What Does Total Minimum Payment Mean On Credit Card

adminse

Apr 05, 2025 · 8 min read

Table of Contents

Decoding the Total Minimum Payment on Your Credit Card: A Comprehensive Guide

What if understanding your credit card's total minimum payment could save you thousands of dollars over your lifetime? Mastering this crucial concept is key to responsible credit card management and achieving financial freedom.

Editor’s Note: This article on understanding your credit card’s total minimum payment was published today. We aim to provide you with clear, concise, and up-to-date information to help you navigate the complexities of credit card debt.

Why Understanding Your Total Minimum Payment Matters:

Understanding your credit card's total minimum payment is far more critical than simply knowing the number. It directly impacts your debt repayment journey, your credit score, and ultimately, your financial health. Paying only the minimum can lead to significantly higher interest charges, prolonging debt and increasing its overall cost. Conversely, understanding and strategically managing your minimum payment can contribute to faster debt reduction and improved financial well-being. This knowledge is relevant whether you're a seasoned credit card user or just starting out.

Overview: What This Article Covers:

This article provides a thorough explanation of what constitutes a total minimum payment on a credit card. We'll delve into how it's calculated, the potential pitfalls of only paying the minimum, strategies for paying more than the minimum, and the implications for your credit score and overall financial health. We will also explore scenarios where your minimum payment might fluctuate and how to avoid common misconceptions.

The Research and Effort Behind the Insights:

This article is the result of extensive research, drawing on information from leading financial institutions, consumer protection agencies, and reputable financial literacy resources. We've analyzed numerous credit card agreements and consulted expert opinions to ensure accuracy and clarity. The information presented here is intended to be educational and should not be considered financial advice. Always consult with a qualified financial advisor for personalized guidance.

Key Takeaways:

- Definition and Core Concepts: A clear definition of the total minimum payment and the factors influencing its calculation.

- Practical Applications: Real-world examples illustrating the long-term cost of paying only the minimum payment.

- Strategies for Debt Reduction: Actionable strategies for paying down credit card debt efficiently.

- Impact on Credit Score: The relationship between minimum payments and your creditworthiness.

- Avoiding Common Pitfalls: Identifying and avoiding common misconceptions about minimum payments.

Smooth Transition to the Core Discussion:

Now that we understand the importance of this topic, let's delve into the specifics of what constitutes a total minimum payment on your credit card.

Exploring the Key Aspects of Total Minimum Payment:

1. Definition and Core Concepts:

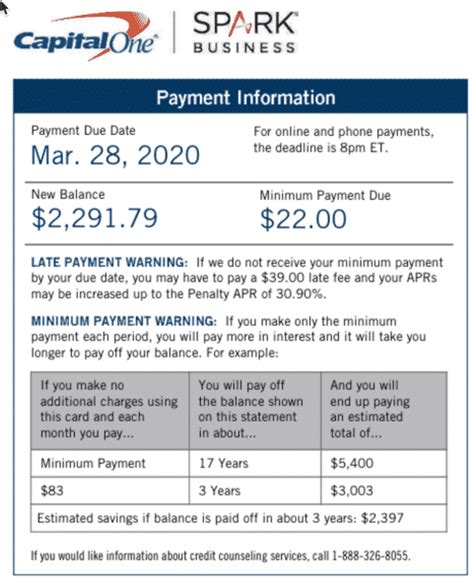

The total minimum payment on your credit card is the smallest amount you can pay each month to avoid late payment fees and maintain your account in good standing. This amount is typically stated clearly on your monthly credit card statement. However, understanding what goes into that number is crucial. The minimum payment is usually calculated as a percentage of your outstanding balance (often 1-3%), plus any accrued interest and any other fees. Therefore, it's not simply a fixed amount; it fluctuates based on your spending, repayment habits, and the applicable interest rate.

2. Applications Across Industries:

The calculation and presentation of the minimum payment are largely standardized across the credit card industry. However, variations may exist based on the specific issuer (e.g., Visa, Mastercard, American Express) and the type of credit card you possess (e.g., secured vs. unsecured, rewards card vs. basic card). Most credit card companies clearly outline their minimum payment calculation method within their terms and conditions. It is essential to review these terms to fully understand the specifics for your card.

3. Challenges and Solutions:

The biggest challenge associated with the minimum payment is the misconception that it's a viable long-term repayment strategy. Paying only the minimum payment will dramatically increase the total cost of your credit card debt due to the compounding effect of interest. The solution lies in developing a proactive repayment plan that involves paying significantly more than the minimum each month. This can involve budgeting, prioritizing debt repayment, and exploring debt consolidation options.

