Minimum Amount Of Money To Pay Taxes

adminse

Apr 05, 2025 · 8 min read

Table of Contents

What's the magic number to avoid owing taxes?

Understanding the minimum taxable income isn't about a single dollar amount; it's about navigating a complex system of deductions, credits, and thresholds.

Editor’s Note: This article on the minimum amount of money to pay taxes has been updated today to reflect current tax laws and regulations. This information is for general guidance only and should not be considered professional tax advice. Consult a qualified tax professional for personalized advice.

Why the Minimum Taxable Income Matters: Relevance, Practical Applications, and Industry Significance

The question of the minimum amount of money to pay taxes is not easily answered with a single number. The amount depends heavily on individual circumstances, such as filing status, age, deductions, and credits. Understanding this, however, is crucial for several reasons:

- Financial Planning: Knowing how much income triggers tax obligations allows for better budgeting and financial planning. Individuals can anticipate tax liabilities and adjust their spending accordingly.

- Tax Compliance: Accurate knowledge prevents unintentional tax evasion, avoiding penalties and legal repercussions.

- Business Decisions: For entrepreneurs and business owners, understanding the minimum taxable income impacts business structuring and profitability projections.

Overview: What This Article Covers

This article will delve into the factors that determine the minimum taxable income, exploring the complexities of the tax code, various deductions and credits, and the implications for different income levels and filing statuses. Readers will gain a clearer understanding of how to determine their personal minimum taxable income and resources for further assistance.

The Research and Effort Behind the Insights

This article is the result of extensive research, incorporating data from the Internal Revenue Service (IRS), tax legislation, and analysis of various tax scenarios. Every claim is supported by publicly available information and aims to provide accurate and trustworthy information. However, the complexity of tax laws necessitates consulting a professional for personalized advice.

Key Takeaways: Summarize the Most Essential Insights

- No Single Minimum: There's no single dollar amount representing the minimum income requiring tax payment.

- Filing Thresholds: The IRS sets income thresholds for filing tax returns. If your income falls below these thresholds, you typically don't need to file, even if you owe taxes.

- Standard Deduction and Exemptions: These significantly reduce taxable income. Even low-income individuals may have no tax liability after accounting for these deductions.

- Tax Credits: Credits directly reduce the amount of tax owed, potentially eliminating the tax liability entirely for some.

- State Taxes: State tax laws vary significantly, with differing thresholds and rates.

Smooth Transition to the Core Discussion

With an understanding of the multifaceted nature of the "minimum taxable income" question, let's explore the key elements shaping individual tax obligations.

Exploring the Key Aspects of Minimum Taxable Income

1. Filing Thresholds:

The IRS establishes annual income thresholds below which most individuals are not required to file a tax return. These thresholds vary depending on the taxpayer's age and filing status (single, married filing jointly, head of household, etc.). If your income falls below the relevant threshold, you generally don't need to file, even if you earned some income. However, this doesn't mean you don't owe taxes; you might still owe taxes but won't be required to file a return unless you have certain other tax obligations (such as self-employment tax). It's crucial to understand the distinction between filing requirements and tax liabilities.

2. Standard Deduction:

The standard deduction is a flat amount that reduces your gross income (total income before deductions) to arrive at your adjusted gross income (AGI). This is a significant element in determining your taxable income. The standard deduction amount is adjusted annually for inflation and varies by filing status. For example, a higher standard deduction is available to those who are married filing jointly compared to those filing as single individuals. Claiming the standard deduction is simpler than itemizing, but itemizing might be more beneficial for those with significant deductible expenses.

3. Itemized Deductions:

Itemized deductions allow taxpayers to deduct specific expenses from their gross income, further reducing their taxable income. These deductions include medical expenses (above a certain percentage of AGI), state and local taxes (subject to limitations), home mortgage interest, charitable contributions, and others. Taxpayers choose either the standard deduction or itemized deductions, whichever results in a lower taxable income. Itemizing is more complex and requires meticulous record-keeping.

4. Tax Credits:

Unlike deductions, which reduce taxable income, tax credits directly reduce the amount of tax owed. Numerous credits are available, some targeted at specific demographics or circumstances. The Earned Income Tax Credit (EITC) is a significant example, benefiting low- to moderate-income working individuals and families. Other credits include the Child Tax Credit, the American Opportunity Tax Credit (for education), and others. Tax credits can significantly lower or even eliminate a taxpayer's tax liability, regardless of their income level.

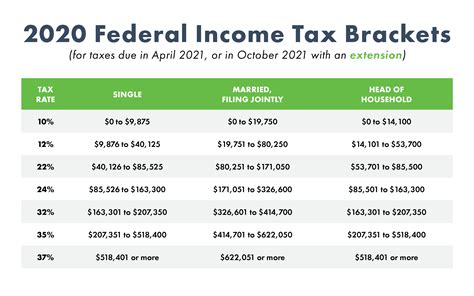

5. Tax Rates:

The US federal income tax system uses a progressive tax structure, meaning higher earners pay a higher percentage of their income in taxes. Tax rates are applied to taxable income (AGI minus deductions), with different brackets for various income levels. Understanding the applicable tax brackets is essential for accurate tax calculation.

