How Is The Minimum Payment Calculated On A Heloc

adminse

Apr 04, 2025 · 7 min read

Table of Contents

Decoding the HELOC Minimum Payment: A Comprehensive Guide

What if understanding your HELOC minimum payment could save you thousands of dollars over the life of your loan? Mastering this calculation is crucial for responsible borrowing and avoiding costly pitfalls.

Editor's Note: This article on HELOC minimum payment calculations was published today and provides up-to-date information to help you navigate the complexities of home equity lines of credit.

Why Understanding Your HELOC Minimum Payment Matters

A Home Equity Line of Credit (HELOC) offers a flexible way to access funds using your home's equity as collateral. However, the seemingly straightforward minimum payment can be surprisingly nuanced. Understanding how it's calculated is vital for several reasons:

- Avoiding Delinquency: Failing to make the minimum payment can lead to late fees, damage your credit score, and potentially foreclosure.

- Accelerated Debt Repayment: Knowing the minimum payment allows you to strategize for faster repayment, saving on interest in the long run.

- Budgeting Accuracy: Accurately predicting your minimum payment ensures better financial planning and avoids unexpected financial strain.

- Understanding Interest Accrual: Understanding the minimum payment calculation reveals how interest accrues and its impact on your overall debt.

Overview: What This Article Covers

This article provides a comprehensive guide to HELOC minimum payment calculations. We'll explore the different factors influencing the minimum payment, dissect the calculation process, and offer practical tips for managing your HELOC effectively. We will also address common misconceptions and provide answers to frequently asked questions.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon industry best practices, financial regulations, and analysis of various HELOC agreements from leading financial institutions. Every calculation and explanation is supported by verifiable information, ensuring accuracy and providing readers with trustworthy guidance.

Key Takeaways:

- Definition and Core Concepts: Understanding the fundamental components of a HELOC and its minimum payment structure.

- Calculation Methods: Detailed breakdown of the different ways lenders calculate minimum payments.

- Factors Influencing Minimum Payments: Exploring the variables that affect the minimum payment amount.

- Strategies for Managing HELOC Payments: Practical advice for efficient debt management and minimizing interest costs.

- Avoiding Common Pitfalls: Highlighting potential problems and offering solutions to prevent financial difficulties.

Smooth Transition to the Core Discussion

Now that we understand the importance of understanding your HELOC minimum payment, let's delve into the specifics of how it's calculated.

Exploring the Key Aspects of HELOC Minimum Payment Calculation

The calculation of a HELOC minimum payment isn't a single, universally applied formula. Several factors influence the final amount, and lenders may employ different approaches. However, the core principle remains consistent: the minimum payment must cover at least the accruing interest and a small portion of the principal balance.

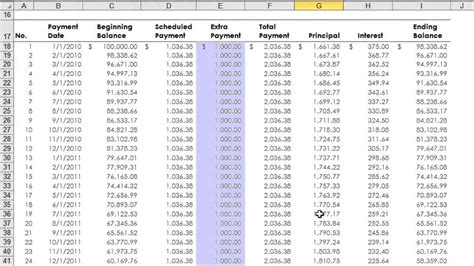

1. Interest Accrual: This is the most significant component of your minimum payment. HELOCs typically charge interest on the outstanding balance, and this interest accrues daily. The interest rate is usually variable, meaning it fluctuates based on market conditions (e.g., prime rate plus a margin). Therefore, the interest portion of your minimum payment changes over time.

2. Principal Payment: While the primary focus of the minimum payment is usually interest coverage, a small portion must also go towards reducing the principal balance (the original amount borrowed). The percentage of the principal included in the minimum payment varies depending on the lender and the terms of your agreement. A larger percentage is beneficial because it accelerates debt repayment, but it increases your monthly payment.

3. Draw Period vs. Repayment Period: HELOCs typically operate in two phases: the draw period and the repayment period. During the draw period, you can borrow funds up to your credit limit. The minimum payment during this phase often only covers the accrued interest. The repayment period follows, and the lender requires payments covering both interest and a significant portion of the principal.

4. Lender-Specific Calculations: Each lender has its own method for calculating the minimum payment, which may be detailed in your loan agreement. Some lenders use a simple interest-only minimum payment during the draw period, while others incorporate a small principal payment from the outset. It's crucial to review your loan documents carefully to understand your lender's specific calculation method.

