What Is Statement Date In Credit Card Union Bank

adminse

Apr 04, 2025 · 7 min read

Table of Contents

Unveiling the Mystery: Understanding Statement Dates in Credit Union Bank Cards

What if your financial planning hinged on knowing exactly when your credit union bank card statement arrives? Mastering the intricacies of statement dates empowers you to manage your finances with precision and avoid costly late fees.

Editor’s Note: This article on statement dates for credit union bank cards was published today, providing you with the most up-to-date information available to effectively manage your credit union account.

Why Statement Dates Matter: More Than Just a Number

Understanding your credit union bank card's statement date is crucial for several reasons. It's not simply a date; it's a keystone in effective financial management. Knowing your statement date allows for:

- Precise Budgeting: You can accurately track spending and allocate funds for the upcoming payment.

- Avoiding Late Fees: Missing a payment can lead to significant penalties. Knowing the statement date helps you schedule timely payments.

- Credit Score Management: Late payments negatively impact your credit score. Consistent on-time payments, facilitated by understanding statement dates, are essential for maintaining a healthy credit score.

- Debt Management: Accurate tracking of charges, facilitated by regular statement review, assists in effectively managing debt and avoiding overspending.

- Fraud Detection: Regularly reviewing your statement allows for prompt identification of any fraudulent transactions.

Overview: What This Article Covers

This article comprehensively explores credit union bank card statement dates, encompassing their determination, variations, access methods, and importance in overall financial health. We will delve into common questions, practical tips for managing payments, and strategies for maximizing the benefits of understanding this crucial aspect of credit card management.

The Research and Effort Behind the Insights

The information presented here is compiled from a variety of sources, including official statements from major credit unions, financial industry reports, and expert opinions on consumer credit. We have meticulously examined various credit union policies and practices to provide an accurate and holistic understanding of statement date processes.

Key Takeaways:

- Definition of Statement Date: The precise date your credit union generates your monthly summary of transactions.

- Factors Influencing Statement Dates: Understanding how various factors contribute to the determination of your statement date.

- Accessing Your Statement: Various methods for reviewing your statement online, by mail, or via mobile app.

- Payment Due Date: The importance of differentiating between the statement date and the payment due date.

- Proactive Management Strategies: Effective strategies to ensure timely payments and prevent late fees.

Smooth Transition to the Core Discussion:

Now that we've established the significance of understanding statement dates, let's explore the intricacies of how they are determined and how you can utilize this knowledge for your financial benefit.

Exploring the Key Aspects of Credit Union Bank Card Statement Dates

1. Definition and Core Concepts:

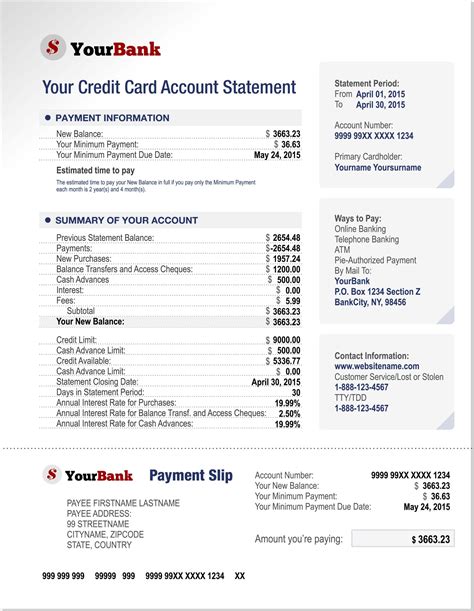

The statement date is the date your credit union generates your monthly credit card statement. This statement summarizes all transactions made during the billing cycle, including purchases, payments, fees, and interest charges. It is not the due date for your payment.

2. Factors Influencing Statement Dates:

Several factors influence the statement date assigned to your credit union bank card:

- Account Opening Date: The initial statement date is often linked to your account opening date.

- Credit Union Policy: Each credit union sets its own policies regarding statement generation, which can lead to variations.

- System Processing: The credit union's internal systems and processing schedules influence the timing of statement generation.

- Billing Cycle: The statement date marks the end of a specific billing cycle, usually a month-long period.

