What If I Pay The Minimum On My Credit Card

adminse

Apr 04, 2025 · 7 min read

Table of Contents

What if I Only Pay the Minimum on My Credit Card? The High Cost of Convenience

What if the seemingly small act of paying only the minimum on your credit card could lead to a financial crisis? Ignoring the implications of minimum payments can snowball into a debt trap that takes years, if not decades, to escape.

Editor’s Note: This article on the consequences of paying only the minimum on your credit card was published today. Understanding the intricacies of credit card debt is crucial for maintaining sound financial health. This information will empower you to make informed decisions about your finances.

Why Paying Only the Minimum Matters: Relevance, Practical Applications, and Industry Significance

The allure of credit cards is undeniable – convenience, rewards programs, and emergency funds are just some of the advantages. However, the ease of access often masks a significant risk: the high cost of carrying a balance by only making minimum payments. This practice, while seemingly harmless in the short-term, can lead to crippling debt, negatively impacting credit scores, and significantly hindering long-term financial goals like homeownership or retirement planning. The implications are far-reaching, affecting not only personal finances but also impacting the overall economy through increased consumer debt burdens.

Overview: What This Article Covers

This article provides a comprehensive analysis of the consequences of paying only the minimum on your credit card. We will explore the mechanics of interest accrual, the impact on credit scores, the long-term financial implications, and strategies to avoid falling into the debt trap. Readers will gain actionable insights, backed by factual information and real-world examples.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon data from consumer finance agencies, credit reporting bureaus, and financial literacy resources. Calculations and examples are based on realistic interest rates and minimum payment structures, reflecting the current financial landscape. The goal is to present accurate and trustworthy information that empowers readers to make informed decisions.

Key Takeaways:

- Understanding Interest Accrual: A detailed explanation of how compounding interest works and how it quickly amplifies credit card debt.

- Impact on Credit Scores: How consistently paying only the minimum negatively impacts creditworthiness.

- Long-Term Financial Implications: The cascading effects of high-interest debt on future financial goals.

- Strategies for Debt Management: Practical steps to overcome credit card debt and regain financial control.

Smooth Transition to the Core Discussion

Now that we understand the gravity of this issue, let's delve into the specific mechanisms that drive the escalating cost of paying only the minimum on your credit card.

Exploring the Key Aspects of Paying Only the Minimum

1. Definition and Core Concepts:

Paying the minimum payment on a credit card refers to paying only the stated minimum amount due on your monthly statement. This amount typically covers a small portion of the balance, often just the interest accrued and a tiny fraction of the principal. The remaining balance carries over to the next month, accruing additional interest.

2. Interest Accrual: The Compound Effect:

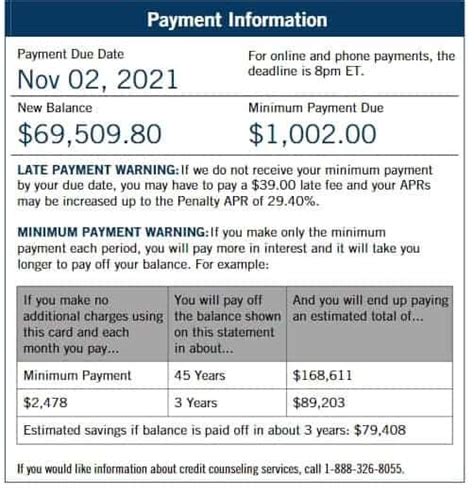

Credit cards typically charge high annual percentage rates (APRs), often ranging from 15% to 30% or even higher. This interest is compounded daily or monthly, meaning interest is calculated not only on the original principal balance but also on the accumulated interest. This compounding effect is a significant factor in rapidly increasing the overall debt. Let's illustrate with an example:

Suppose you have a $1,000 balance with a 20% APR. Your minimum payment might be around $25. If you only pay the minimum each month, a significant portion of your payment goes towards interest, leaving a much smaller amount to reduce the principal. Over time, the interest charges consistently outweigh your payments, causing the debt to grow exponentially.

