What Does Total Minimum Payment Due Mean On A Credit Card

adminse

Apr 05, 2025 · 7 min read

Table of Contents

Decoding Your Credit Card Statement: What Does "Total Minimum Payment Due" Really Mean?

What if ignoring the "Total Minimum Payment Due" on your credit card statement could lead to serious financial consequences? Understanding this seemingly simple figure is crucial for maintaining good credit health and avoiding crippling debt.

Editor’s Note: This article on "Total Minimum Payment Due" on credit card statements was published today. We've compiled comprehensive information to help you navigate this important aspect of credit card management.

Why "Total Minimum Payment Due" Matters: Relevance, Practical Applications, and Industry Significance

The "Total Minimum Payment Due" (often shortened to "Minimum Payment Due") on your credit card statement is more than just a suggested payment; it's a critical threshold influencing your credit score, overall debt, and financial well-being. Ignoring this seemingly small number can lead to a cascade of negative consequences, including accumulating high interest charges, damaging your credit rating, and even potential legal action. Understanding its implications is essential for responsible credit card usage. This understanding allows for better financial planning and empowers individuals to make informed decisions about their debt management.

Overview: What This Article Covers

This article will delve into the meaning of "Total Minimum Payment Due," explaining its calculation, implications, the potential pitfalls of only paying the minimum, strategies for managing credit card debt effectively, and addressing frequently asked questions. Readers will gain a clear understanding of how this seemingly small number impacts their financial future.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon information from leading financial institutions, credit bureaus, consumer protection agencies, and legal resources. The information provided is factual and aims to provide readers with a clear, unbiased understanding of the complexities surrounding minimum payments on credit cards.

Key Takeaways:

- Definition: A precise explanation of "Total Minimum Payment Due" and its components.

- Calculation: How the minimum payment is calculated by credit card issuers.

- Consequences of Minimum Payments: The long-term financial implications of only paying the minimum.

- Debt Management Strategies: Effective strategies for managing credit card debt beyond minimum payments.

- Legal Aspects: Understanding potential legal ramifications of prolonged non-payment.

Smooth Transition to the Core Discussion:

Now that we understand the importance of comprehending the "Total Minimum Payment Due," let's dissect this crucial aspect of credit card management.

Exploring the Key Aspects of "Total Minimum Payment Due"

1. Definition and Core Concepts:

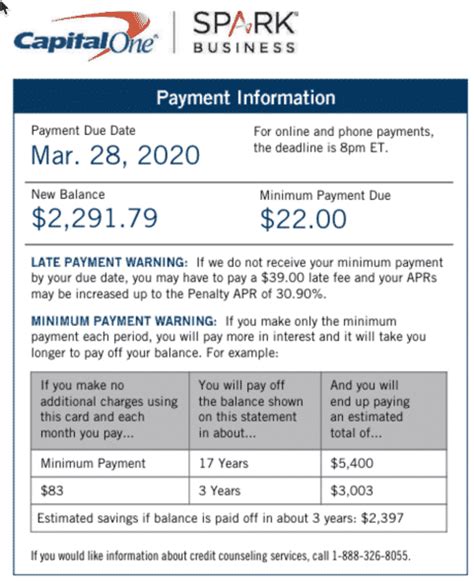

The "Total Minimum Payment Due" represents the smallest amount of money you can pay on your credit card statement without incurring late payment fees. It typically includes a portion of your outstanding balance, plus any accrued interest and applicable fees. Importantly, it's a minimum, not an ideal, payment.

2. Calculation Methods:

There isn't a single, universally applied formula for calculating the minimum payment. However, common methods include:

- Percentage of Balance: A common approach is to set the minimum payment at a fixed percentage (often 1-3%) of the outstanding balance.

- Flat Fee Plus Interest: Some issuers may require a minimum flat fee, plus the total interest accrued during the billing cycle.

- Combination Approach: Many issuers combine both methods, ensuring a minimum payment that's at least a percentage of the balance, but also covers the accumulated interest. If the percentage-based calculation results in a lower amount than the interest and fee total, the higher amount is required as the minimum.

3. Applications Across Industries:

The concept of minimum payment is consistent across various credit card issuers, though the specific calculation method may vary. Understanding this consistency allows consumers to apply their knowledge effectively regardless of the credit card provider.

4. Impact on Credit Scores:

While paying the minimum payment prevents immediate late payment fees, it's crucial to understand the long-term impact on your credit score. Continuously paying only the minimum significantly increases the utilization rate (the percentage of your available credit you're using). High utilization rates negatively impact your credit score, making it harder to secure loans, rent an apartment, or even obtain certain jobs.

