What Is A Credit Cards Grace Period Quizlet

adminse

Apr 02, 2025 · 9 min read

Table of Contents

Decoding the Grace Period: Your Credit Card Quizlet Conquered

What if understanding your credit card grace period could save you hundreds, even thousands, of dollars in interest charges? Mastering this crucial aspect of credit card management is key to responsible spending and financial health.

Editor’s Note: This article on credit card grace periods provides a comprehensive overview of this critical financial concept, helping you understand how it works, its implications, and how to maximize its benefits. Updated [Date of Publication].

Why Understanding Your Grace Period Matters:

Credit card grace periods are often misunderstood, leading to unnecessary interest payments. Understanding this period is not just beneficial; it’s crucial for managing your credit card debt effectively and improving your overall financial well-being. This knowledge allows you to avoid accumulating interest charges, saving you significant money over time. It also plays a role in maintaining a healthy credit score, a vital factor in securing loans, mortgages, and even rental properties. Ignoring your grace period can lead to a snowball effect of debt, impacting your financial stability. This article will clarify the intricacies of grace periods, arming you with the knowledge to make informed decisions regarding your credit card usage.

Overview: What This Article Covers:

This in-depth guide will dissect the concept of a credit card grace period, covering its definition, how it's calculated, factors that affect it, what happens when you miss a payment, and strategies to fully utilize this valuable benefit. We'll also explore the differences between grace periods for purchases and cash advances, address common misconceptions, and provide actionable tips for maximizing your grace period. Finally, we will address some frequently asked questions to comprehensively cover all aspects of this topic.

The Research and Effort Behind the Insights:

This article draws upon extensive research from reputable sources, including financial institutions' websites, consumer finance authorities like the Consumer Financial Protection Bureau (CFPB), and leading personal finance publications. The information provided is factual and intended to offer clear, actionable insights backed by reliable data and expert analysis. The aim is to demystify the grace period concept, empowering readers to make confident financial choices.

Key Takeaways:

- Definition and Core Concepts: A precise definition of a credit card grace period and its foundational principles.

- Purchase vs. Cash Advance Grace Periods: Understanding the key differences and their financial implications.

- Calculating Your Grace Period: A step-by-step guide to understanding how your grace period is determined.

- Factors Affecting Grace Periods: Exploring variables that can impact the length of your grace period.

- Consequences of Missing a Payment: Understanding the implications of not paying your balance in full by the due date.

- Maximizing Your Grace Period: Practical strategies for taking full advantage of this benefit.

- Common Misconceptions: Addressing frequently held, but inaccurate beliefs about grace periods.

Smooth Transition to the Core Discussion:

Now that we've established the importance of understanding credit card grace periods, let's delve into the specifics of what constitutes this crucial period and how it impacts your finances.

Exploring the Key Aspects of Credit Card Grace Periods:

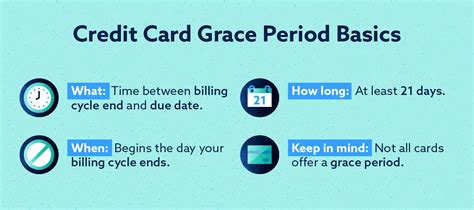

Definition and Core Concepts: A credit card grace period is the time between the end of your billing cycle and the due date of your payment during which you can avoid paying interest on purchases. This essentially means that if you pay your statement balance in full by the due date, you won't be charged any interest on those purchases. It's a crucial feature designed to benefit responsible cardholders. The grace period typically ranges from 21 to 25 days, but it can vary depending on your credit card issuer and your payment history.

Purchase vs. Cash Advance Grace Periods: There's a significant difference between how grace periods apply to purchases and cash advances. Purchases made using your credit card usually qualify for the grace period. However, cash advances – which are essentially loans taken directly from your available credit – typically do not have a grace period. This means that interest starts accruing immediately on cash advances, often at a much higher rate than interest on purchases. This highlights the importance of understanding the distinction and using cash advances only when absolutely necessary.

Calculating Your Grace Period: The calculation of your grace period involves several factors. First, your billing cycle ends on a specific date. This is when your statement is generated, outlining all your transactions during that period. The due date is then typically 21-25 days after the end of the billing cycle. The grace period is the timeframe between the end of your billing cycle and this payment due date. Failing to pay the full balance by the due date eliminates the grace period for the next billing cycle.

Factors Affecting Grace Periods: Several factors influence the length of your grace period. Firstly, as mentioned, your credit card issuer sets the minimum grace period. Some issuers might offer longer grace periods as a reward for good credit history or as a feature of a specific card. Your payment history is also a key factor. Consistent late payments can cause your issuer to shorten or even eliminate your grace period. It's also important to note that making only minimum payments generally negates the benefit of the grace period. This is because interest charges accumulate, exceeding the amount you paid, thus eliminating the grace period's effect.

Consequences of Missing a Payment: Missing your payment due date has several severe consequences. The most immediate is the loss of the grace period for the next billing cycle, meaning you'll start accruing interest immediately on any outstanding balance. Furthermore, late payment fees will be applied, adding to your outstanding debt. Repeated late payments will damage your credit score, making it more difficult to secure future loans or credit lines. This can even impact your ability to rent an apartment or get certain jobs.