3. Impact on Credit Scores:

Credit scores are crucial for obtaining loans, mortgages, and even securing certain jobs. Consistently paying only the minimum payment significantly harms your credit score. Credit bureaus track your payment history, and late or minimum payments are negative indicators. A low credit score results in higher interest rates on future loans, limiting your borrowing capacity, and impacting your overall financial well-being.

4. Long-Term Financial Implications:

The implications of carrying a high credit card balance extend far beyond your credit score. The persistent interest charges consume a large portion of your monthly budget, hindering your ability to save, invest, or achieve significant financial goals. It can create a cycle of debt, making it difficult to escape the burden of minimum payments. This can delay major life milestones like buying a house, investing in education, or securing a comfortable retirement.

Exploring the Connection Between High Interest Rates and Paying Only the Minimum

The relationship between high interest rates and paying only the minimum is inextricably linked. High interest rates accelerate the growth of debt when only minimum payments are made. This is because a larger portion of the minimum payment is allocated to interest, leaving less to reduce the principal.

Key Factors to Consider:

- Roles and Real-World Examples: Many individuals, particularly those facing financial hardship, resort to minimum payments, hoping to manage their finances. However, this often backfires, leading to a larger debt burden.

- Risks and Mitigations: The risk of snowballing debt is significant. To mitigate this, creating a realistic budget, exploring debt consolidation options, or seeking professional financial advice are crucial steps.

- Impact and Implications: The long-term impact of consistently making minimum payments can lead to severe financial strain, hindering opportunities and creating significant stress.

Conclusion: Reinforcing the Connection

The connection between high interest rates and minimum payments underscores the importance of proactive debt management. By understanding the exponential growth of debt due to high interest and minimum payments, individuals can make informed choices to prevent financial distress.

Further Analysis: Examining APRs in Greater Detail

The Annual Percentage Rate (APR) is a crucial factor in understanding the cost of credit. A higher APR translates to significantly higher interest charges, exacerbating the problem of paying only the minimum. Understanding the APR on your credit card is paramount in managing your debt effectively.

FAQ Section: Answering Common Questions About Minimum Payments

Q: What is the minimum payment?

A: The minimum payment is the lowest amount you can pay on your credit card statement each month without incurring late fees. However, it's usually insufficient to reduce the principal balance significantly.

Q: How is the minimum payment calculated?

A: The calculation varies by credit card issuer, but it generally includes a portion of the interest accrued and a small fraction of the principal.

Q: What happens if I consistently pay only the minimum?

A: You'll likely accrue significant interest charges, increasing your debt balance. This impacts your credit score and hinders your ability to reach financial goals.

Q: What are the alternatives to paying only the minimum?

A: Alternatives include paying more than the minimum, creating a debt repayment plan, or seeking professional financial counseling.

Practical Tips: Maximizing the Benefits of Responsible Credit Card Use

-

Understand Your APR: Know the APR on your credit card to understand the true cost of carrying a balance.

-

Pay More Than the Minimum: Make larger payments whenever possible to reduce the principal balance more quickly and save on interest.

-

Create a Budget: Track your income and expenses to determine how much you can realistically allocate towards debt repayment.

-

Consider Debt Consolidation: Explore options to consolidate high-interest debts into a loan with a lower interest rate.

-

Seek Professional Help: If you're struggling with credit card debt, contact a credit counselor or financial advisor for assistance.

Final Conclusion: Wrapping Up with Lasting Insights

Paying only the minimum on your credit card can seem like a convenient option in the short term, but it carries significant long-term risks. The compounding effect of high interest rates quickly transforms manageable debt into an overwhelming burden. By understanding the mechanics of interest, the impact on credit scores, and the long-term consequences, you can make informed decisions to avoid the debt trap and achieve better financial well-being. Proactive debt management, including paying more than the minimum, creating a budget, and seeking professional help when needed, are crucial steps in ensuring a secure financial future.

Latest Posts

Latest Posts

-

How Does Chase Credit Card Calculate Minimum Payment

Apr 05, 2025

-

How Does Chase Calculate Minimum Payment

Apr 05, 2025

-

Whats The Minimum Payment For Ssi

Apr 05, 2025

-

What Is The Minimum Ssdi Disability Payment

Apr 05, 2025

-

What Is The Minimum Social Security Disability Payment Per Month

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about What If I Pay The Minimum On My Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.