Closing Insights: Summarizing the Core Discussion

The "Total Minimum Payment Due" is a critical element of your credit card statement, reflecting the smallest payment you can make without facing immediate penalties. However, relying solely on minimum payments is a financially risky strategy with long-term consequences for your credit health and overall financial well-being.

Exploring the Connection Between High Interest Rates and "Total Minimum Payment Due"

High interest rates are intrinsically linked to the "Total Minimum Payment Due." When only making the minimum payment, a significant portion goes towards interest, leaving a smaller amount to reduce the principal balance. This results in a prolonged period of debt repayment, accruing even more interest over time, creating a vicious cycle of debt.

Key Factors to Consider:

- Roles and Real-World Examples: Consider a $10,000 balance with a 20% APR. The minimum payment may be just $200, with $150 going to interest and only $50 reducing the principal. This slow repayment traps individuals in a long-term debt cycle.

- Risks and Mitigations: The significant risk is prolonged debt and damage to credit scores. Mitigation strategies involve increasing payments beyond the minimum, exploring balance transfer options, or seeking professional debt counseling.

- Impact and Implications: Long-term, high-interest debt can severely restrict financial flexibility, impacting purchasing power, savings goals, and overall financial freedom.

Conclusion: Reinforcing the Connection

The connection between high interest rates and minimum payments underscores the danger of only meeting the minimum payment requirement. This strategy often leads to prolonged debt and a diminished credit score, ultimately hindering long-term financial progress.

Further Analysis: Examining the "Debt Snowball" and "Debt Avalanche" Methods

Addressing credit card debt effectively requires strategies beyond simply meeting the minimum payment. Two commonly used methods are the "Debt Snowball" and "Debt Avalanche" methods.

- Debt Snowball: This method prioritizes paying off the smallest debt first, regardless of interest rate. The psychological boost of quickly eliminating a debt can motivate continued repayment efforts.

- Debt Avalanche: The "Debt Avalanche" method targets the debt with the highest interest rate first. This approach minimizes the total interest paid over the long term but can be less motivating initially as the payoff period for the largest debt may be longer.

Both methods offer viable approaches to tackling credit card debt, allowing individuals to tailor their strategy to their personal circumstances and motivational preferences.

FAQ Section: Answering Common Questions About "Total Minimum Payment Due"

- What happens if I only pay the minimum payment? While you avoid late fees, you'll pay significantly more interest over time, and your credit utilization will increase, potentially damaging your credit score.

- What if I can't afford the minimum payment? Contact your credit card issuer immediately to discuss options like hardship programs, payment plans, or temporary interest rate reductions. Ignoring the issue will only worsen the situation.

- How is the minimum payment calculated? The calculation method varies by issuer, but it typically involves a percentage of your balance or a fixed amount plus accrued interest.

- Can I negotiate a lower minimum payment? In some cases, you might be able to negotiate a lower payment with your issuer, especially if you're facing financial hardship. However, this is not always guaranteed.

- Will paying more than the minimum help my credit score? Yes, consistently paying more than the minimum will reduce your credit utilization ratio, which positively impacts your credit score.

Practical Tips: Maximizing the Benefits of Responsible Credit Card Usage

- Budgeting: Create a realistic budget to track income and expenses, ensuring you can afford credit card payments.

- Payment Automation: Set up automatic payments to avoid missed payments and late fees.

- Debt Consolidation: Consider consolidating high-interest debts into a lower-interest loan or balance transfer card.

- Financial Counseling: Seek professional advice from a certified credit counselor to develop a personalized debt management plan.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding the "Total Minimum Payment Due" on your credit card statement is paramount to responsible credit card management. While it represents the least you can pay without immediate penalties, relying solely on minimum payments can lead to a debt spiral with far-reaching financial consequences. By adopting proactive strategies and a commitment to responsible spending and repayment, you can navigate the complexities of credit cards effectively and build a strong financial future. Remember, proactively managing your credit card debt is a key component of maintaining good financial health.

Latest Posts

Latest Posts

-

What Is The Standard Payment For Pip

Apr 06, 2025

-

What Is The Lowest Payment For Pip

Apr 06, 2025

-

How Much Is Minimum Pip Payment

Apr 06, 2025

-

What Is The Minimum Pip Coverage In Michigan

Apr 06, 2025

-

What Is The Minimum Pip Coverage In Florida

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about What Does Total Minimum Payment Due Mean On A Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.