What Is The Grace Period On A Mortgage

adminse

Apr 02, 2025 · 8 min read

Table of Contents

What if missing a single mortgage payment could have unexpected consequences? Understanding the grace period on your mortgage is crucial for avoiding late fees and potential foreclosure.

Editor’s Note: This article on mortgage grace periods was published today, providing up-to-date information and insights for homeowners and prospective buyers navigating the complexities of mortgage payments.

Why Mortgage Grace Periods Matter: Avoiding Financial Distress

A mortgage grace period is the timeframe a lender allows after a scheduled payment is due before officially marking it as late. While the exact length varies significantly depending on the lender, the loan type, and even the individual contract, understanding its implications is paramount for responsible homeownership. Failing to grasp the grace period can lead to unnecessary late fees, damage to credit scores, and in extreme cases, foreclosure proceedings. This understanding is crucial for both budgeting purposes and maintaining a healthy financial standing. The potential financial distress associated with late payments highlights the critical need for homeowners to proactively manage their mortgage accounts and be aware of the specific terms of their loan agreements.

Overview: What This Article Covers

This article delves into the specifics of mortgage grace periods, exploring their variations, the consequences of missed payments, strategies for avoiding late payments, and the importance of communication with lenders. Readers will gain actionable insights into protecting their financial well-being and ensuring responsible homeownership.

The Research and Effort Behind the Insights

This article is the result of comprehensive research, drawing upon information from reputable financial institutions, consumer protection agencies, and legal resources specializing in mortgage lending. The information presented is intended to provide accurate and up-to-date information to assist homeowners in understanding their mortgage agreements and managing their finances responsibly.

Key Takeaways:

- Definition and Core Concepts: A clear definition of mortgage grace periods and the factors influencing their duration.

- Variations in Grace Periods: An examination of the differences between lenders and loan types.

- Consequences of Late Payments: A detailed breakdown of the financial penalties and credit score impacts.

- Strategies for Avoiding Late Payments: Practical tips and advice on effective financial planning and proactive mortgage management.

- Communication with Lenders: The importance of open communication with lenders regarding potential payment difficulties.

- Understanding Your Mortgage Contract: Emphasis on reviewing and understanding the specific terms of the loan agreement.

Smooth Transition to the Core Discussion

With a clear understanding of the importance of mortgage grace periods, let's delve deeper into their nuances and practical implications for homeowners.

Exploring the Key Aspects of Mortgage Grace Periods

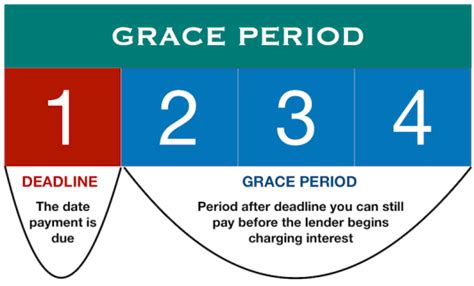

Definition and Core Concepts: A mortgage grace period is the brief window of time following the due date of a mortgage payment during which the lender does not yet consider the payment late. This period typically ranges from a few days to a couple of weeks, but it's crucial to note that this is not a universal standard. The grace period is not a given right but rather a provision typically included in the mortgage loan agreement. During this period, no late fees are usually assessed. However, interest still accrues on the outstanding principal balance.

Variations in Grace Periods: There's no single, universally mandated grace period for all mortgages. The length of the grace period can vary substantially depending on several factors:

- Lender Policies: Individual lenders set their own grace period policies. Some may offer a generous period, while others might have a shorter, more stringent timeframe.

- Loan Type: Different types of mortgages may have varying grace periods. For instance, a conventional loan might have a different grace period than an FHA or VA loan.

- Specific Loan Agreement: The terms of the individual mortgage agreement are paramount. The loan documents will explicitly state the grace period length.

Consequences of Late Payments: Once the grace period expires, the payment is considered delinquent. This triggers several significant consequences:

- Late Fees: Lenders impose late fees, which can range from a small percentage of the missed payment to a fixed dollar amount. These fees can quickly add up and significantly impact the overall cost of the mortgage.

- Negative Impact on Credit Score: A late payment is reported to the credit bureaus, which can severely damage the homeowner's credit score. A lower credit score makes it harder to secure future loans, and it can result in higher interest rates on credit cards, auto loans, and other forms of credit.

- Potential Foreclosure: Repeated or prolonged late payments can lead to serious consequences, eventually culminating in foreclosure proceedings initiated by the lender to recover the outstanding debt. This can result in the loss of the home.

Strategies for Avoiding Late Payments:

- Automatic Payments: Setting up automatic payments from a checking or savings account is the most effective method for ensuring on-time payments. This eliminates the risk of forgetting or missing the due date.

- Budgeting: Creating a detailed budget that accurately reflects monthly expenses and income is crucial for allocating sufficient funds to cover the mortgage payment.

- Payment Reminders: Utilizing online banking tools, calendar alerts, or mobile apps to receive payment reminders can help prevent accidental late payments.

