What Is A Grace Period On Your Credit Card

adminse

Apr 02, 2025 · 10 min read

Table of Contents

What's the Secret Weapon Hiding in Your Credit Card Agreement? Understanding Grace Periods

Mastering your credit card grace period can significantly impact your financial well-being.

Editor’s Note: This article on credit card grace periods was published today, providing readers with up-to-date information and practical advice to manage their credit card accounts effectively. We've consulted leading financial experts and analyzed numerous credit card agreements to ensure accuracy and clarity.

Why Grace Periods Matter: Relevance, Practical Applications, and Financial Significance

Understanding your credit card's grace period is crucial for managing your finances responsibly. A grace period is the time you have after your billing cycle ends to pay your balance in full without incurring interest charges. This seemingly small window can save you hundreds, even thousands, of dollars over time. Effectively utilizing your grace period directly impacts your credit score, reduces overall debt, and contributes to better financial health. The implications extend beyond personal finance; understanding grace periods is relevant for businesses managing corporate credit cards and for anyone seeking to build a strong credit history.

Overview: What This Article Covers

This comprehensive article will dissect the intricacies of credit card grace periods. We’ll explore their definition, the factors that influence their length, how to maximize their benefits, common misconceptions, and the potential pitfalls of neglecting them. We will also delve into the relationship between grace periods and other key credit card features, offering actionable strategies to make the most of this valuable financial tool.

The Research and Effort Behind the Insights

This article is the product of extensive research, incorporating information from reputable financial institutions, consumer protection agencies, and legal documents related to credit card agreements. We've meticulously analyzed numerous credit card terms and conditions to ensure the accuracy and comprehensiveness of the information presented. The goal is to provide readers with clear, unbiased, and actionable insights based on verifiable data and authoritative sources.

Key Takeaways: Summarize the Most Essential Insights

- Definition and Core Concepts: A precise understanding of what constitutes a grace period and its fundamental principles.

- Grace Period Eligibility: The conditions that must be met to qualify for a grace period on your credit card.

- Calculating Your Grace Period: How to determine the precise length of your grace period based on your billing cycle and payment due date.

- Maximizing Grace Period Benefits: Strategies to fully utilize your grace period and avoid interest charges.

- Consequences of Missing Payments: The repercussions of not paying your balance in full before the grace period expires.

- Grace Period and Credit Score: The impact of grace period utilization (or lack thereof) on your credit rating.

- Common Misconceptions: Debunking prevalent myths surrounding credit card grace periods.

- Protecting Your Grace Period Rights: Understanding your rights as a consumer and how to address any discrepancies.

Smooth Transition to the Core Discussion

With a foundational understanding of the importance of grace periods, let’s delve into the specifics of how they work and how you can leverage them to your advantage.

Exploring the Key Aspects of Credit Card Grace Periods

Definition and Core Concepts:

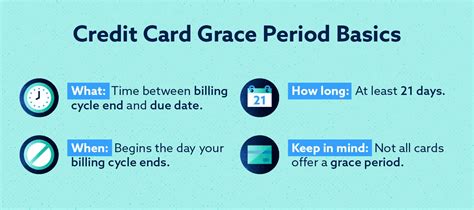

A grace period, in the context of credit cards, is the period of time between the end of your billing cycle and the date your payment is due. During this period, if you pay your statement balance in full, you will not be charged any interest on your purchases. This means you can essentially borrow money interest-free for a specific timeframe, provided you meet the conditions outlined in your credit card agreement. Crucially, this only applies to purchases; cash advances, balance transfers, and certain fees typically do not qualify for the grace period.

Eligibility for a Grace Period:

Not everyone automatically qualifies for a grace period. To be eligible, you generally must:

- Pay your previous month's balance in full: This is the most critical condition. If you carry a balance from the previous month, the grace period on your current purchases is often waived.

- Be current on your payments: Any late payments or accounts in default can invalidate your grace period.

- Not have violated any terms of your credit card agreement: Certain actions, such as exceeding your credit limit or engaging in fraudulent activity, might also negate your grace period.

- The grace period is offered by your credit card provider: Some credit cards, particularly those with high interest rates or fees, might not offer a grace period at all. Always check your credit card agreement for details.

Calculating Your Grace Period:

Your grace period is usually 21-25 days, but this can vary depending on your credit card issuer and the length of your billing cycle. The grace period begins on the date your billing cycle ends and ends on the due date printed on your statement. Carefully review your statement to determine the exact duration of your grace period. Late payments, even by a day, typically forfeit the grace period.

Maximizing Grace Period Benefits:

To fully benefit from your grace period, follow these steps:

- Pay your statement balance in full: This is the single most important step. Any outstanding balance will negate your grace period on new purchases.

- Track your spending: Monitor your credit card transactions closely to ensure you stay within your budget and avoid carrying a balance.

- Set up automatic payments: To avoid accidental late payments, consider setting up automatic payments that will debit your bank account before your due date.

- Read your credit card agreement: Familiarize yourself with the specific terms and conditions related to your grace period to ensure you understand your rights and responsibilities.

- Contact your credit card company: If you have questions or concerns about your grace period, do not hesitate to reach out to your credit card provider for clarification.

Consequences of Missing Payments:

Failing to pay your balance in full before the grace period expires will result in interest charges being applied to your outstanding balance. These interest charges can significantly increase the amount you owe, making it more difficult to manage your debt. Furthermore, late payments negatively impact your credit score, making it harder to obtain loans or other forms of credit in the future.