4. Impact on Innovation:

While the core concept of the minimum payment remains largely unchanged, the credit card industry continues to innovate in terms of providing tools and resources to help consumers manage their debt. Many credit card companies now offer online tools and mobile apps that allow users to track their spending, monitor their payments, and explore different repayment scenarios to better understand the long-term implications of their payment choices.

Closing Insights: Summarizing the Core Discussion:

The total minimum payment is a deceptively simple concept that can have profound financial consequences. While it provides a safety net against late payment fees, relying solely on it can trap you in a cycle of debt for years, costing you significantly more in interest than you initially borrowed.

Exploring the Connection Between Interest Rates and Total Minimum Payment:

The relationship between interest rates and the total minimum payment is crucial. A higher interest rate translates to a larger portion of your minimum payment going toward interest rather than principal. This means it will take significantly longer to pay off your balance, leading to higher overall costs. Conversely, a lower interest rate allows a larger portion of your minimum payment to be applied to the principal, accelerating debt reduction.

Key Factors to Consider:

- Roles and Real-World Examples: Imagine two individuals with the same outstanding balance, one with a 15% interest rate and the other with a 25% interest rate. The individual with the higher interest rate will find a significantly larger portion of their minimum payment going toward interest, making it much harder to pay off their debt.

- Risks and Mitigations: The primary risk is prolonged debt and higher overall costs. Mitigation strategies include proactively paying more than the minimum, negotiating a lower interest rate with your credit card company, or exploring debt consolidation options.

- Impact and Implications: The long-term impact of high interest rates and minimum payments can include hampered financial growth, decreased credit score, and stress related to managing debt.

Conclusion: Reinforcing the Connection:

The interplay between interest rates and the minimum payment underscores the importance of understanding your credit card agreement thoroughly. By proactively managing your spending, negotiating favorable interest rates, and paying more than the minimum, you can minimize the cost of credit and achieve financial stability.

Further Analysis: Examining Interest Calculation in Greater Detail:

Credit card interest is typically calculated using the average daily balance method. This means that the interest charge is based on the average balance of your account over the billing cycle. Understanding this calculation method is critical because it impacts the amount of interest accrued each month and therefore, the size of your minimum payment.

FAQ Section: Answering Common Questions About Total Minimum Payment:

-

Q: What happens if I only pay the minimum payment?

- A: While you avoid late payment fees, you’ll accrue significant interest, prolonging your debt and increasing the total cost of borrowing.

-

Q: Can my minimum payment change?

- A: Yes, it fluctuates based on your balance, interest rates, and any added fees.

-

Q: What if I can't afford the minimum payment?

- A: Contact your credit card company immediately. They may offer hardship programs or payment plans to help you manage your debt.

-

Q: How can I lower my minimum payment?

- A: The most effective way is to pay down your balance significantly. Paying more than the minimum each month reduces your balance, thus lowering the future minimum payment.

-

Q: Is it always better to pay more than the minimum?

- A: Absolutely. Paying extra reduces the total interest paid, saving you money and helping you become debt-free faster.

Practical Tips: Maximizing the Benefits of Understanding Your Minimum Payment:

-

Understand the Basics: Thoroughly read your credit card agreement to understand how your minimum payment is calculated.

-

Track Your Spending: Monitor your spending habits closely to avoid unnecessary debt accumulation.

-

Create a Budget: Develop a budget that allocates funds towards paying more than the minimum payment each month.

-

Explore Debt Reduction Strategies: Consider strategies such as the debt snowball or debt avalanche methods to accelerate your repayment.

-

Negotiate with Your Credit Card Company: If you're struggling, contact your creditor to explore options like lower interest rates or payment plans.

Final Conclusion: Wrapping Up with Lasting Insights:

The total minimum payment is a crucial element in managing your credit card debt. However, it's a tool that should be used wisely, not as a long-term repayment strategy. By understanding how it's calculated, the potential pitfalls of only paying the minimum, and adopting proactive debt reduction strategies, you can take control of your finances and build a strong foundation for future financial success. Remember, knowledge is power – and understanding your minimum payment empowers you to make informed financial decisions that benefit your financial well-being.

Latest Posts

Latest Posts

-

Money Management Rules In Trading

Apr 06, 2025

-

What Is The Primary Goal Of Money Management In Trading

Apr 06, 2025

-

What Is Money Management And Risk Management In Trading

Apr 06, 2025

-

What Is Cash Management Trading

Apr 06, 2025

-

What Is Money Management In Binary Trading

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about What Does Total Minimum Payment Mean On Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.