- Emergency Fund: Maintaining an emergency fund can provide a financial cushion to cover unexpected expenses that could otherwise jeopardize on-time mortgage payments.

- Communication with Lender: If facing financial difficulties, proactively contacting the lender to discuss potential options is vital. Many lenders are willing to work with borrowers experiencing temporary hardships, such as forbearance or loan modification programs.

Communication with Lenders: Open communication is key. If facing any challenges that might affect timely payments, contact the lender immediately. Explain the situation honestly and explore potential options such as forbearance or a loan modification. Proactive communication often prevents the escalation of late payments to more severe consequences.

Understanding Your Mortgage Contract: The most reliable source of information about your specific grace period is your mortgage contract. Carefully review the document to ascertain the exact length of the grace period, and any associated late payment penalties.

Exploring the Connection Between Prepayment Penalties and Grace Periods

The existence of a grace period doesn't negate the potential implications of prepayment penalties. While a grace period addresses late payments, prepayment penalties pertain to paying off the loan early. These penalties are outlined in the mortgage contract and are not directly related to the grace period for late payments.

Key Factors to Consider:

- Roles and Real-World Examples: A homeowner might miss a payment due to an unexpected job loss, but even then, understanding the grace period allows them to rectify the situation before incurring severe penalties. Conversely, a homeowner diligently paying their mortgage early doesn't have implications related to the grace period for late payments unless they deliberately miss a scheduled payment.

- Risks and Mitigations: The risk of missing a payment and entering the late payment phase increases if a homeowner isn't proactively managing their finances. Mitigation involves careful budgeting, automated payments, and maintaining an emergency fund.

- Impact and Implications: Missing a payment after the grace period expires has a significantly negative impact on credit scores and could lead to increased financial burdens from late fees. Conversely, prepayment (if allowed without penalties) can lead to long-term savings on interest payments.

Conclusion: Reinforcing the Connection

The relationship between prepayment penalties and grace periods is largely independent. While a grace period deals with late payments, prepayment penalties are concerned with early loan payoff. Understanding both aspects is crucial for sound financial management.

Further Analysis: Examining Prepayment Penalties in Greater Detail

Prepayment penalties are designed to protect lenders from the loss of potential interest income when borrowers pay off their mortgages early. These penalties, generally a percentage of the remaining loan balance, vary widely depending on the loan type and lender. Some mortgages, especially those with lower interest rates, might have significant prepayment penalties, whereas others might be penalty-free or have much lower penalties. Always thoroughly review your mortgage agreement to fully understand any potential prepayment penalties.

FAQ Section: Answering Common Questions About Mortgage Grace Periods

What is a mortgage grace period? A mortgage grace period is the short period after your mortgage payment due date before your lender considers the payment late.

How long is a typical mortgage grace period? The length varies by lender and loan type; it's usually a few days to a couple of weeks. Check your mortgage documents for the exact period.

What happens if I miss a payment after the grace period? Late fees will be applied, and the late payment will be reported to credit bureaus, negatively affecting your credit score. Repeated late payments can lead to foreclosure.

Can I negotiate with my lender if I'm facing payment difficulties? Yes, it's crucial to contact your lender immediately if facing financial difficulties to discuss options such as forbearance or loan modification.

What is forbearance? Forbearance is a temporary suspension or reduction of mortgage payments, typically granted due to extenuating circumstances.

What is loan modification? Loan modification involves changing the terms of your mortgage, such as lowering the interest rate or extending the loan term, to make payments more manageable.

Practical Tips: Maximizing the Benefits of Understanding Your Grace Period

- Review Your Mortgage Documents: Familiarize yourself with the specifics of your loan agreement, including the grace period length and late payment penalties.

- Set Up Automatic Payments: Automate your mortgage payments to ensure timely payments and eliminate the risk of forgetting.

- Budget Carefully: Develop a realistic budget that accounts for all expenses, ensuring sufficient funds for your mortgage payment.

- Utilize Payment Reminders: Employ online banking tools, calendar alerts, or mobile apps to receive payment reminders.

- Build an Emergency Fund: Save enough money to cover unexpected expenses that could otherwise jeopardize your mortgage payments.

- Communicate Proactively: Contact your lender immediately if you anticipate any difficulties in making your mortgage payments.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding your mortgage grace period is crucial for responsible homeownership. By proactively managing finances, setting up automatic payments, and communicating openly with your lender, you can minimize the risks associated with late payments and safeguard your financial future. Remember that proactive management and clear communication are your best tools for navigating the complexities of mortgage payments.

Latest Posts

Latest Posts

-

Liquidity Pool Crypto Adalah

Apr 04, 2025

-

What Is Liquidity Pool In Blockchain

Apr 04, 2025

-

What Is A Liquidity Pool In Cryptocurrency

Apr 04, 2025

-

Quickbooks Late Fees

Apr 04, 2025

-

How To Set Up Automatic Late Fees In Quickbooks Desktop

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about What Is The Grace Period On A Mortgage . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.