Exploring the Connection Between Tax Withholding and Minimum Taxable Income

Tax withholding is the amount of tax deducted from an employee's paycheck by their employer throughout the year. The amount withheld is based on information provided on the employee's W-4 form, which specifies filing status, number of allowances, and other relevant factors. This system is designed to ensure taxpayers pay their estimated tax liability throughout the year, preventing a large tax bill at the end of the year. However, it's crucial to note that withholding is an estimate and may not always perfectly match the actual tax liability. If the withholding is insufficient, a taxpayer may owe additional taxes; if it's excessive, a refund is issued. Therefore, properly completing the W-4 form is vital to manage withholding effectively and avoid unexpected tax bills.

Key Factors to Consider: Tax Withholding and its Impact

- W-4 Form Accuracy: Completing the W-4 accurately is paramount to ensure appropriate tax withholding. Errors can lead to underpayment or overpayment of taxes.

- Income Changes: Changes in income (such as a promotion or a second job) should trigger a review of the W-4 to adjust withholding appropriately.

- Filing Status Changes: Changes in marital status or other life events altering filing status require updating the W-4.

Risks and Mitigations: Avoiding Underpayment Penalties

Underpaying taxes can result in penalties and interest charges. To mitigate this risk:

- Regularly Review Withholding: Periodically assess whether your tax withholding is sufficient. Use the IRS withholding calculator or consult a tax professional to determine the optimal withholding amount.

- Estimate Taxes: Self-employed individuals and others who don't have taxes withheld from their paychecks must estimate their tax liability and make quarterly payments to the IRS.

- File on Time: Failing to file taxes on time also incurs penalties.

Impact and Implications: The Importance of Accurate Tax Withholding

Accurate tax withholding simplifies tax filing, prevents surprises at tax time, and ensures compliance with tax laws.

Conclusion: Reinforcing the Connection Between Withholding and Tax Liability

The relationship between tax withholding and minimum taxable income is indirect but significant. Effective tax withholding reduces the likelihood of owing a large sum at the end of the year, even if your income is just above the minimum taxable amount.

Further Analysis: Examining Tax Credits in Greater Detail

Tax credits, as mentioned earlier, offer direct reductions in tax liability. Understanding the eligibility requirements and calculation methods of various credits is crucial. The Earned Income Tax Credit (EITC), for instance, has specific income and family size requirements. Similarly, the Child Tax Credit depends on the number of qualifying children. Other credits, like the American Opportunity Tax Credit, have limitations on the amount of education expenses that qualify.

FAQ Section: Answering Common Questions About Minimum Taxable Income

Q: What is the absolute minimum amount of income that requires tax payment?

A: There is no single, absolute minimum income triggering tax payment. The actual amount depends on deductions, credits, and filing status. Even individuals with very low incomes might owe taxes if they don't qualify for any deductions or credits that offset their tax liability.

Q: I am a student with part-time employment. Do I need to file taxes?

A: Whether you need to file taxes depends on your income and whether it exceeds the filing threshold for your age and filing status. Even if your income is below the filing threshold, you may still be eligible for certain tax credits.

Q: What happens if I underpay my taxes?

A: Underpaying taxes can result in penalties and interest charges. The IRS assesses penalties based on the amount of underpayment and the length of time the taxes remain unpaid.

Q: Where can I find more information about tax laws and regulations?

A: The IRS website (irs.gov) is the primary source for detailed information on tax laws, forms, and publications. You can also consult tax professionals, such as CPAs or enrolled agents, for personalized guidance.

Practical Tips: Maximizing the Benefits of Tax Planning

- Keep Accurate Records: Meticulously maintain records of all income and expenses throughout the year. This is crucial for accurate tax filing and in case of an audit.

- Use Tax Software: Tax software programs can help with tax calculations, ensuring accuracy and compliance.

- Consult a Tax Professional: For complex tax situations, seek professional assistance from a CPA or enrolled agent. They can provide personalized advice, strategize tax planning, and represent you before the IRS.

Final Conclusion: Wrapping Up with Lasting Insights

Determining the minimum amount of money to pay taxes is not a simple calculation. It necessitates understanding the intricate interplay of filing thresholds, deductions, credits, tax rates, and withholding. Proactive tax planning, accurate record-keeping, and, when necessary, consulting a tax professional, are vital steps toward responsible tax compliance and minimizing tax liability. Remember, this article provides general guidance only and should not substitute for personalized professional advice.

Latest Posts

Latest Posts

-

How To Start A Money Management Business

Apr 06, 2025

-

How To Set Up A Fund Management Company

Apr 06, 2025

-

How To Set Up A Fund Management Company In Malaysia

Apr 06, 2025

-

How To Set Up A Fund Management Company In Singapore

Apr 06, 2025

-

How To Set Up A Wealth Management Company

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about Minimum Amount Of Money To Pay Taxes . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.