3. Accessing Your Statement:

Most credit unions offer multiple ways to access your statement:

- Online Access: Through your online banking portal, you can usually access your statement as a PDF download.

- Mobile App: Many credit unions provide mobile banking apps allowing statement viewing on your smartphone or tablet.

- Mail Delivery: Some members prefer to receive paper statements mailed to their address. This often requires opting-in or not opting-out of e-statements.

4. Payment Due Date vs. Statement Date:

It’s crucial to understand the difference. The statement date reflects when the statement is generated; the payment due date indicates when your payment must be received by the credit union to avoid late fees. The payment due date is usually a specific number of days after the statement date (e.g., 21 or 25 days). Always check your statement for the precise payment due date.

5. Impact on Financial Health:

Knowing your statement date is fundamental to maintaining healthy finances. It empowers you to:

- Budget effectively: Track spending and plan for upcoming payments.

- Avoid late fees: Pay on time to avoid penalties.

- Maintain a good credit score: Consistent on-time payments contribute to a strong credit history.

Closing Insights: Summarizing the Core Discussion

Understanding your credit union bank card statement date is not merely about receiving a monthly summary; it's a critical element of responsible financial management. By understanding the various factors that influence the date and the various ways to access your statement, you can maintain a proactive approach to your finances, ultimately improving your overall financial well-being.

Exploring the Connection Between Billing Cycle Length and Statement Date

The billing cycle length directly impacts your statement date. A typical billing cycle is 30 days, but this can vary. Understanding this connection is crucial for accurate financial planning.

Key Factors to Consider:

- Roles and Real-World Examples: A shorter billing cycle (e.g., 28 days) will result in more frequent statement dates throughout the year. Conversely, a longer cycle might mean fewer statements. This can impact budgeting if you are not accustomed to the rhythm.

- Risks and Mitigations: An unexpected change in your billing cycle can disrupt your financial planning. Contacting your credit union promptly for clarification is key.

- Impact and Implications: Inconsistent billing cycles can make budgeting more challenging. Understanding the cycle length enables more precise financial planning.

Conclusion: Reinforcing the Connection

The interplay between billing cycle length and statement date emphasizes the importance of staying informed about your credit union’s policies. By actively monitoring your billing cycle and understanding its effect on your statement date, you can create a more robust and effective financial strategy.

Further Analysis: Examining Billing Cycle Length in Greater Detail

The billing cycle length is determined by your credit union and is usually consistent unless a change is communicated. Factors influencing length can include system updates or internal processes. Regular review of your statements helps detect any anomalies.

FAQ Section: Answering Common Questions About Statement Dates

Q: What if I miss my payment due date? A: Late payment fees will apply, and this can negatively impact your credit score. Contact your credit union immediately to discuss payment options.

Q: How can I change my statement delivery method? A: Check your credit union's website or mobile app for options to switch between paper and electronic statements.

Q: My statement date has changed; why? A: Contact your credit union to determine the cause. There might be a system update or a policy change.

Q: Where can I find my payment due date? A: The payment due date is clearly stated on your credit card statement.

Practical Tips: Maximizing the Benefits of Understanding Statement Dates

- Mark your calendar: Note the statement date and payment due date on your calendar or digital planner.

- Set up automatic payments: Automate payments to avoid late fees.

- Review your statement meticulously: Check for errors or fraudulent activity.

- Contact your credit union: Don't hesitate to contact your credit union if you have any questions or concerns about your statement date.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding your credit union bank card statement date is a crucial step towards achieving financial literacy and stability. By utilizing the information and strategies presented in this article, you can confidently manage your finances, avoid costly mistakes, and maintain a healthy credit profile. Remember that proactive engagement with your credit union and diligent monitoring of your account are key to responsible credit card management.

Latest Posts

Latest Posts

-

Minimum Payment On Loan

Apr 05, 2025

-

How Is Minimum Monthly Credit Card Payment Calculated

Apr 05, 2025

-

How Does Chase Credit Card Calculate Minimum Payment

Apr 05, 2025

-

How Does Chase Calculate Minimum Payment

Apr 05, 2025

-

Whats The Minimum Payment For Ssi

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about What Is Statement Date In Credit Card Union Bank . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.