resolving tax debt and avoiding severe consequences. Don't hesitate to seek professional help when needed. Taking a proactive approach and understanding your options can significantly ease the burden of tax debt and pave the way for financial recovery.

Latest Posts

Latest Posts

-

Where Can I Purchase A Money Order With My Credit Card

Apr 07, 2025

-

Where Can I Buy A Money Order With My Credit Card

Apr 07, 2025

-

Where Can I Get A Money Order Using Credit Card

Apr 07, 2025

-

Where Can I Make A Money Order With Credit Card

Apr 07, 2025

-

Where Can I Get A Money Order With A Credit Card Near Me

Apr 07, 2025

Related Post

Thank you for visiting our website which covers about What Is The Minimum Irs Payment Plan . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.