5. Payment Schedules and Amortization: While most HELOCs have a variable interest rate and flexible payment options, some offer amortization schedules that outline a fixed payment plan over a specific period. This can help with budgeting but it might not always reflect the minimum payment requirement if your interest rate increases.

Closing Insights: Summarizing the Core Discussion

The HELOC minimum payment calculation isn't a one-size-fits-all solution. It's a dynamic process influenced by interest rates, outstanding balance, loan terms, and lender-specific policies. Understanding these factors is crucial for responsible HELOC management and avoiding potential financial setbacks.

Exploring the Connection Between Interest Rate Fluctuations and HELOC Minimum Payments

The relationship between interest rate fluctuations and HELOC minimum payments is directly proportional. As interest rates rise, the interest portion of your minimum payment increases, even if your outstanding balance remains constant. Conversely, a decrease in interest rates results in a lower minimum payment.

Key Factors to Consider:

- Roles and Real-World Examples: If your interest rate increases by 1%, your minimum payment could substantially increase, necessitating adjustments to your budget. Conversely, a decrease in rates could free up funds for other financial goals.

- Risks and Mitigations: Unpredictable interest rate hikes can make it difficult to manage your HELOC payments, potentially leading to delinquency. Monitoring interest rates and having a contingency plan are essential mitigations.

- Impact and Implications: Long-term, fluctuating interest rates significantly affect the total interest paid over the life of the loan. Higher rates increase the overall cost, while lower rates reduce it.

Conclusion: Reinforcing the Connection

The impact of interest rate changes on your HELOC minimum payment is undeniable. Regularly monitoring these rates and proactively adjusting your budget are critical for managing your debt effectively and minimizing the long-term costs associated with your HELOC.

Further Analysis: Examining Interest Rate Calculation in Greater Detail

The interest calculation on a HELOC typically uses a daily periodic rate. This daily rate is derived from the annual percentage rate (APR) divided by 365. The interest is then calculated daily on the outstanding principal balance, and this daily interest accrues until your next payment is made. This means that even small changes in the APR can lead to noticeable differences in your monthly interest charges.

FAQ Section: Answering Common Questions About HELOC Minimum Payments

Q: What happens if I only pay the minimum payment on my HELOC?

A: While paying only the minimum payment fulfills your contractual obligation, it prolongs the repayment period and increases your total interest paid over time. It's generally advisable to pay more than the minimum if possible.

Q: Can my HELOC minimum payment change?

A: Yes, your minimum payment can change, primarily due to fluctuating interest rates and changes in your outstanding balance. You should review your statement regularly to stay informed.

Q: What happens if I miss a HELOC minimum payment?

A: Missing a minimum payment can lead to late fees, damage your credit score, and negatively impact your creditworthiness. It might also trigger a change in your repayment terms.

Practical Tips: Maximizing the Benefits of HELOC Management

- Understand the Basics: Thoroughly review your HELOC agreement to understand the terms, fees, and calculation methods.

- Budgeting and Forecasting: Create a realistic budget that incorporates your HELOC payments, considering potential interest rate fluctuations.

- Regular Monitoring: Track your HELOC balance, payments, and interest accrual regularly to stay informed.

- Strategic Repayment: Consider making payments beyond the minimum to accelerate repayment and reduce the overall interest cost.

- Seek Professional Advice: Consult with a financial advisor for personalized guidance on managing your HELOC effectively.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding how your HELOC minimum payment is calculated is not just a matter of compliance; it's about responsible financial management. By understanding the nuances of interest accrual, payment schedules, and the impact of interest rate fluctuations, you can make informed decisions, optimize your repayment strategy, and avoid potential financial pitfalls. Proactive management of your HELOC can significantly impact your financial well-being, both in the short and long term. Take control of your finances by mastering the details of your HELOC minimum payment calculation.

Latest Posts

Latest Posts

-

How Does Amex Calculate Minimum Payment Due

Apr 05, 2025

-

How Is American Express Minimum Payment Calculated

Apr 05, 2025

-

How Does American Express Calculate Minimum Payment

Apr 05, 2025

-

What Is The Minimum Repayment On Barclaycard

Apr 05, 2025

-

How Does Barclays Calculate Minimum Payment

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about How Is The Minimum Payment Calculated On A Heloc . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.