Grace Period and Credit Score:

On-time payments, including payments made within the grace period, are crucial for maintaining a good credit score. Consistent, timely payments demonstrate financial responsibility and positively influence your creditworthiness. Conversely, late payments, missed payments, and failing to utilize the grace period can severely damage your credit score.

Common Misconceptions:

- Myth: You have a grace period on cash advances and balance transfers. Reality: Cash advances and balance transfers typically do not have a grace period and accrue interest immediately.

- Myth: Your grace period is always 21 days. Reality: While common, the grace period can vary; always refer to your credit card agreement.

- Myth: Paying a minimum payment will preserve your grace period. Reality: Only paying the full statement balance preserves the grace period on new purchases.

Protecting Your Grace Period Rights:

If you believe your credit card company has improperly applied interest charges or denied you your grace period, take these steps:

- Review your credit card agreement: Ensure you are not violating any of the terms and conditions.

- Contact your credit card company: Explain the situation and request a review of the charges.

- File a complaint: If you are unable to resolve the issue with your credit card company, you can file a complaint with your state's attorney general or the Consumer Financial Protection Bureau (CFPB).

Closing Insights: Summarizing the Core Discussion

The credit card grace period is a powerful financial tool, but its benefits are contingent upon responsible credit card usage and a clear understanding of your credit card agreement. By diligently paying your statement balance in full before the due date, you can leverage this interest-free borrowing period, saving money and building a healthy credit history. Neglecting this valuable feature, however, can lead to significant financial burdens and damage your creditworthiness.

Exploring the Connection Between Late Payments and Grace Periods

Late payments significantly impact your ability to utilize your grace period. As previously mentioned, paying your previous month's balance in full is a fundamental requirement for accessing the grace period on new purchases. A single late payment can trigger interest charges on previous purchases and negate the grace period on new ones.

Key Factors to Consider:

- Roles and Real-World Examples: Consider a scenario where a cardholder misses a payment by even one day. This action immediately forfeits the grace period, resulting in interest accruing on all outstanding balances. This can snowball quickly, significantly increasing the overall cost of credit.

- Risks and Mitigations: The primary risk is accumulating significant debt due to compounded interest charges. Mitigations involve setting up automated payments, carefully budgeting, and setting reminders for payment due dates.

- Impact and Implications: The long-term impact of late payments extends beyond immediate financial consequences. They severely damage credit scores, impacting future loan applications, insurance rates, and even employment opportunities.

Conclusion: Reinforcing the Connection

The connection between late payments and grace periods is undeniable. Consistent timely payments are crucial for maintaining a positive credit history and taking full advantage of the grace period's financial benefits. By understanding this relationship and implementing strategies to avoid late payments, cardholders can significantly improve their financial well-being.

Further Analysis: Examining Late Payment Penalties in Greater Detail

Late payment penalties vary by credit card issuer, ranging from a flat fee to a percentage of the missed payment. These penalties, in addition to interest charges, rapidly increase the cost of carrying a balance. Many credit card agreements stipulate a specific grace period for disputing charges, so swift action is crucial.

FAQ Section: Answering Common Questions About Credit Card Grace Periods

Q: What happens if I only pay the minimum payment? A: Paying only the minimum payment does not preserve your grace period. Interest charges will accrue on your outstanding balance.

Q: Can I lose my grace period permanently? A: While not permanent, consistently late or missed payments can significantly affect your access to the grace period, possibly leading your issuer to revoke it altogether on future balances.

Q: What if my statement shows a different grace period than my agreement? A: Always refer to the official terms and conditions in your credit card agreement. If there is a discrepancy, contact your credit card issuer for clarification.

Q: Does a grace period apply to all types of credit card transactions? A: No, grace periods typically do not apply to cash advances, balance transfers, or certain fees.

Q: How does a grace period affect my credit score? A: Timely payments made during the grace period help maintain a good credit score. Late or missed payments negatively impact your credit score.

Practical Tips: Maximizing the Benefits of Your Credit Card Grace Period

- Understand Your Billing Cycle: Know when your billing cycle starts and ends.

- Track Your Spending: Monitor your spending throughout the billing cycle.

- Set Payment Reminders: Use calendar alerts or automatic payment options to ensure on-time payment.

- Pay in Full: Always aim to pay your statement balance in full before the due date.

- Review Your Statement: Regularly review your statements for accuracy and unexpected charges.

Final Conclusion: Wrapping Up with Lasting Insights

The credit card grace period is a valuable financial tool that can significantly reduce the overall cost of credit. By understanding its nuances, adhering to your credit card agreement, and consistently making timely payments, you can leverage this benefit and achieve better financial health. Proactive management and careful attention to your account ensure you maximize this often-overlooked feature. Remember, responsible credit card usage is key to financial success.

Latest Posts

Latest Posts

-

Calculate 18 Per Annum Interest

Apr 03, 2025

-

How Much Can I Charge For Late Fees

Apr 03, 2025

-

How To Compute Late Per Hour

Apr 03, 2025

-

How To Calculate Late Fees

Apr 03, 2025

-

How To Dispute Credit Card Charge Dbs

Apr 03, 2025

Related Post

Thank you for visiting our website which covers about What Is A Grace Period On Your Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.