Maximizing Your Grace Period: Here are several strategies to fully leverage your credit card's grace period:

- Pay in Full and on Time: This is the most crucial step. Ensure you pay your statement balance in full by the due date to avoid interest charges. Set up automatic payments to prevent accidental late payments.

- Track Your Spending: Monitor your spending throughout the billing cycle to avoid overspending and exceeding your budget. This prevents accumulating a balance that might be difficult to pay in full.

- Understand Your Billing Cycle: Be aware of your billing cycle's end date and the due date to ensure you have ample time to make your payment.

- Use Online Banking Tools: Many banks offer online banking tools that allow you to schedule payments and receive reminders, reducing the risk of missed payments.

Common Misconceptions:

- Minimum Payments Utilize Grace Periods: Many believe that making minimum payments utilizes the grace period. This is incorrect. Minimum payments only cover a portion of the interest accrued, leaving the remaining balance to incur additional interest. This negates the grace period's benefit.

- Grace Periods Apply to All Transactions: Cash advances and balance transfers typically don't have grace periods. Interest starts accumulating immediately on these transactions.

- Grace Periods Are Static: While the standard grace period is usually 21-25 days, late payments can shorten or even eliminate it.

Exploring the Connection Between Responsible Spending and Grace Periods:

Responsible spending is inextricably linked to effectively utilizing grace periods. Overspending and accumulating debt can quickly erode the benefits of the grace period. By practicing responsible spending habits – budgeting, tracking expenses, and paying off balances in full – you can maximize the advantages of the grace period, saving significant money on interest charges.

Key Factors to Consider:

Roles and Real-World Examples: Responsible spending habits, such as meticulous budgeting and tracking expenses, ensure that you can pay your credit card balance in full by the due date, thereby maximizing your grace period. For example, someone who diligently tracks their spending throughout the month and avoids unnecessary purchases is more likely to pay off their balance in full and enjoy the interest-free period. Conversely, someone who consistently overspends and makes only minimum payments will quickly find the grace period rendered ineffective.

Risks and Mitigations: The primary risk is failing to pay in full by the due date, leading to interest charges, late fees, and damage to your credit score. Mitigation strategies include setting up automatic payments, utilizing budgeting tools, and monitoring your spending closely.

Impact and Implications: Effectively utilizing grace periods can significantly reduce interest expenses, saving substantial money over time. This allows for greater financial flexibility and reduces the burden of credit card debt.

Conclusion: Reinforcing the Connection:

The connection between responsible spending and maximizing your grace period is undeniable. By adopting prudent financial habits and paying your balance in full and on time, you can fully leverage this benefit and enjoy significant cost savings.

Further Analysis: Examining Responsible Spending in Greater Detail:

Responsible spending encompasses numerous strategies beyond simply paying your credit card balance on time. It includes creating a realistic budget, tracking income and expenses, setting financial goals, and avoiding impulsive purchases. This proactive approach to personal finance not only maximizes the benefits of grace periods but also builds a strong foundation for long-term financial health.

FAQ Section: Answering Common Questions About Credit Card Grace Periods:

-

Q: What happens if I miss my credit card payment due date?

- A: You lose your grace period for the next billing cycle, and interest charges and late fees will be applied. Your credit score will also be negatively impacted.

-

Q: Does paying the minimum payment utilize my grace period?

- A: No, paying only the minimum payment does not utilize your grace period. Interest continues to accrue on the remaining balance.

-

Q: How long is a typical grace period?

- A: Grace periods typically range from 21 to 25 days, but this can vary depending on your issuer and payment history.

-

Q: Do cash advances have grace periods?

- A: Typically, no. Interest starts accruing immediately on cash advances.

-

Q: How can I improve my chances of getting a longer grace period?

- A: Maintaining a good credit history and consistent on-time payments are crucial.

Practical Tips: Maximizing the Benefits of Credit Card Grace Periods:

- Set up automatic payments: This ensures timely payments and prevents accidental late payments.

- Use budgeting apps: Track your spending and ensure you're staying within your budget.

- Check your statement carefully: Verify all charges and report any discrepancies immediately.

- Pay your balance in full by the due date: This is crucial for maximizing the grace period’s benefits.

- Read your credit card agreement: Understand the terms and conditions related to your grace period.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding and maximizing your credit card grace period is a fundamental aspect of responsible credit card management. By diligently paying your statement balance in full and on time, you can avoid accumulating interest charges, save significant money, and protect your credit score. This knowledge empowers you to make informed financial decisions, paving the way for greater financial stability and success. Remember, responsible spending is the key to unlocking the full potential of your credit card grace period.

Latest Posts

Latest Posts

-

Liquidity Pool Crypto Adalah

Apr 04, 2025

-

What Is Liquidity Pool In Blockchain

Apr 04, 2025

-

What Is A Liquidity Pool In Cryptocurrency

Apr 04, 2025

-

Quickbooks Late Fees

Apr 04, 2025

-

How To Set Up Automatic Late Fees In Quickbooks Desktop

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about What Is A Credit Cards Grace Period Quizlet . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.